- LIVE QUOTES

- LEARN

- HELP

Nasdaq

Nasdaq Wall Street Journal

Wall Street JournalEN

Don't Even Think About Buying Tilray Stock Until You Read This Warning

Key Points

Tilray has been expanding beyond marijuana to include hemp products and alcoholic beverages.

The company's strategy has led to top-line growth, but it has yet to generate sustainable profits.

Tilray Brands (NASDAQ: TLRY) bills itself as "a global lifestyle and consumer packaged goods company leading at the nexus of the beverage, cannabis, and wellness industries." While largely viewed as a marijuana stock, the company also sells hemp products and alcoholic beverages. The question is whether this amalgam of products will actually lead to profits. So will it?

Tilray Brands is losing money

After its initial public offering, Tilray Brands' stock price skyrocketed. At that point, Wall Street was enamored of marijuana companies, and investors were excited about the future. There was a good reason to be excited, given that more and more locations have been legalizing the use of cannabis. However, Tilray wasn't the only company attempting to capitalize on the opportunity, and competition has been fierce.

Where to invest $1,000 right now? Our analyst team just revealed what they believe are the 10 best stocks to buy right now, when you join Stock Advisor. See the stocks »

Image source: Getty Images.

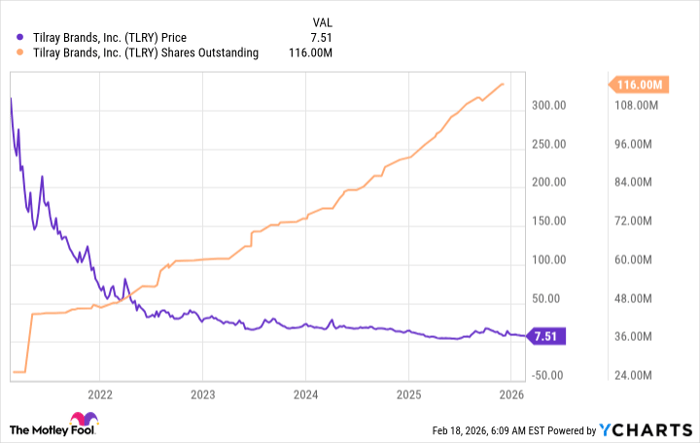

Now add on the still existing illicit drug trade, and it has been hard for cannabis companies to generate sustainable profits. Tilray is no different in this regard, and investors have grown tired of waiting for black ink on the bottom line. The stock is now down 99% from its all-time high. Recognizing that marijuana might not be enough, the company has expanded into other areas, notably alcohol. This brings both risk and opportunity, but so far it hasn't yielded positive earnings.

Tilray is moving fast

Right now, Tilray is focusing a lot on the revenue growth it is achieving. That's fair, but the revenue growth has to be viewed in context. The company has been aggressively buying brands since 2021. Each new brand brings additional revenue, and there are synergy opportunities, as well, as a brand is integrated into the company. However, there are costs to consider.

The one that investors need to think about most right now is Tilray's steadily rising share count. It isn't unusual for companies to raise cash by selling stock or to pay for acquisitions with shares. However, each new share dilutes existing shareholders. And this approach could also make it harder for the company to generate a profit, since earnings are being spread over an increasing number of shares.

Tilray is a high-risk investment

Given the ongoing losses and aggressive acquisition approach management has undertaken, investors should tread with caution. Sometimes companies stretch themselves too far in an effort to buy their way to growth. Notably, the company has already been forced to take write-downs across every division. Most investors will be better off watching from the sidelines here until Tilray has proven its model can support sustainable earnings.

Reuben Gregg Brewer has no position in any of the stocks mentioned. The Motley Fool recommends Tilray Brands. The Motley Fool has a disclosure policy.