- LIVE QUOTES

- LEARN

- HELP

Nasdaq

Nasdaq Wall Street Journal

Wall Street JournalEN

A Look At Callaway Golf (CALY) Valuation After Earnings Miss And Cautious 2026 Outlook

Callaway Golf (CALY) is under pressure after fourth quarter revenue missed analyst expectations, and management issued 2026 guidance that points to lower sales and profitability than the market was looking for.

See our latest analysis for Callaway Golf.

The disappointing quarter and softer 2026 guidance have reversed much of Callaway Golf's recent momentum, with a 1 day share price return of a 15.05% decline to US$12.59 and a 7 day share price return of a 14.06% decline, even though the 90 day share price return of a 34.51% gain and 1 year total shareholder return of a 68.54% gain still point to a strong rebound off longer term total shareholder return declines over 3 and 5 years.

If this earnings setback has you reassessing where growth and income might come from next, it could be a good moment to look at 21 elite gold producer stocks as potential alternatives in the broader leisure and commodities space.

With the shares now back at US$12.59 and trading at a discount to some analyst targets and intrinsic estimates, you have to ask: is Callaway Golf being undervalued after this reset, or is the market already pricing in its future growth?

Most Popular Narrative: 1% Overvalued

At $12.59, Callaway Golf sits just above its most widely followed fair value estimate of $12.50, which is built off detailed long term forecasts.

The analysts have a consensus price target of $10.5 for Topgolf Callaway Brands based on their expectations of its future earnings growth, profit margins and other risk factors. However, there is a degree of disagreement amongst analysts, with the most bullish reporting a price target of $13.0, and the most bearish reporting a price target of just $9.0.

Curious what sits behind that tight fair value band? The narrative leans on specific assumptions for revenue trends, margin rebuild, and the earnings multiple the market might be willing to pay.

Result: Fair Value of $12.50 (ABOUT RIGHT)

Have a read of the narrative in full and understand what's behind the forecasts.

However, you still need to weigh risks such as pressure from discounting at Topgolf and higher tariffs, which could squeeze margins and challenge those fair value assumptions.

Find out about the key risks to this Callaway Golf narrative.

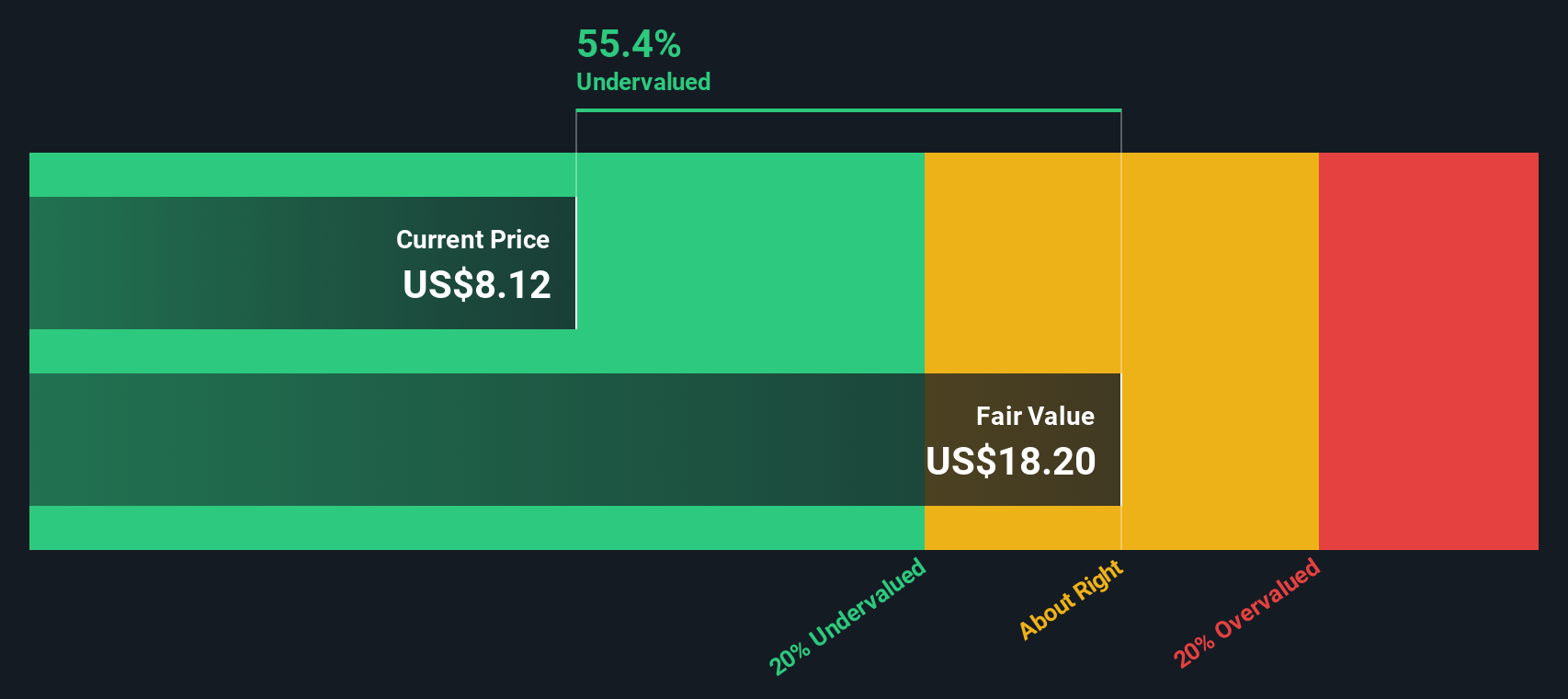

Another Take: DCF Sees Meaningful Upside

The earlier narrative suggests Callaway Golf is about 1% overvalued at $12.59 versus a $12.50 fair value, but our DCF model paints a different picture. It points to a value of $23.87 per share, which implies the current price could be materially below the long term cash flow estimate. Which story do you think fits your expectations better?

Look into how the SWS DCF model arrives at its fair value.

Simply Wall St performs a discounted cash flow (DCF) on every stock in the world every day (check out Callaway Golf for example). We show the entire calculation in full. You can track the result in your watchlist or portfolio and be alerted when this changes, or use our stock screener to discover 55 high quality undervalued stocks. If you save a screener we even alert you when new companies match - so you never miss a potential opportunity.

Next Steps

Feeling torn between the mixed signals in this story? Take a closer look at the underlying data now and carefully weigh the trade off between 3 key rewards and 1 important warning sign.

Looking for more investment ideas?

If this update has sharpened your focus, do not stop here. Fresher opportunities could sit just a screener away and you may not want to miss them.

- Target quality at a discount by scanning for companies our models flag in 55 high quality undervalued stocks that combine attractive pricing with solid fundamentals.

- Prioritise resilience by checking out 81 resilient stocks with low risk scores, highlighting businesses with lower risk scores that may suit a steadier approach to equity investing.

- Get ahead of the crowd by reviewing our screener containing 24 high quality undiscovered gems, a set of under the radar names with fundamentals that could warrant a closer look.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

Have feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team@simplywallst.com