- LIVE QUOTES

- LEARN

- HELP

Nasdaq

Nasdaq Wall Street Journal

Wall Street JournalEN

A Look At Grab Holdings (NasdaqGS:GRAB) Valuation After Net Profit, Double Digit Growth And US$500m Buyback

Grab Holdings (GRAB) just packed several key events into one week, combining its first full year of net profit, double digit revenue growth, a new US$500 million buyback, and an exclusive lidar distribution deal.

See our latest analysis for Grab Holdings.

Despite the strong earnings, buyback announcement and lidar deal, the share price is down 22.2% over the past 90 days, and the 1 year total shareholder return is 22.1% lower. However, the 3 year total shareholder return remains positive, which suggests recent momentum has been fading after earlier gains.

If this mix of growth news and share price weakness has you comparing options, it could be a good moment to scan 23 top founder-led companies for fresh ideas beyond Grab.

So with Grab now generating net profit, revenue growth above 10% and a fresh US$500 million buyback, yet a share price that has slid over recent months, is this weakness an opening or is future growth already priced in?

Most Popular Narrative: 49.6% Undervalued

According to the most followed narrative for Grab Holdings, the fair value sits at $8.20, almost double the recent $4.13 close. This puts the latest results and buyback in a very different light.

In reality, Grab is:

• Dominant in mobility and delivery, with a structural localisation moat.

• Building high-margin fintech and advertising businesses with Alipay-like upside.

• Maintaining a fortress balance sheet with over 30% net cash available for further regional expansion.

• Institutionally backed by Uber, SoftBank, Tiger Global, and Toyota.

• Founder-led with proven operating discipline.

Want to see what is driving that near 50% gap to fair value? The narrative leans heavily on compounding revenue, rising margins and a rich future earnings multiple. Curious which combinations of growth, profitability and valuation are doing the heavy lifting in that $8.20 figure? The full story is in the detailed assumptions behind that model.

Result: Fair Value of $8.20 (UNDERVALUED)

Have a read of the narrative in full and understand what's behind the forecasts.

However, this hinges on thin profit margins and heavy share dilution, so any setback in profitability or tougher Indonesian regulation could quickly challenge that undervalued story.

Find out about the key risks to this Grab Holdings narrative.

Another Way To Look At Value

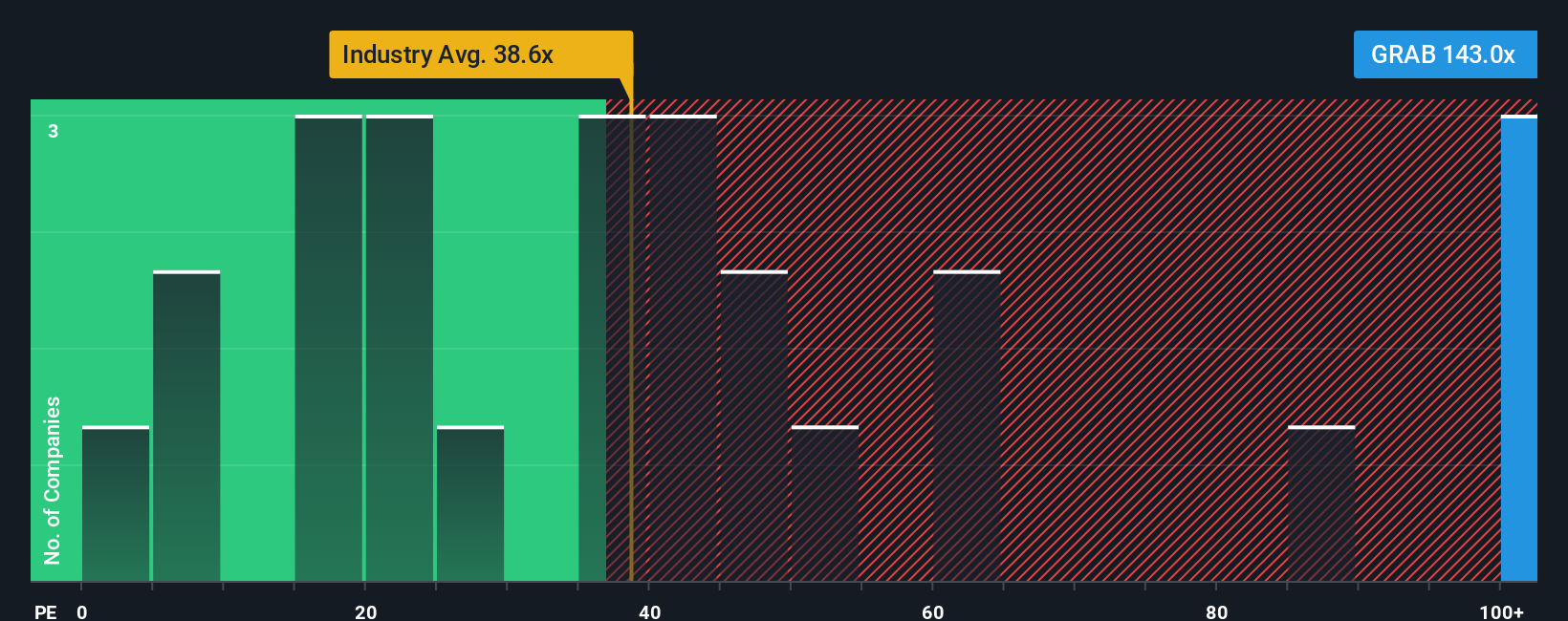

While the user narrative emphasizes long term growth and a higher fair value, our multiples view is much less generous. Grab trades on a P/E of 63x, compared with a fair ratio of 25.2x, the US Transportation industry at 36.9x, and peers at 26.5x. That kind of premium can signal valuation risk if expectations slip, so how much of the story do you think is already in the price?

See what the numbers say about this price — find out in our valuation breakdown.

Next Steps

If this mix of optimism and warning signs feels finely balanced, take a closer look at the numbers yourself and decide quickly where you stand. You can start with 4 key rewards and 1 important warning sign.

Looking for more investment ideas?

If you stop at Grab, you might miss other opportunities that suit your style, so use the screener to line up your next potential moves.

- Spot resilient names that aim to weather bumps in the market by checking out 82 resilient stocks with low risk scores and see which businesses keep risk scores in focus.

- Hunt for companies with solid fundamentals and strong financial footing using the solid balance sheet and fundamentals stocks screener (44 results) to see who keeps debt and cash flow in tighter shape.

- Zero in on potential underpriced opportunities with 55 high quality undervalued stocks, where the screener filters for quality businesses that trade below their estimated worth.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

Have feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team@simplywallst.com