- LIVE QUOTES

- LEARN

- HELP

Nasdaq

Nasdaq Wall Street Journal

Wall Street JournalEN

Is Bruker’s (BRKR) Spatial Biology Push Quietly Redefining Its Long-Term Competitive Moat?

- Earlier this week, Bruker Corporation unveiled major upgrades across its spatial biology and proteomics portfolio, including the PaintScape 3D genome visualization platform, the CellScape XR spatial proteomics system, Functional Proteomics 2.0 workflows on timsOmni, and a new Spatial Biology Center of Excellence with the University of Glasgow.

- Together, these launches and collaborations deepen Bruker’s presence in high-content multiomics and translational research tools, potentially increasing the importance of its software, consumables, and workflow ecosystems in long-term research programs.

- We’ll now examine how Bruker’s expanded spatial biology ecosystem, especially PaintScape’s 3D genome capabilities, may influence its existing investment narrative.

Find 56 companies with promising cash flow potential yet trading below their fair value.

Bruker Investment Narrative Recap

To own Bruker, you need to believe its investment in advanced spatial biology and proteomics can translate a complex instrument portfolio into growing, higher quality recurring revenue. The key near term catalyst is whether new platforms like PaintScape and CellScape XR can help offset soft academic and biopharma demand and support the company’s modest 2026 organic growth outlook. The biggest risk remains that prolonged funding and order weakness keeps book to bill and backlog under pressure, limiting any recovery.

Among the recent announcements, PaintScape’s move into pre orders with shipments expected this spring looks most relevant. It adds a differentiated 3D genome visualization capability that sits squarely within Bruker’s broader spatial biology ecosystem, deepening the link between instruments, software and consumables. If adoption progresses, it could reinforce the catalyst of mix improving toward higher attachment, workflow based revenue, even as macro and funding risks remain very much in focus.

Yet, while the product story is compelling, investors should be aware that prolonged weakness in research funding and order intake could still...

Read the full narrative on Bruker (it's free!)

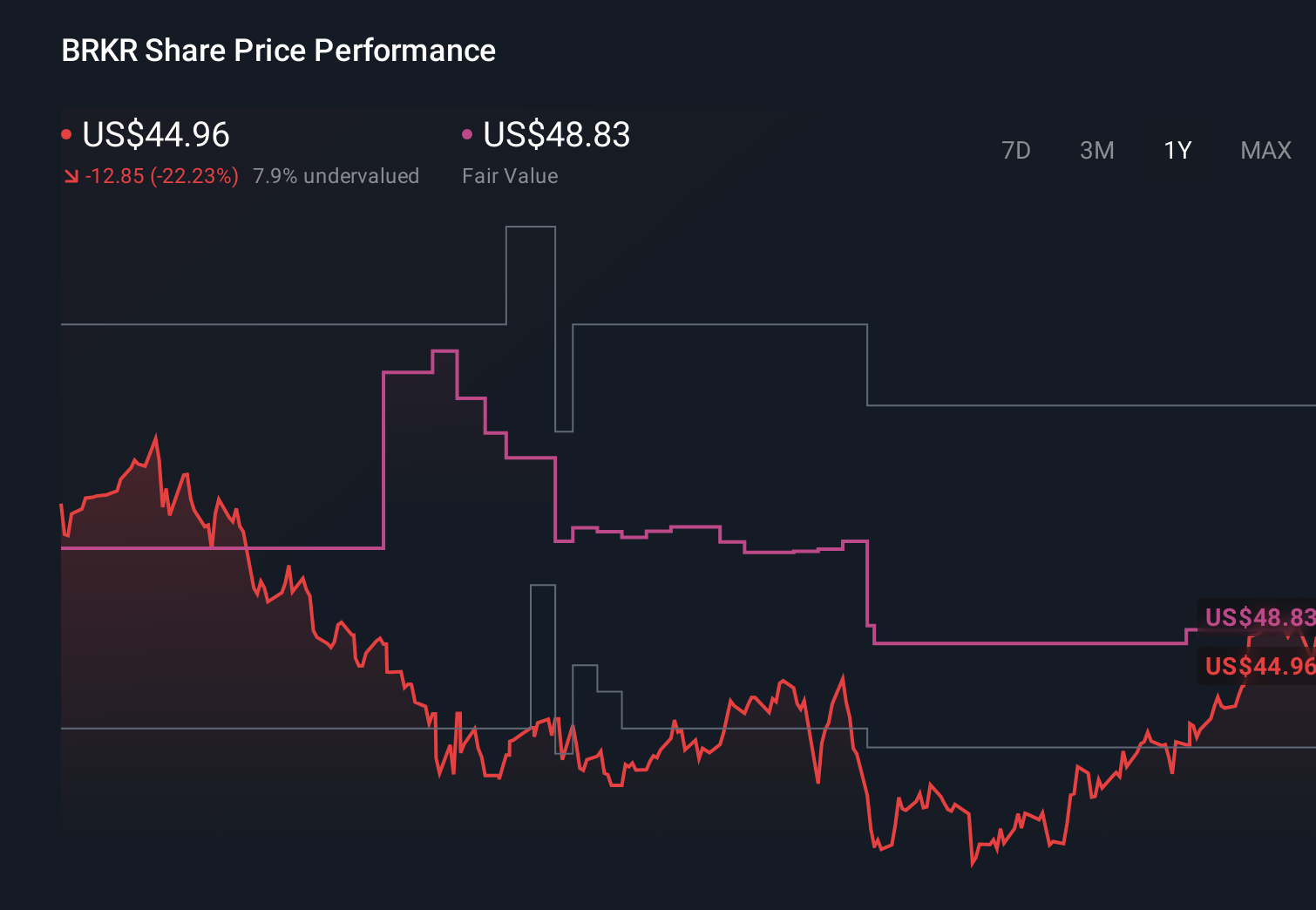

Bruker’s narrative projects $3.8 billion revenue and $404.1 million earnings by 2028.

Uncover how Bruker's forecasts yield a $54.43 fair value, a 38% upside to its current price.

Exploring Other Perspectives

Some analysts were far more optimistic, assuming revenue near US$3.9 billion and earnings around US$449.5 million by 2028, but the latest spatial biology launches could either support that view or highlight how sensitive those expectations are to funding risk and competition.

Explore 5 other fair value estimates on Bruker - why the stock might be worth as much as 90% more than the current price!

Form Your Own Verdict

Don't just follow the ticker - dig into the data and build a conviction that's truly your own.

- A great starting point for your Bruker research is our analysis highlighting 3 key rewards and 1 important warning sign that could impact your investment decision.

- Our free Bruker research report provides a comprehensive fundamental analysis summarized in a single visual - the Snowflake - making it easy to evaluate Bruker's overall financial health at a glance.

Searching For A Fresh Perspective?

Early movers are already taking notice. See the stocks they're targeting before they've flown the coop:

- Invest in the nuclear renaissance through our list of 85 elite nuclear energy infrastructure plays powering the global AI revolution.

- Uncover the next big thing with 31 elite penny stocks that balance risk and reward.

- The best AI stocks today may lie beyond giants like Nvidia and Microsoft. Find the next big opportunity with these 24 smaller AI-focused companies with strong growth potential through early-stage innovation in machine learning, automation, and data intelligence that could fund your retirement.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

Have feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team@simplywallst.com