- LIVE QUOTES

- LEARN

- HELP

Nasdaq

Nasdaq Wall Street Journal

Wall Street JournalEN

Assessing Watts Water Technologies (WTS) Valuation After Strong 2025 Results And Upbeat 2026 Outlook

Why Watts Water Technologies (WTS) is on investors’ radar right now

Watts Water Technologies (WTS) has drawn fresh attention after reporting fourth quarter and full year 2025 results, along with an outlook for 2026 that points to higher reported net sales.

The combination of recent earnings, management’s 2026 guidance, and a series of capital allocation moves, including dividends and buybacks, has also coincided with analysts lifting their revenue and earnings forecasts for the company.

See our latest analysis for Watts Water Technologies.

Watts Water Technologies’ recent earnings beat, ongoing buybacks, confirmed dividend and active acquisition plans have coincided with a 10.8% 1 month share price return and a 52.2% 1 year total shareholder return. This suggests that momentum has been building over both shorter and longer periods.

If this kind of compounding story interests you, it is worth broadening your search and checking out 24 power grid technology and infrastructure stocks as another way to find companies linked to essential infrastructure themes.

With the shares up strongly over 1 year and the last close only about 3% below the average analyst price target of $338.56, the key question now is whether Watts Water is still mispriced or whether the market is already pricing in future growth.

Most Popular Narrative: 12.6% Overvalued

Compared with the fair value estimate of $292.50, Watts Water Technologies’ last close at $329.48 sits above what the most followed narrative sees as justified, which is built using a discount rate of 8.32%.

The accelerating rollout and success of Nexa, Watts' intelligent water management platform, positions the company to capture the growing demand for advanced, data-driven water conservation, efficiency, and regulatory compliance solutions, which is expected to drive higher-margin, recurring revenue and support long-term earnings and margin expansion.

Curious how a water hardware company ends up priced like a growth compounder? The narrative leans heavily on future margins, steady revenue compounding and a premium earnings multiple to tie it all together.

Result: Fair Value of $292.50 (OVERVALUED)

Have a read of the narrative in full and understand what's behind the forecasts.

However, you also have to weigh softer European demand and tariff swings, which could pressure volumes and margins if pricing power or cost controls fall short.

Find out about the key risks to this Watts Water Technologies narrative.

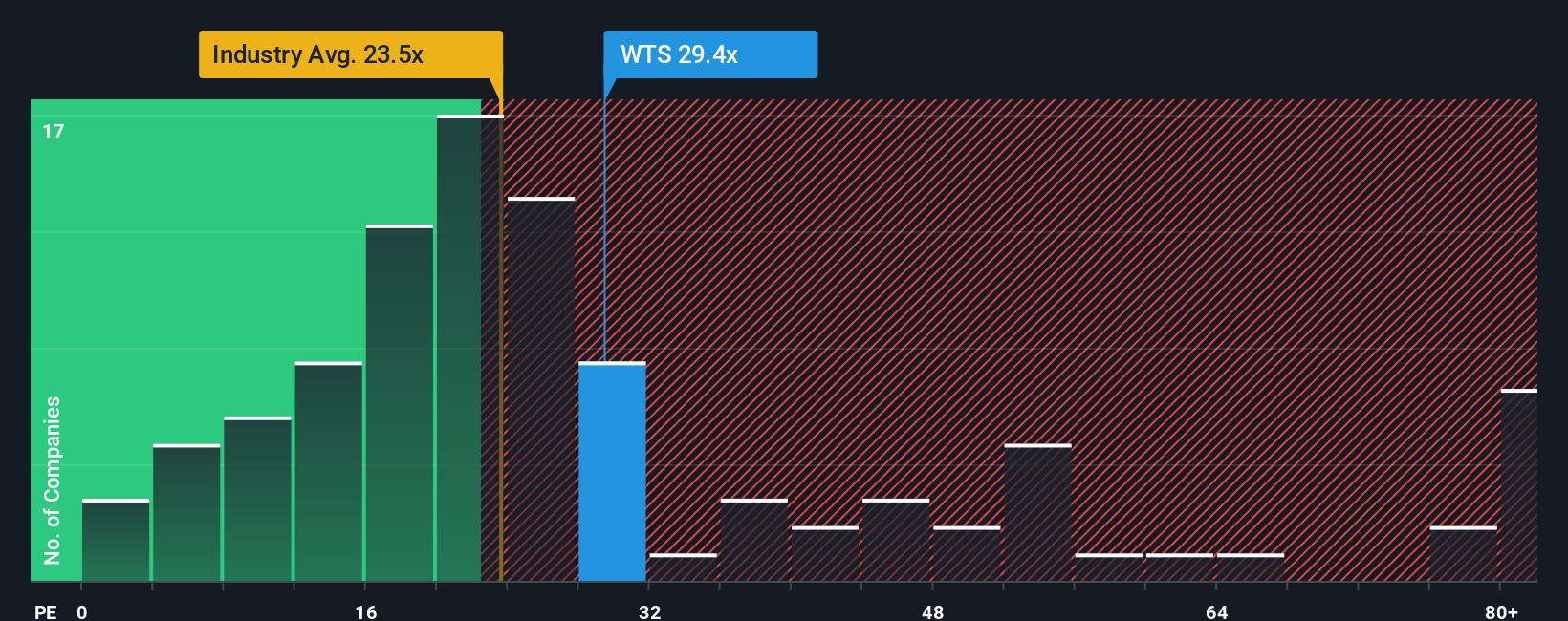

Another Angle on Value: P/E Tells a Different Story

Our DCF view pegs Watts Water at about 12.6% above fair value. The current P/E of 32.2x sits below the 38.6x peer average, and above the 29.9x US Machinery group and the 25x fair ratio. That gap hints at both quality and valuation risk, so which side of that trade off matters more to you?

See what the numbers say about this price — find out in our valuation breakdown.

Next Steps

Does this story sound optimistic or cautious to you? Take a closer look at the numbers, weigh the trade offs, and see how our view of 2 key rewards and 1 important warning sign lines up with your own.

Looking for more investment ideas?

If Watts Water has caught your attention, do not stop here. Broaden your watchlist with a few focused stock ideas built from our screener insights.

- Target quality potential by checking out 56 high quality undervalued stocks, which pairs solid fundamentals with prices that may not fully reflect their underlying business strengths.

- Strengthen your income stream by reviewing 13 dividend fortresses, a hand picked set of companies offering 5%+ yields with an emphasis on stability.

- Lower your stress level by scanning 81 resilient stocks with low risk scores, highlighting resilient names that score well on our risk checks and balance sheet metrics.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

Have feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team@simplywallst.com