- LIVE QUOTES

- LEARN

- HELP

Nasdaq

Nasdaq Wall Street Journal

Wall Street JournalEN

Record Blue Creek Ramp And Higher 2026 Output Guidance Might Change The Case For Investing In Warrior Met Coal (HCC)

- Warrior Met Coal, Inc. reported past fourth-quarter 2025 results showing steelmaking coal production rising to 3,392,000 short tons, including 1.3 million short tons from the newly producing Blue Creek mine, alongside higher quarterly revenue and net income versus a year earlier.

- Despite full-year 2025 revenue and earnings being lower than the prior year, record output and the early, low-cost ramp-up at Blue Creek underpinned stronger margins in late 2025 and supported the company’s higher 2026 production and sales guidance of 12.0–13.0 million and 12.5–13.5 million short tons respectively.

- We’ll now explore how Blue Creek’s early ramp and Warrior Met Coal’s higher 2026 production guidance reshape the company’s broader investment narrative.

Rare earth metals are an input to most high-tech devices, military and defence systems and electric vehicles. The global race is on to secure supply of these critical minerals. Beat the pack to uncover the 30 best rare earth metal stocks of the very few that mine this essential strategic resource.

Warrior Met Coal Investment Narrative Recap

To own Warrior Met Coal, you need to believe Blue Creek can turn record tonnage and lower costs into sustainably better profitability, despite soft steelmaking coal markets and dependence on Asian buyers. The latest results support that near term catalyst by showing Blue Creek contributing 1.3 million short tons in Q4 2025 and lifting margins, while the key risk remains whether higher 2026 volumes can be profitably placed if pricing stays under pressure. So far, this news does not materially change that risk.

The most relevant recent announcement is Warrior’s 2026 production and sales guidance of 12.0 to 13.0 million and 12.5 to 13.5 million short tons. Set against the strong Q4 production ramp, this guidance ties directly into the main catalyst of Blue Creek scaling up. It also intersects with the main risk that a bigger output base, in a weak pricing backdrop, could strain free cash flow if customers do not absorb the extra tons on acceptable terms.

Yet behind the stronger volumes and guidance, investors should be aware that...

Read the full narrative on Warrior Met Coal (it's free!)

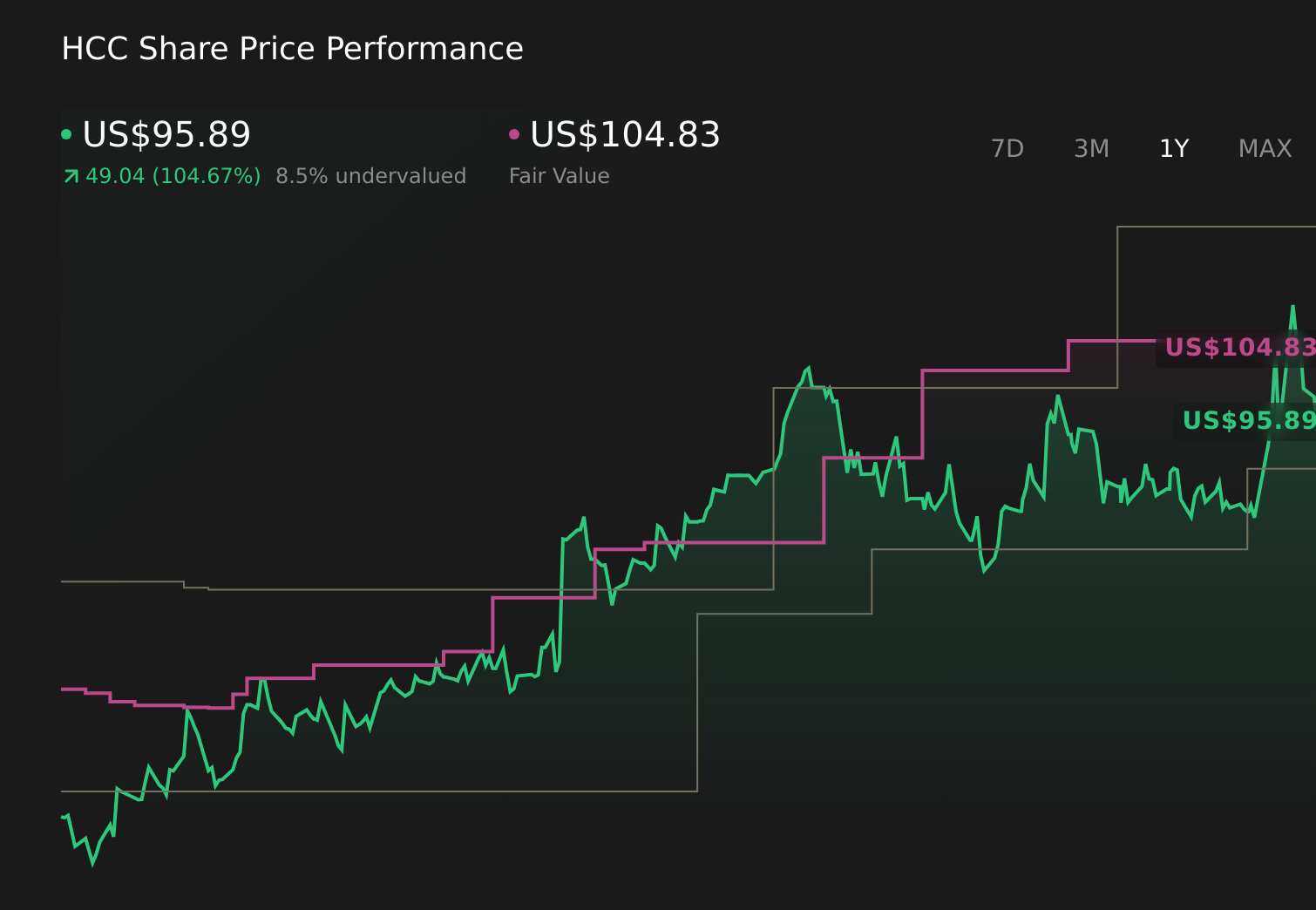

Warrior Met Coal's narrative projects $2.0 billion revenue and $636.5 million earnings by 2028.

Uncover how Warrior Met Coal's forecasts yield a $102.17 fair value, a 17% upside to its current price.

Exploring Other Perspectives

While recent results highlight faster Blue Creek ramp and higher 2026 volume targets, the most pessimistic analysts were assuming only about US$1.9 billion of revenue and US$264.0 million of earnings by 2028, so you should weigh that more cautious view of long term demand and margins against this newer production story.

Explore 3 other fair value estimates on Warrior Met Coal - why the stock might be worth as much as 17% more than the current price!

The Verdict Is Yours

Disagree with existing narratives? Extraordinary investment returns rarely come from following the herd, so go with your instincts.

- A great starting point for your Warrior Met Coal research is our analysis highlighting 1 key reward and 1 important warning sign that could impact your investment decision.

- Our free Warrior Met Coal research report provides a comprehensive fundamental analysis summarized in a single visual - the Snowflake - making it easy to evaluate Warrior Met Coal's overall financial health at a glance.

Ready For A Different Approach?

Our top stock finds are flying under the radar-for now. Get in early:

- Outshine the giants: these 25 early-stage AI stocks could fund your retirement.

- Capitalize on the AI infrastructure supercycle with our selection of the 34 best 'picks and shovels' of the AI gold rush converting record-breaking demand into massive cash flow.

- This technology could replace computers: discover 24 stocks that are working to make quantum computing a reality.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

Have feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team@simplywallst.com