- LIVE QUOTES

- LEARN

- HELP

Nasdaq

Nasdaq Wall Street Journal

Wall Street JournalEN

A Look At Darling Ingredients (DAR) Valuation As Profit Falls Despite Higher Full Year Sales

Darling Ingredients (DAR) has released its fourth quarter and full-year results, reporting sales of US$1,709.8 million for the quarter and US$6,135.88 million for the year, while net income declined significantly compared with the prior periods.

See our latest analysis for Darling Ingredients.

The earnings release followed a strong share price run, with a 1-month share price return of 28.78% and a 90-day share price return of 49.49%. This helped lift the 1-year total shareholder return to 21.77%, although the 3- and 5-year total shareholder returns remain negative. This suggests that recent momentum is rebuilding after a weaker long-term experience.

If this earnings move has you reassessing opportunities in related areas, it could be a good moment to look at 24 power grid technology and infrastructure stocks as another way to find companies exposed to long-term infrastructure and energy themes.

With sales rising but net income much lower than a year ago, and the share price already up sharply in recent months, the question now is whether Darling Ingredients is still undervalued or if the market is already pricing in future growth.

Most Popular Narrative: 7.4% Overvalued

At a last close of $50.96 versus a narrative fair value of about $47.46, the widely followed view suggests the market price is running ahead of that estimate.

Policy changes favoring U.S.-sourced renewable diesel feedstocks (higher domestic fat prices, reduced foreign competition) and increasing U.S. biofuel mandates are expected to structurally expand demand and improve pricing power in Darling's Feed and Fuel segments. This is described as a driver of higher revenue and margin expansion through 2026 and beyond. Geographic and product diversification, especially through integration in Brazil and expansion in Europe and the U.K., is presented as positioning Darling to benefit from population growth and rising protein consumption globally. It is also cited as providing operational flexibility and stability that is expected to support both top-line growth and resilient net margins.

Want to see what is described as being baked into that valuation gap? The narrative focuses on earnings compounding, steadier margins, and a future earnings multiple that is characterized as not especially aggressive on those projections.

Result: Fair Value of $47.46 (OVERVALUED)

Have a read of the narrative in full and understand what's behind the forecasts.

However, there is still the risk that ongoing regulatory uncertainty around renewable fuels, or higher and more volatile feedstock costs, could quickly undermine the current bullish narrative.

Find out about the key risks to this Darling Ingredients narrative.

Another View: Cash Flows Point the Other Way

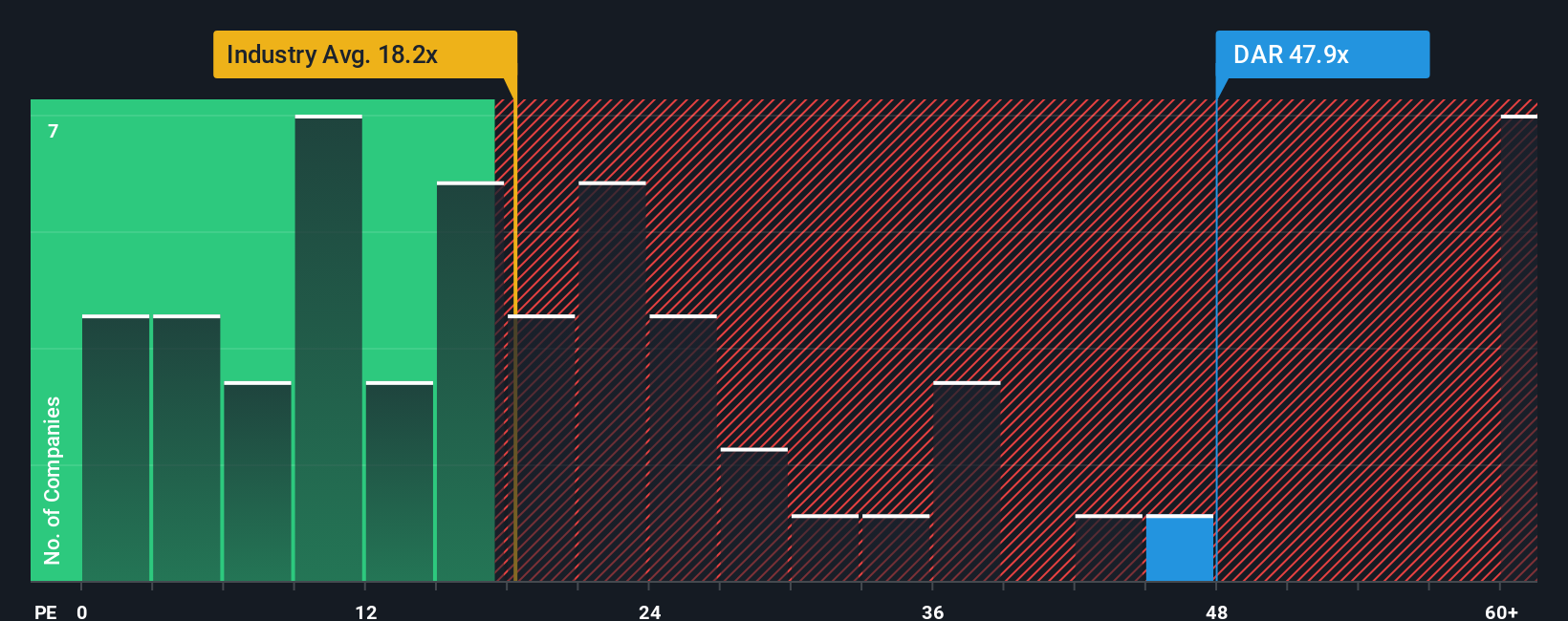

Analysts looking at ratios see Darling Ingredients on a rich P/E of 128.4x, compared with 24.4x for the US Food industry and a fair ratio of 91.4x. That gap suggests meaningful valuation risk if sentiment cools. The key question is whether you think the earnings outlook really justifies paying this kind of premium.

See what the numbers say about this price — find out in our valuation breakdown.

Simply Wall St performs a discounted cash flow (DCF) on every stock in the world every day (check out Darling Ingredients for example). We show the entire calculation in full. You can track the result in your watchlist or portfolio and be alerted when this changes, or use our stock screener to discover 55 high quality undervalued stocks. If you save a screener we even alert you when new companies match - so you never miss a potential opportunity.

Next Steps

With mixed signals across earnings, valuation, and sentiment, it makes sense to move quickly and test the numbers yourself before opinions harden. Our work already highlights that the company carries both risks investors are watching and rewards they are optimistic about. You can weigh these in detail by checking out 2 key rewards and 3 important warning signs.

Looking for more investment ideas?

If this update has sharpened your focus, do not stop here. The real edge often comes from comparing several quality ideas side by side.

- Spot potential value opportunities early by scanning our list of 55 high quality undervalued stocks that pair solid fundamentals with prices that may not fully reflect them yet.

- Strengthen the defensive side of your portfolio by reviewing companies in the solid balance sheet and fundamentals stocks screener (44 results) that put balance sheet resilience front and center.

- Aim for a steady stream of cash returns by checking out the 13 dividend fortresses that focus on higher yielding companies with income potential.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

Have feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team@simplywallst.com