- LIVE QUOTES

- LEARN

- HELP

Nasdaq

Nasdaq Wall Street Journal

Wall Street JournalEN

Assessing Genesis Energy (GEL) Valuation After Strong Q4 Earnings And Distribution Increase

Genesis Energy (GEL) has come back into focus after reporting stronger than expected fourth quarter earnings. The results were supported by offshore pipeline transportation growth, better margins, and a 9.1% increase in its quarterly common unit distribution.

See our latest analysis for Genesis Energy.

At a share price of $17.66, Genesis Energy has paired its stronger than expected fourth quarter earnings and higher distribution with positive momentum, including a 15.5% 90 day share price return and a 49.8% one year total shareholder return. This suggests recent news is being reflected in both income expectations and perceived risk.

If this kind of income focused story has your attention, you might also want to see what else is out there by checking a curated list of 23 top founder-led companies as another set of ideas to research.

With the units at $17.66, a value score of 4, and an indicated 64% discount to one intrinsic value estimate, the key question is clear: is Genesis Energy still mispriced, or is the market already baking in those future cash flows?

Preferred Price-to-Sales of 1.3x: Is It Justified?

On a P/S of 1.3x, Genesis Energy screens as good value against both its Oil and Gas peers and the wider US market, even after the recent share price strength.

The P/S multiple compares the company’s equity value to its revenue, which can be useful for a business that is currently loss making. For Genesis Energy, this helps investors focus on how the market is pricing its $1,630.415 million of revenue rather than its current net loss of $89.664 million.

Relative to the US Oil and Gas industry average P/S of 1.7x, Genesis Energy trades at a clear discount, and it also sits well below the peer average multiple of 2.6x. At the same time, our fair P/S estimate of 0.9x indicates the market is pricing the units above this regression based level, a gap that some investors may watch if sentiment or revenue expectations change.

Explore the SWS fair ratio for Genesis Energy

Result: Price-to-Sales of 1.3x (ABOUT RIGHT)

However, the story can change quickly if revenue growth remains weak at a 0.6% decline, or if the current net loss of $89.664 million widens.

Find out about the key risks to this Genesis Energy narrative.

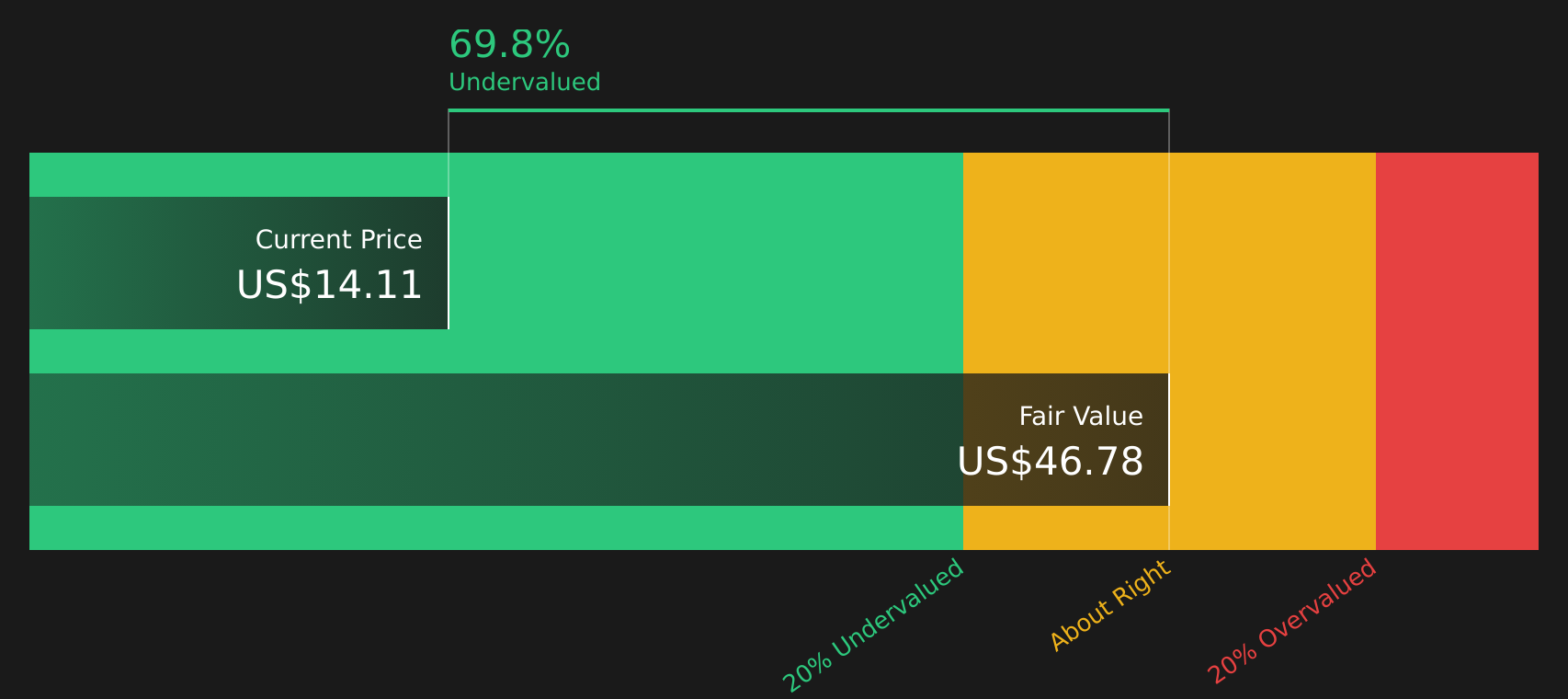

Another View: DCF Points to a Very Different Price

While the P/S of 1.3x suggests the units are roughly in line with where the market has settled, our DCF model presents a very different perspective. On that view, Genesis Energy at $17.66 is trading at a substantial discount to an indicated future cash flow value of $49.69. This raises a key question for investors: which signal matters more, current revenue multiples or long term cash flows?

Look into how the SWS DCF model arrives at its fair value.

Simply Wall St performs a discounted cash flow (DCF) on every stock in the world every day (check out Genesis Energy for example). We show the entire calculation in full. You can track the result in your watchlist or portfolio and be alerted when this changes, or use our stock screener to discover 56 high quality undervalued stocks. If you save a screener we even alert you when new companies match - so you never miss a potential opportunity.

Next Steps

Does this mix of signals leave you excited or cautious? Take a closer look at the full picture and weigh up the 2 key rewards and 2 important warning signs for yourself before deciding what it all means for you.

Looking for more investment ideas?

If Genesis Energy has sharpened your focus, do not stop here. Broaden your watchlist with other ideas that fit different goals and comfort levels.

- Target value opportunities first by reviewing our list of 56 high quality undervalued stocks that combine attractive pricing with solid fundamentals to consider for deeper research.

- Strengthen your income focus by scanning 13 dividend fortresses that aim to pair higher yields with resilience, so you are not relying on just one payer.

- Protect your downside by checking a 80 resilient stocks with low risk scores that highlights companies with more resilient profiles before the market fully prices them in.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

Have feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team@simplywallst.com