- LIVE QUOTES

- LEARN

- HELP

Nasdaq

Nasdaq Wall Street Journal

Wall Street JournalEN

Assessing Williams-Sonoma (WSM) Valuation After Recent Share Price Pullback And Mixed Fair Value Signals

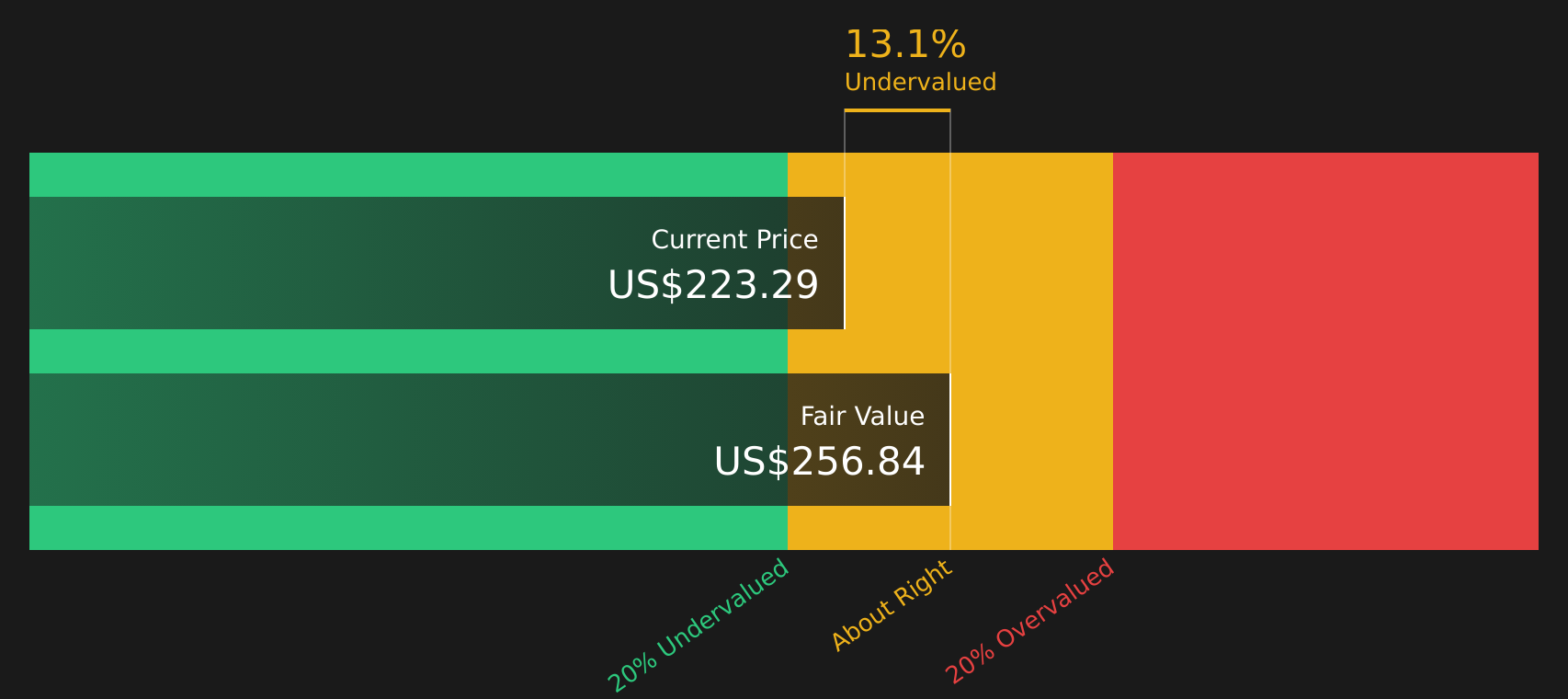

Williams-Sonoma stock snapshot after recent performance

Williams-Sonoma (WSM) shares recently closed at US$211.82, leaving investors weighing short term pullbacks against longer term returns. The stock shows mixed moves over the past week, month, and past 3 months.

See our latest analysis for Williams-Sonoma.

While the latest pullback leaves Williams-Sonoma with a 1-day share price return of a 1.28% decline and a 7-day share price return of a 2.29% decline, the 90-day share price return of 21.30% and 3-year total shareholder return of 249.01% suggest longer term momentum has been strong even as shorter term sentiment cools.

If this home-focused retailer has you rethinking where growth could come from next, it might be worth scanning our list of 23 top founder-led companies as a fresh hunting ground.

With Williams-Sonoma trading near US$211.82 and sitting slightly above some analyst targets yet still showing an intrinsic discount, you have to ask: is there real value left here, or is the market already pricing in future growth?

Most Popular Narrative: 6.6% Overvalued

With Williams-Sonoma last closing at $211.82 against a narrative fair value of about $199, the current share price sits above that widely followed estimate, which is built using an 8.56% discount rate.

Continued investment and advances in AI-powered tools and digital platforms are driving higher conversion rates, improved customer experience, and measurable productivity gains. This supports both revenue growth and expanded operating leverage at the margin level.

Want to understand why this valuation still leans rich? The narrative leans on steady revenue gains, resilient margins, and a future earnings multiple that assumes those trends hold. Curious which specific growth and profitability assumptions are doing the heavy lifting here, and how much optimism is baked into that premium?

Result: Fair Value of $199 (OVERVALUED)

Have a read of the narrative in full and understand what's behind the forecasts.

However, that optimism still depends on tariffs staying manageable and housing related demand not weakening further. Both of these factors could quickly challenge the current premium narrative.

Find out about the key risks to this Williams-Sonoma narrative.

Another Take: DCF Points In A Different Direction

The narrative-based fair value of about $199 suggests Williams-Sonoma is 6.6% overvalued at $211.82. Yet our DCF model points to a future cash flow value of $215.92, which is about 1.9% above the current price. Same company, two lenses; which one do you trust more?

Look into how the SWS DCF model arrives at its fair value.

Simply Wall St performs a discounted cash flow (DCF) on every stock in the world every day (check out Williams-Sonoma for example). We show the entire calculation in full. You can track the result in your watchlist or portfolio and be alerted when this changes, or use our stock screener to discover 56 high quality undervalued stocks. If you save a screener we even alert you when new companies match - so you never miss a potential opportunity.

Next Steps

If this mix of optimism and caution has you on the fence, take a moment to review the underlying data yourself and move quickly to shape your own view, starting with 2 key rewards.

Looking for more investment ideas?

If you stop with just one company, you risk missing other opportunities, so use the Simply Wall St screener to line up your next set of candidates.

- Target quality at a discount by scanning our list of 56 high quality undervalued stocks that pair solid fundamentals with pricing that may appeal to value focused investors.

- Focus on resilience first by checking out 80 resilient stocks with low risk scores, where companies show lower overall risk scores that may suit a more cautious approach.

- Hunt for future standouts by reviewing the screener containing 24 high quality undiscovered gems, highlighting companies with strong fundamentals that fewer investors may be watching closely.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

Have feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team@simplywallst.com