- LIVE QUOTES

- LEARN

- HELP

Nasdaq

Nasdaq Wall Street Journal

Wall Street JournalEN

A Look At Empire State Realty Trust (ESRT) Valuation As New Leases And 2026 Guidance Draw Investor Attention

Why Empire State Realty Trust Stock Is Back on Investors’ Radar

Empire State Realty Trust (ESRT) just paired fresh leasing wins with tenants like TJ Maxx, JP Morgan Chase Bank, Burlington Stores, and Nespresso with updated earnings guidance and recent quarterly results that have caught investor attention.

See our latest analysis for Empire State Realty Trust.

Even with fresh leases, updated guidance and the recent SoHo acquisition, Empire State Realty Trust’s share price tells a mixed story, with a 1-day share price return of 1.91% against a 1-year total shareholder return of 28.04% decline, suggesting short term interest is picking up while longer term returns remain under pressure.

If this REIT news has you thinking about where else capital could work harder, take a look at 23 top founder-led companies as a way to uncover fresh stock ideas beyond real estate.

With ESRT shares down 28.04% on a 1-year total return, but trading below the average analyst price target and management guiding to 2026 earnings, you have to ask: is this a reset entry point, or is the market already pricing in what comes next?

Most Popular Narrative: 23.6% Undervalued

With Empire State Realty Trust last closing at $6.39 against a narrative fair value of $8.36, the widely followed view sees meaningful upside still on the table.

The analysts have a consensus price target of $8.967 for Empire State Realty Trust based on their expectations of its future earnings growth, profit margins and other risk factors. However, there is a degree of disagreement amongst analysts, with the most bullish reporting a price target of $10.0, and the most bearish reporting a price target of just $8.0.

Want to understand why modest revenue growth, shrinking margins and a rich future earnings multiple still add up to a higher fair value in this narrative? The tension between softer profit forecasts and a high implied P/E is exactly what makes this story worth a closer read.

The narrative uses an 8.25% discount rate and builds around gradual revenue growth, lower future profit margins and a higher earnings multiple to arrive at its $8.36 fair value. It also factors in expectations for share count changes and the balance between office exposure and diversified income streams such as observatory and multifamily, all of which feed into the return profile investors are being asked to underwrite.

Result: Fair Value of $8.36 (UNDERVALUED)

Have a read of the narrative in full and understand what's behind the forecasts.

However, you also have to weigh pressure on Observatory income and higher operating expenses, which could challenge the margin assumptions behind that higher fair value.

Find out about the key risks to this Empire State Realty Trust narrative.

Another Take: Earnings Multiple Sends a Different Signal

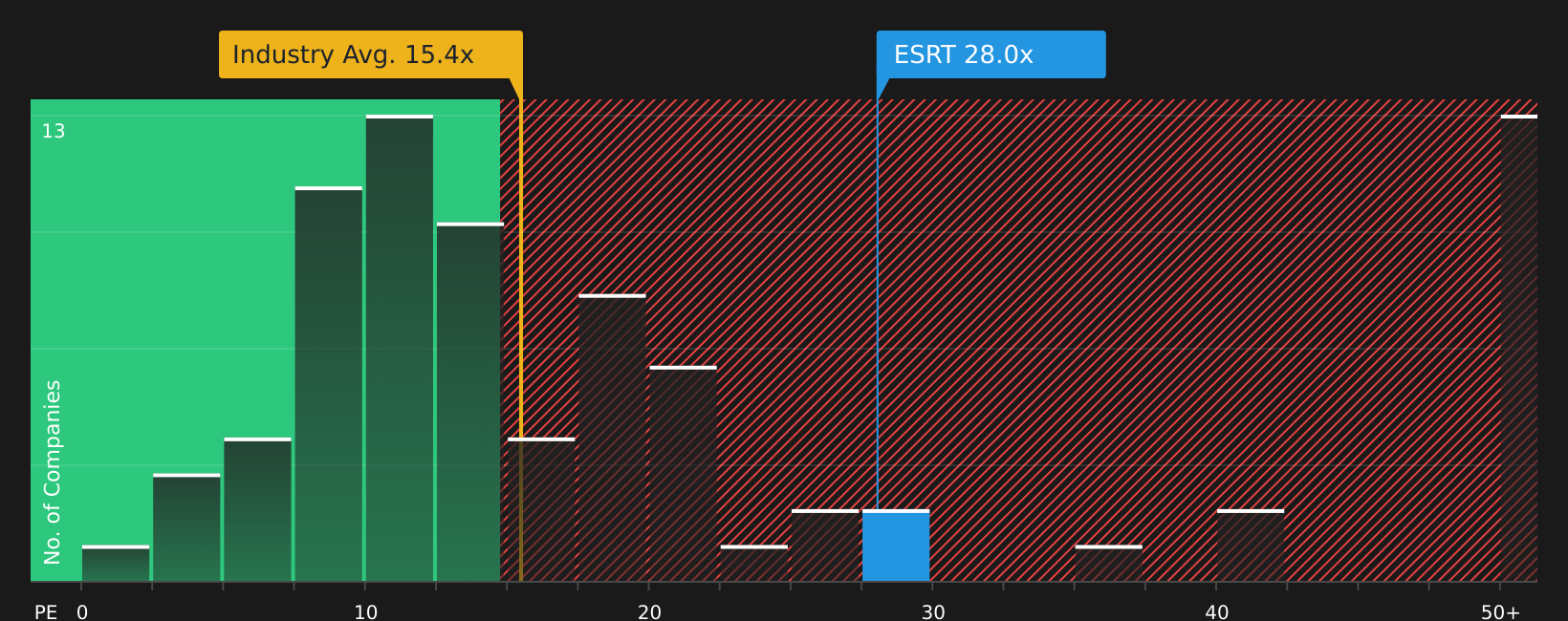

The narrative fair value of $8.36 paints ESRT as 23.6% undervalued, but the current P/E of 31.2x is above the fair ratio of 20.8x and above the global office REITs average of 20.6x, even if it sits below a 56.4x peer group. That mix of premium and discount raises a simple question: is the upside case already partly in the price?

See what the numbers say about this price — find out in our valuation breakdown.

Next Steps

Given the mixed signals in the share price and valuation, it is worth checking the full picture for yourself and moving quickly while sentiment is split. To weigh both the concerns and the potential upside, take a look at 2 key rewards and 4 important warning signs and decide where you stand.

Looking for more investment ideas?

If ESRT has you rethinking your watchlist, do not stop here. Use the screener to find other stocks that better match your return and risk goals.

- Target potential mispricing and look for value by reviewing our list of 56 high quality undervalued stocks, which currently screen well on quality and price.

- Strengthen the income side of your portfolio by checking out 13 dividend fortresses, focused on companies with higher yields that may support steadier cash flows.

- Calm the volatility in your holdings by scanning 80 resilient stocks with low risk scores to see which businesses score well on stability and financial resilience.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

Have feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team@simplywallst.com