- LIVE QUOTES

- LEARN

- HELP

Nasdaq

Nasdaq Wall Street Journal

Wall Street JournalEN

Does Strong Q4 Earnings and New Shelf Registration Change The Bull Case For Philip Morris International (PM)?

- In early February 2026, Philip Morris International reported that fourth-quarter 2025 sales rose to US$10,362 million and net income reached US$2,141 million, while full-year 2025 sales increased to US$40.65 billion and net income to US$11.35 billion, alongside sharply higher earnings per share from continuing operations.

- On the same day, the company also filed an omnibus shelf registration for new debt securities and warrants, giving it flexibility to raise capital that could support its smoke-free transformation or other corporate needs without immediately committing to a specific issuance.

- We’ll now examine how Philip Morris International’s stronger recent earnings performance shapes its existing investment narrative around smoke-free growth and margins.

AI is about to change healthcare. These 25 stocks are working on everything from early diagnostics to drug discovery. The best part - they are all under $10b in market cap - there's still time to get in early.

Philip Morris International Investment Narrative Recap

To own Philip Morris International, you need to believe its smoke free portfolio can more than offset pressure on traditional cigarettes and protect margins. The latest results confirm stronger earnings and higher profit margins, but they do not fundamentally change the near term catalyst, which remains execution in smoke free products, nor the key risk, which is the possibility that growth in those products slows before combustibles’ decline is fully offset.

The omnibus shelf registration for new debt securities and warrants is the most relevant recent announcement here, as it gives PMI additional flexibility around funding needs at a time when smoke free growth, regulatory costs, and high existing leverage all matter for the investment case and perceived risk profile.

Yet alongside the stronger earnings, investors should still be aware of how rising regulation and potential smoke free growth slowdowns could...

Read the full narrative on Philip Morris International (it's free!)

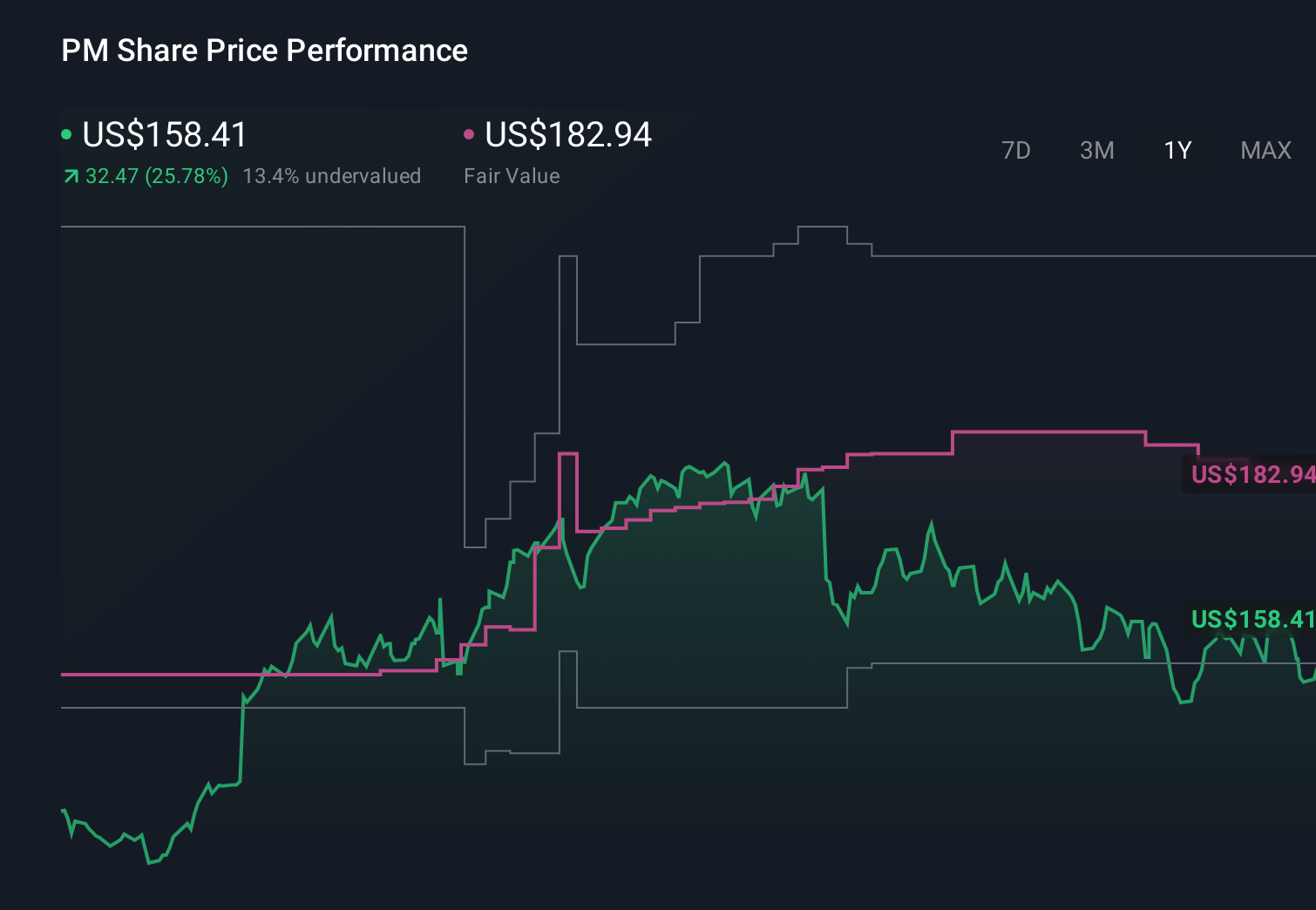

Philip Morris International's narrative projects $49.4 billion revenue and $14.5 billion earnings by 2028. This requires 8.2% yearly revenue growth and a $6.3 billion earnings increase from $8.2 billion today.

Uncover how Philip Morris International's forecasts yield a $180.38 fair value, in line with its current price.

Exploring Other Perspectives

Before this earnings beat, the most optimistic analysts were assuming revenue near US$53.2 billion and earnings around US$15.7 billion by 2028, which is far more bullish than consensus and leans heavily on faster smoke free growth than many expect; with 2025 net income already at US$11.35 billion, these views could either gain support or be reassessed as new results like this come through, so it is worth comparing several different outlooks side by side.

Explore 10 other fair value estimates on Philip Morris International - why the stock might be worth as much as 17% more than the current price!

The Verdict Is Yours

Disagree with existing narratives? Extraordinary investment returns rarely come from following the herd, so go with your instincts.

- A great starting point for your Philip Morris International research is our analysis highlighting 4 key rewards and 1 important warning sign that could impact your investment decision.

- Our free Philip Morris International research report provides a comprehensive fundamental analysis summarized in a single visual - the Snowflake - making it easy to evaluate Philip Morris International's overall financial health at a glance.

Want Some Alternatives?

Opportunities like this don't last. These are today's most promising picks. Check them out now:

- The latest GPUs need a type of rare earth metal called Dysprosium and there are only 30 companies in the world exploring or producing it. Find the list for free.

- Find 56 companies with promising cash flow potential yet trading below their fair value.

- Uncover the next big thing with 31 elite penny stocks that balance risk and reward.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

Have feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team@simplywallst.com