- LIVE QUOTES

- LEARN

- HELP

Nasdaq

Nasdaq Wall Street Journal

Wall Street JournalEN

Arista Networks (ANET) Is Down 9.7% After AMD‑Meta AI Pact Expands Hyperscaler Buildouts – Has The Bull Case Changed?

- In February 2026, Advanced Micro Devices announced a multi‑year AI infrastructure agreement with Meta Platforms, expanding their collaboration on hardware and software to support next‑generation AI workloads and lifting sentiment around key networking providers such as Arista Networks.

- The development underscores how hyperscaler AI buildouts and aligned chip‑to‑network ecosystems can influence demand expectations for Arista’s Ethernet‑based data center and AI networking solutions.

- Against this backdrop, we’ll examine how the expanded AMD‑Meta AI infrastructure agreement could reshape Arista Networks’ AI‑driven investment narrative.

Capitalize on the AI infrastructure supercycle with our selection of the 34 best 'picks and shovels' of the AI gold rush converting record-breaking demand into massive cash flow.

Arista Networks Investment Narrative Recap

To own Arista Networks, you generally have to believe that Ethernet based AI and cloud networking will keep gaining traction with hyperscalers, and that Arista can defend its margins despite customer concentration and rising competition. The AMD Meta AI infrastructure agreement has lifted sentiment around AI data center buildouts, but it does not materially change Arista’s most immediate swing factors: hyperscaler order timing and exposure to tariff or trade related shocks.

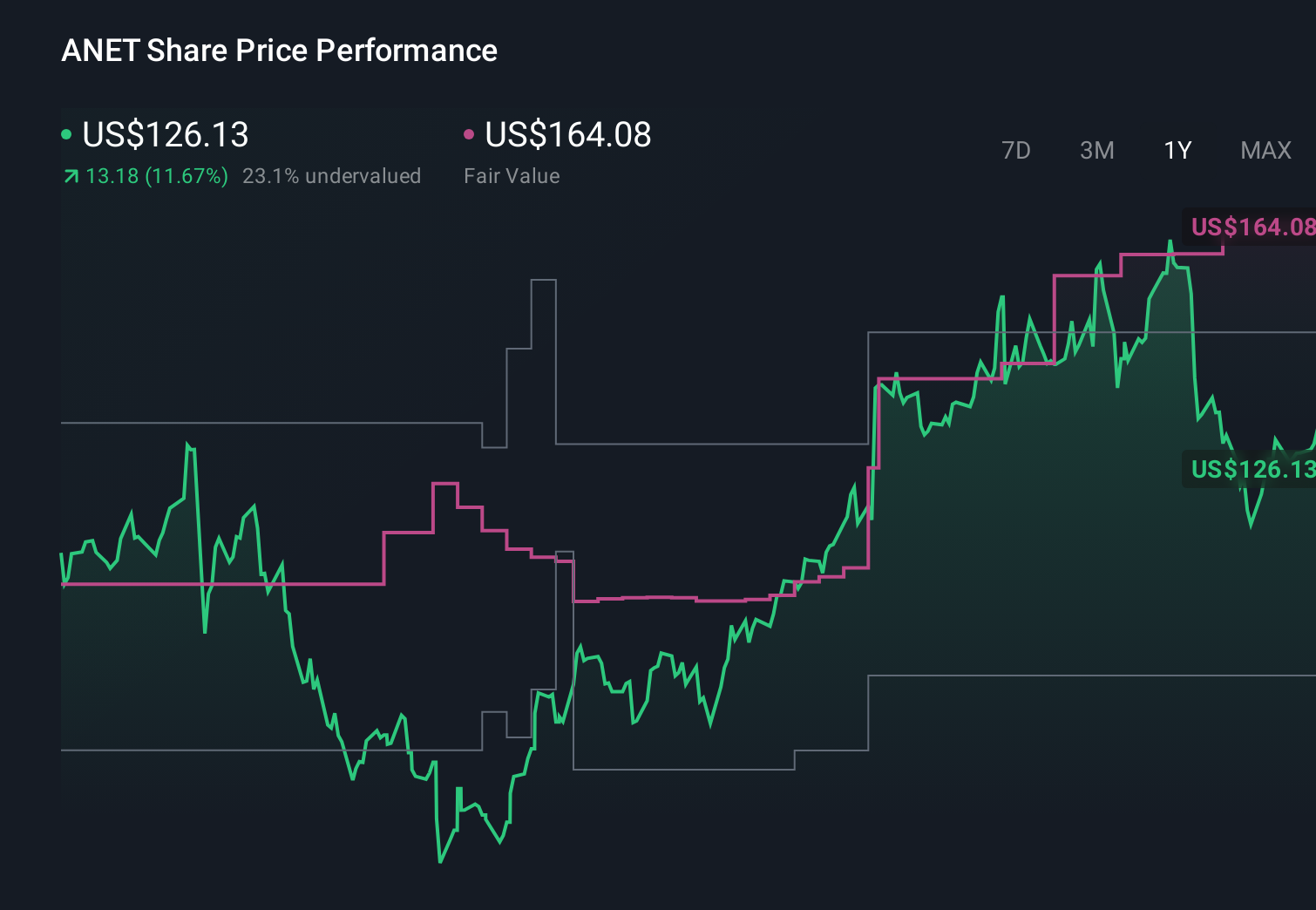

The most relevant recent milestone here is Arista’s Q4 2025 earnings, where revenue reached US$2,487.8 million and net income was US$955.8 million, with full year 2025 revenue of US$9,005.7 million. That performance, alongside Q1 2026 revenue guidance of about US$2.6 billion, has kept attention on AI driven cloud demand as the key near term catalyst, while also highlighting execution risk around deferred revenue and experimental AI deployments.

Yet investors should also be aware that growing dependence on a handful of hyperscale AI customers could quickly amplify the impact of any shift in ordering behavior...

Read the full narrative on Arista Networks (it's free!)

Arista Networks’ narrative projects $13.6 billion revenue and $5.4 billion earnings by 2028. This requires 19.5% yearly revenue growth and about a $2.1 billion earnings increase from $3.3 billion today.

Uncover how Arista Networks' forecasts yield a $163.37 fair value, a 27% upside to its current price.

Exploring Other Perspectives

Some of the most optimistic analysts were already modeling Arista’s revenue near US$15.4 billion and earnings around US$5.9 billion by 2028, so if you lean toward that view, the AMD Meta news may strengthen your belief that AI driven Ethernet adoption can offset the customer concentration risks you are taking on.

Explore 17 other fair value estimates on Arista Networks - why the stock might be worth as much as 51% more than the current price!

Form Your Own Verdict

Disagree with existing narratives? Extraordinary investment returns rarely come from following the herd, so go with your instincts.

- A great starting point for your Arista Networks research is our analysis highlighting 4 key rewards and 1 important warning sign that could impact your investment decision.

- Our free Arista Networks research report provides a comprehensive fundamental analysis summarized in a single visual - the Snowflake - making it easy to evaluate Arista Networks' overall financial health at a glance.

Ready For A Different Approach?

Early movers are already taking notice. See the stocks they're targeting before they've flown the coop:

- The future of work is here. Discover the 33 top robotics and automation stocks leading the charge in AI-driven automation and industrial transformation.

- The latest GPUs need a type of rare earth metal called Neodymium and there are only 30 companies in the world exploring or producing it. Find the list for free.

- We've uncovered the 16 dividend fortresses yielding 5%+ that don't just survive market storms, but thrive in them.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

Have feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team@simplywallst.com