- LIVE QUOTES

- LEARN

- HELP

Nasdaq

Nasdaq Wall Street Journal

Wall Street JournalEN

Moelis (MC) Expands Buybacks And Dividends – What Does This Reveal About Its Margin Story?

- In early February 2026, Moelis & Company reported fourth-quarter 2025 net income of US$87.87 million and full-year net income of US$233.04 million, alongside a regular quarterly dividend of US$0.65 per share payable on March 26, 2026 to holders of record on February 17, 2026.

- On the same day, the firm completed a multi-year US$196.47 million buyback and launched a new, open-ended US$300 million repurchase program, reinforcing a capital return approach that pairs earnings growth with consistent shareholder distributions.

- We’ll examine how Moelis’s new US$300 million share repurchase program may influence its existing investment narrative around margin expansion.

The latest GPUs need a type of rare earth metal called Dysprosium and there are only 30 companies in the world exploring or producing it. Find the list for free.

Moelis Investment Narrative Recap

To own Moelis, you need to be comfortable with a transaction-driven advisory model that can swing with deal cycles, while management pushes for margin expansion through higher-fee PCA and sector teams. The latest results and new US$300 million buyback support the existing capital return story but do not fundamentally change the near-term catalyst around sustaining margin gains or the key risk that compensation and expansion costs could again pressure profitability if deal activity slows.

The most relevant update here is the open-ended US$300 million repurchase program, following completion of the prior US$196.47 million plan. For investors focused on margins, this matters because buybacks can lift per-share earnings and signal confidence in the firm’s ability to keep funding both growth investments and shareholder returns, even as Moelis manages through the inherent earnings volatility of episodic, often lumpy advisory fees.

Yet investors should also be aware that, even with these repurchases and dividends, Moelis still faces the risk that heavy reliance on irregular large mandates could...

Read the full narrative on Moelis (it's free!)

Moelis' narrative projects $2.1 billion revenue and $381.7 million earnings by 2028. This requires 15.3% yearly revenue growth and about a $183.6 million earnings increase from $198.1 million today.

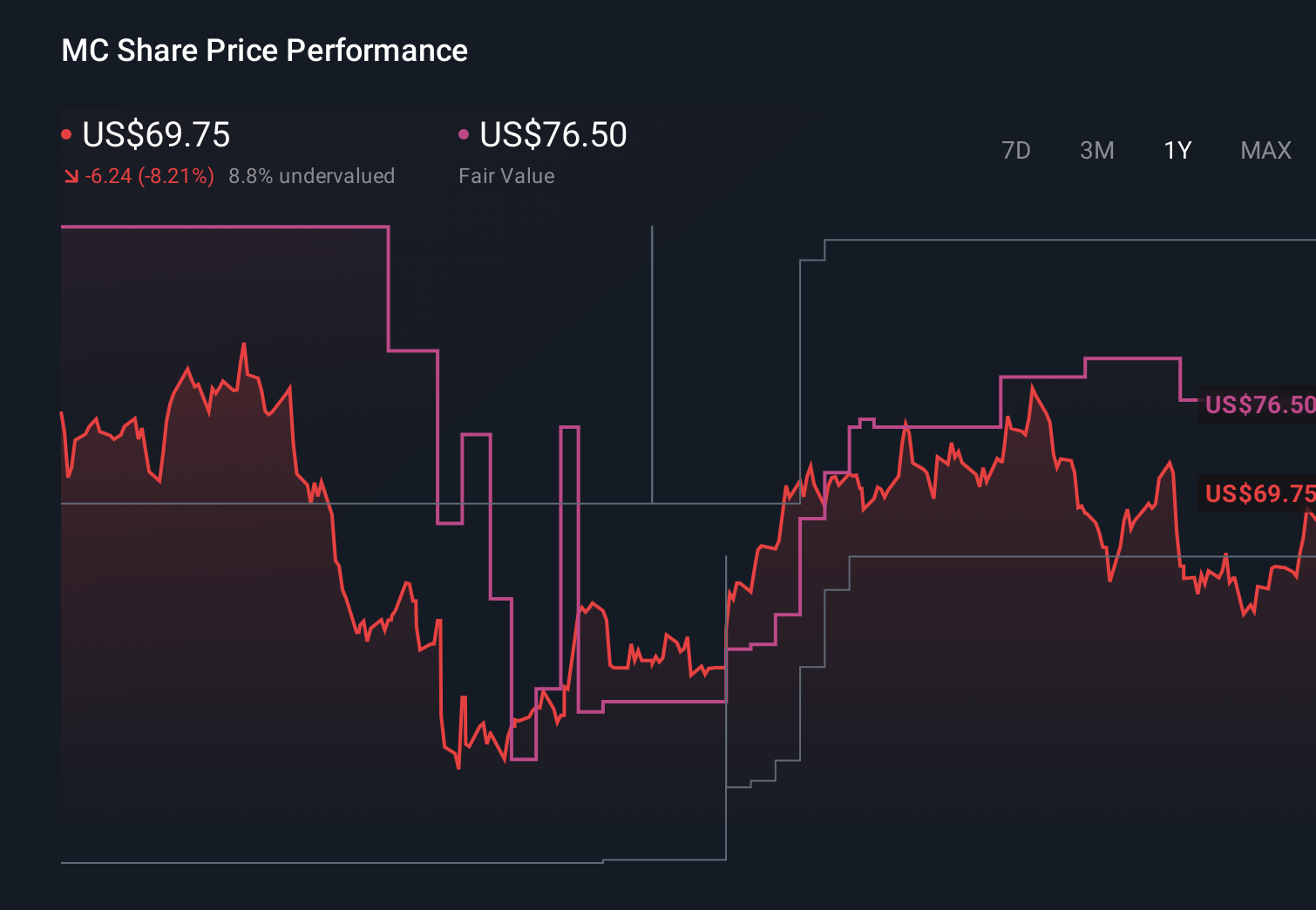

Uncover how Moelis' forecasts yield a $76.50 fair value, a 21% upside to its current price.

Exploring Other Perspectives

Some of the most optimistic analysts were already expecting Moelis to reach about US$2.4 billion of revenue and US$395 million of earnings, so this new buyback and earnings update could either support that faster growth story or reinforce concerns about dependence on big, uneven deals, reminding you that reasonable views on Moelis’s upside and risk can differ widely.

Explore 2 other fair value estimates on Moelis - why the stock might be worth just $76.50!

The Verdict Is Yours

Disagree with existing narratives? Extraordinary investment returns rarely come from following the herd, so go with your instincts.

- A great starting point for your Moelis research is our analysis highlighting 4 key rewards and 1 important warning sign that could impact your investment decision.

- Our free Moelis research report provides a comprehensive fundamental analysis summarized in a single visual - the Snowflake - making it easy to evaluate Moelis' overall financial health at a glance.

Curious About Other Options?

Every day counts. These free picks are already gaining attention. See them before the crowd does:

- Uncover the next big thing with 31 elite penny stocks that balance risk and reward.

- We've uncovered the 13 dividend fortresses yielding 5%+ that don't just survive market storms, but thrive in them.

- Outshine the giants: these 25 early-stage AI stocks could fund your retirement.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

Have feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team@simplywallst.com