- LIVE QUOTES

- LEARN

- HELP

Nasdaq

Nasdaq Wall Street Journal

Wall Street JournalEN

A Look At Casey's General Stores (CASY) Valuation After Q2 Earnings Growth And Store Expansion

Casey's General Stores (CASY) is back in focus after reporting 14% earnings growth in Q2 fiscal 2026, alongside a 9% rise in store count, with management reiterating expectations for mid teen EBITDA growth.

See our latest analysis for Casey's General Stores.

The recent Q2 update, dividend payment of US$0.57 per share, and February share price move that saw Casey's touch an intraday high near its 52 week peak all sit against a strong backdrop. A 90 day share price return of 19.61% and a 1 year total shareholder return of 56.97% suggest that momentum has been building rather than fading.

If this kind of momentum has you looking beyond a single name, it could be a good time to check out 23 top founder-led companies as you think about what else belongs on your watchlist.

With earnings up 14%, a 9% larger store base, and the stock hovering near its 52 week high, you have to ask whether Casey's is still trading below its intrinsic value or if the market is already pricing in future growth.

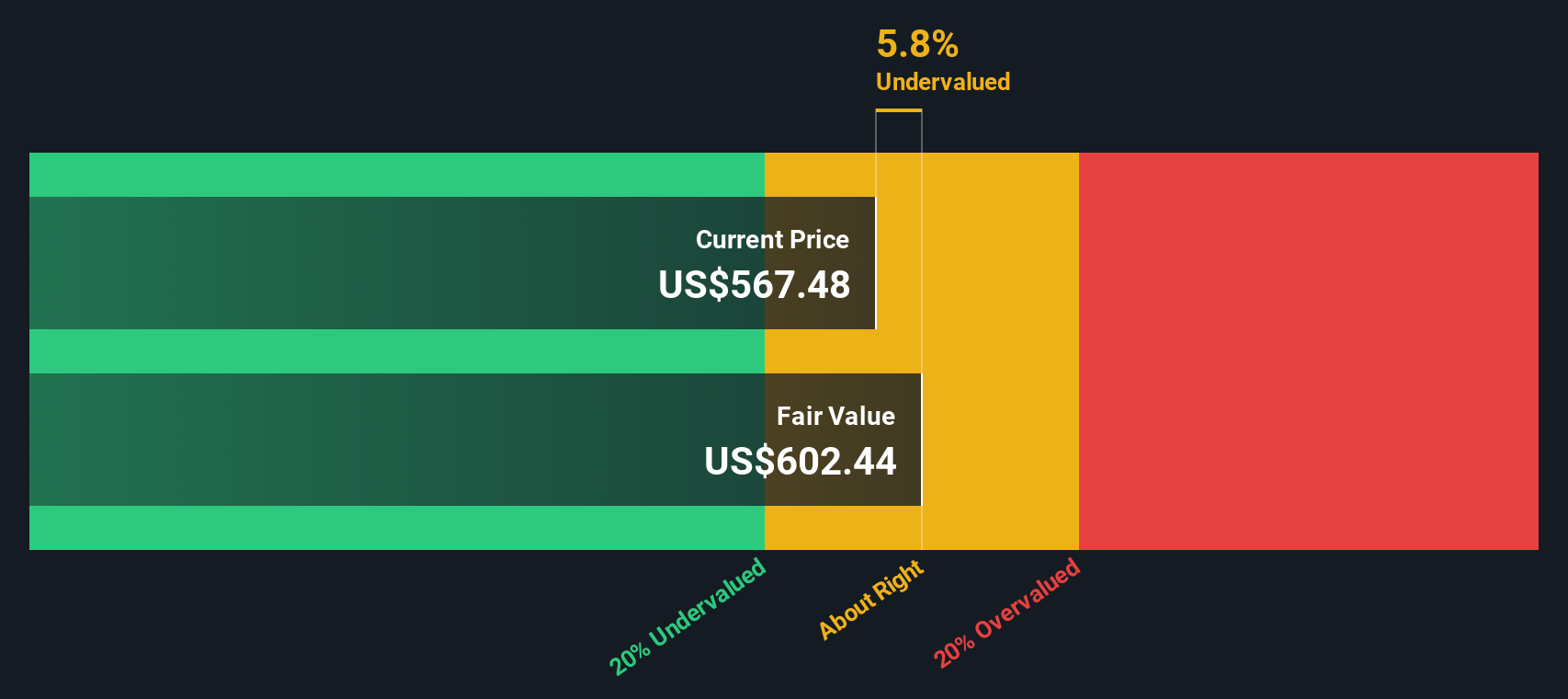

Most Popular Narrative: 11% Overvalued

With Casey's last closing at $665.86 versus a narrative fair value of $600, the current price sits above what that widely followed view suggests. The reasoning behind that gap comes down to how earnings, margins, and discount rates are expected to play together over the next few years.

Analysts expect earnings to reach $760.7 million (and earnings per share of $20.72) by about September 2028, up from $581.7 million today. The analysts are largely in agreement about this estimate.

Curious what kind of revenue climb, margin lift, and future P/E multiple are baked into that target? The full narrative lays out a tight set of assumptions, grounded in detailed forecasts and a specific discount rate that ties it all back to today.

Result: Fair Value of $600 (OVERVALUED)

Have a read of the narrative in full and understand what's behind the forecasts.

However, there is still the chance that slower synergy from acquisitions or pressure on fuel-driven traffic could challenge the upbeat earnings path analysts are expecting.

Find out about the key risks to this Casey's General Stores narrative.

Another View: Cash Flows Point To Undervaluation

The narrative fair value of $600 suggests Casey's General Stores might be 11% overvalued, but our DCF model offers a different perspective. Under that approach, the shares appear to be around 5% below an estimated future cash flow value of $700.75. Which lens do you think aligns better with your thesis?

Look into how the SWS DCF model arrives at its fair value.

Simply Wall St performs a discounted cash flow (DCF) on every stock in the world every day (check out Casey's General Stores for example). We show the entire calculation in full. You can track the result in your watchlist or portfolio and be alerted when this changes, or use our stock screener to discover 55 high quality undervalued stocks. If you save a screener we even alert you when new companies match - so you never miss a potential opportunity.

Next Steps

If this mix of optimism and questions has you on the fence, now is a good time to look through the numbers yourself and decide where you stand. To weigh the potential upside against the key concerns, take a closer look at the 3 key rewards and 1 important warning sign.

Looking for more investment ideas?

If Casey's has you thinking bigger, do not stop with one stock. Broaden your watchlist with a few focused sets of ideas built from hard numbers.

- Target potential mispricings by scanning our list of 55 high quality undervalued stocks that pair solid fundamentals with prices that may not fully reflect their current metrics.

- Strengthen your income stream by reviewing 13 dividend fortresses, a group of companies offering higher yields that could appeal if regular cash returns matter to you.

- Prioritise resilience by checking 81 resilient stocks with low risk scores, which focuses on businesses with lower risk scores so you are not only chasing upside but also thinking about capital protection.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

Have feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team@simplywallst.com