- LIVE QUOTES

- LEARN

- HELP

Nasdaq

Nasdaq Wall Street Journal

Wall Street JournalEN

Covista (ATGE) Valuation Check As New Ross University Dean Appointment Targets Healthcare Education Strength

Covista (ATGE) stock is in focus after the company named Cheryl Holmes, M.D., as the next dean of Ross University School of Medicine, a leadership appointment closely tied to its healthcare education strategy.

See our latest analysis for Covista.

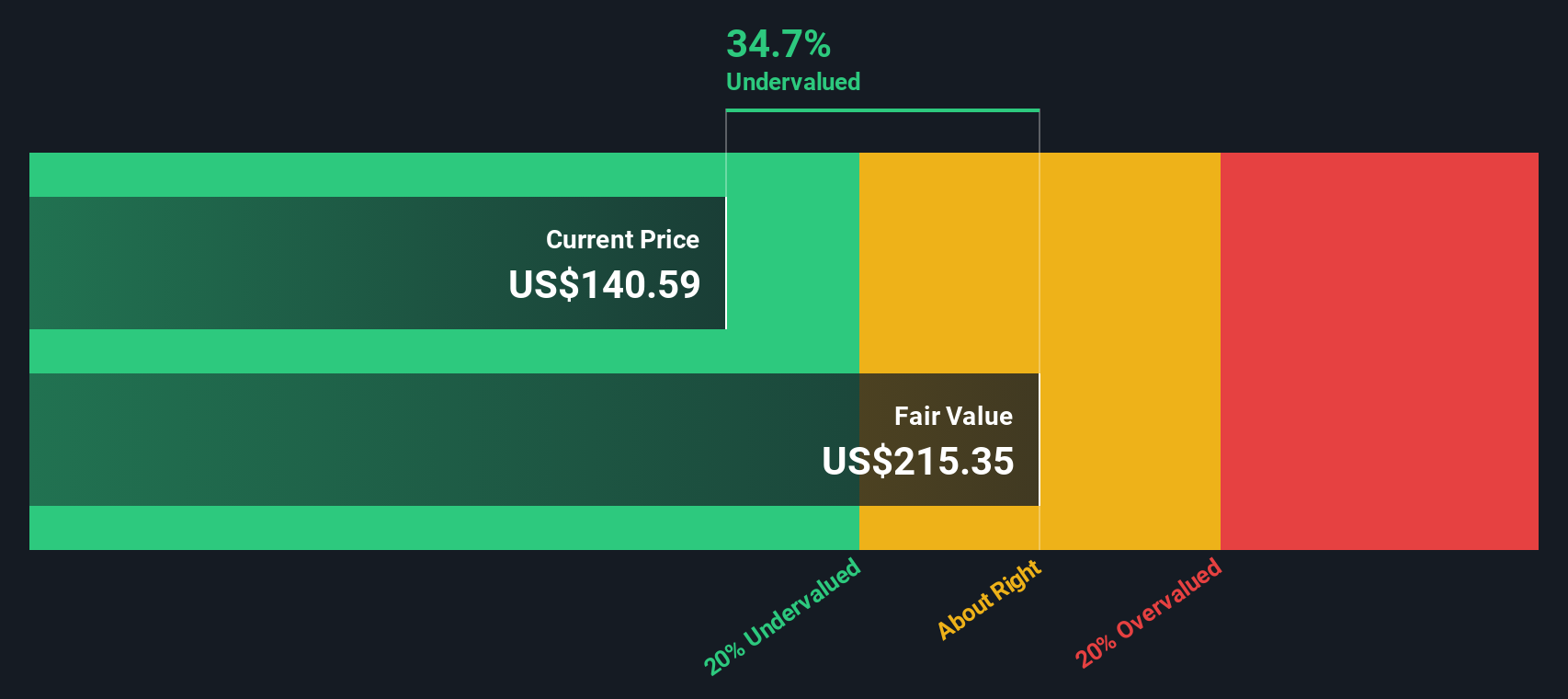

The leadership change at Ross University comes as Covista’s share price, now at $95.59, has seen a 30 day share price return decline of 18.19% and a 1 year total shareholder return decline of 9.74%. However, the 3 year total shareholder return of 133.37% points to strong longer term compounding.

If this healthcare education news has you thinking about where else capital might work hard, it could be a good moment to scan 25 healthcare AI stocks as a fresh set of opportunities.

With Covista trading at $95.59 and sitting at what looks like a meaningful discount to a US$161.50 analyst price target and an indicated intrinsic value gap, you have to ask: is this a potential entry point, or is the market already pricing in future growth?

Price-to-Earnings of 13x: Is it justified?

On top of the DCF and analyst target gaps you have already seen, Covista also screens as inexpensive on earnings, trading on a P/E of 13x while carrying a full value score of 6 out of 6.

The P/E multiple compares the current share price with earnings per share, so a lower number can suggest the market is assigning a modest price to each dollar of profit. For a business focused on healthcare and professional education, with annual revenue of $1,888.83m and net income of $253.98m, this becomes a straightforward way for investors to line up price against an established earnings base.

Here, Covista’s 13x P/E sits below the estimated fair P/E of 18.9x. This is a level our SWS fair ratio work suggests the market could potentially move towards. It also comes in under both the peer average of 14.7x and the wider US Consumer Services industry on 17.7x. That combination points to the market applying a clear discount to Covista’s earnings compared with similar names, despite assessments that earnings quality is high and that profits have grown over the past five years.

Explore the SWS fair ratio for Covista

Result: Price-to-Earnings of 13x (UNDERVALUED)

However, it is still important to monitor potential regulatory changes in higher education and any decline in demand for healthcare and online degree programs, as these factors could negatively affect investor sentiment.

Find out about the key risks to this Covista narrative.

Another View: What The DCF Model Suggests

While the 13x P/E points to value, our DCF model paints an even stronger picture. Covista’s current $95.59 share price sits against an estimated future cash flow value of $233.85. That gap implies a wide margin between market price and modeled cash flows, so how much weight do you give each lens?

Look into how the SWS DCF model arrives at its fair value.

Simply Wall St performs a discounted cash flow (DCF) on every stock in the world every day (check out Covista for example). We show the entire calculation in full. You can track the result in your watchlist or portfolio and be alerted when this changes, or use our stock screener to discover 56 high quality undervalued stocks. If you save a screener we even alert you when new companies match - so you never miss a potential opportunity.

Next Steps

If this combination of value signals and recent share price pressure seems unclear, it may be worth reviewing the details yourself and acting promptly to form your own view, including the 5 key rewards.

Looking for more investment ideas?

If Covista has sharpened your thinking, do not stop here. Broaden your watchlist with focused stock ideas that line up with how you like to invest.

- Target value opportunities by checking companies our screener highlights as 56 high quality undervalued stocks that may warrant a closer look on fundamentals and pricing.

- Prioritise resilience with 81 resilient stocks with low risk scores, so you can focus on businesses our model scores with lower overall risk profiles.

- Spot earlier stage possibilities through a 31 elite penny stocks with strong financials list that surfaces smaller names with specific financial criteria.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

Have feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team@simplywallst.com