- LIVE QUOTES

- LEARN

- HELP

Nasdaq

Nasdaq Wall Street Journal

Wall Street JournalEN

Will NNN REIT's New Chair (NNN) Subtly Shift Its Long-Term Governance and Strategy Priorities?

- NNN REIT has confirmed that Board Chairperson Steven D. Cosler retired on February 18, 2026, after nearly a decade of service, and independent director Edward J. Fritsch, an experienced REIT leader and former Highwoods Properties CEO, was appointed to succeed him.

- Fritsch’s long tenure on NNN’s board and his industry leadership roles at Highwoods and Nareit suggest continuity in governance and deep sector expertise at the helm.

- With Edward Fritsch now chairing the board, we’ll examine how this governance change might influence NNN REIT’s investment narrative and outlook.

This technology could replace computers: discover 23 stocks that are working to make quantum computing a reality.

NNN REIT Investment Narrative Recap

To own NNN REIT, you need to be comfortable with a slow and steady net lease model focused on long-duration, e‑commerce resistant tenants and a high, recurring dividend. The board transition from Steven Cosler to veteran REIT operator Edward Fritsch looks evolutionary rather than disruptive, and does not materially alter the near term focus on external growth through acquisitions or the key risk around tenant health and retail bankruptcies.

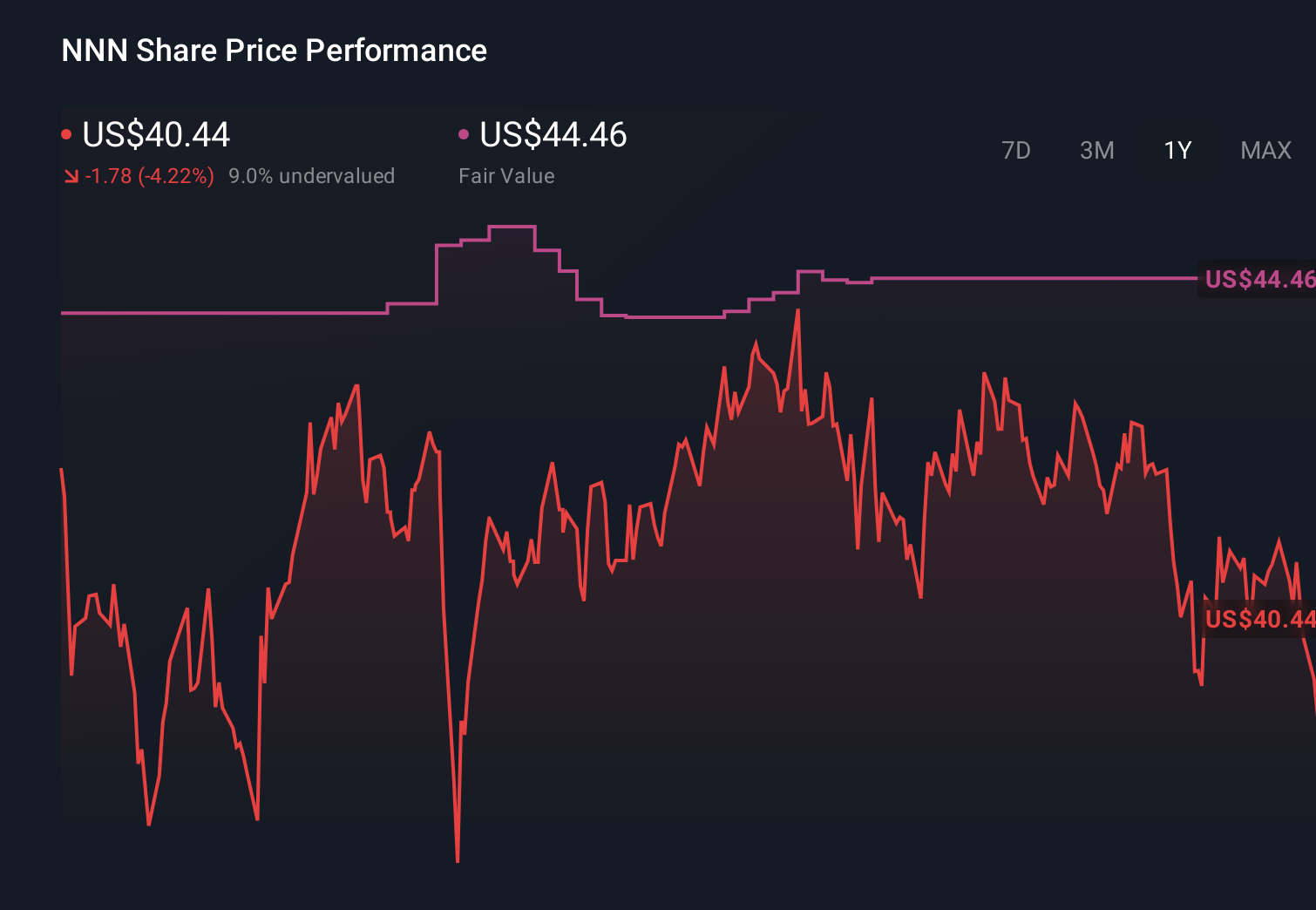

The most relevant recent data point alongside this governance change is NNN’s 2026 earnings guidance of US$2.02 to US$2.08 per share (excluding certain items), which frames investor expectations around modest profit growth. With competition for acquisitions tightening cap rates and tenant risk still in focus, this guidance helps anchor how much room NNN may have to absorb vacancies, higher financing costs, or slower lease up activity while supporting its dividend.

However, behind the reassuring board continuity, investors should still be aware that tenant bankruptcies and consolidations could...

Read the full narrative on NNN REIT (it's free!)

NNN REIT's narrative projects $1.0 billion revenue and $425.2 million earnings by 2028.

Uncover how NNN REIT's forecasts yield a $44.54 fair value, in line with its current price.

Exploring Other Perspectives

Three Simply Wall St Community fair value estimates for NNN REIT range from US$44.54 to US$79.18, highlighting how far apart individual views can be. Set against this, the central catalyst remains NNN’s reliance on long term, net leases to e commerce resistant tenants, which could influence how each of these investors thinks about the resilience of future cash flows.

Explore 3 other fair value estimates on NNN REIT - why the stock might be worth as much as 78% more than the current price!

Reach Your Own Conclusion

Don't just follow the ticker - dig into the data and build a conviction that's truly your own.

- A great starting point for your NNN REIT research is our analysis highlighting 4 key rewards and 1 important warning sign that could impact your investment decision.

- Our free NNN REIT research report provides a comprehensive fundamental analysis summarized in a single visual - the Snowflake - making it easy to evaluate NNN REIT's overall financial health at a glance.

Interested In Other Possibilities?

These stocks are moving-our analysis flagged them today. Act fast before the price catches up:

- Rare earth metals are the new gold rush. Find out which 30 stocks are leading the charge.

- AI is about to change healthcare. These 27 stocks are working on everything from early diagnostics to drug discovery. The best part - they are all under $10b in market cap - there's still time to get in early.

- Outshine the giants: these 24 early-stage AI stocks could fund your retirement.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

Have feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team@simplywallst.com