- LIVE QUOTES

- LEARN

- HELP

Nasdaq

Nasdaq Wall Street Journal

Wall Street JournalEN

How Investors Are Reacting To NOV (NOV) Earnings Miss, Impairments, Buybacks And Tighter M&A Focus

- In early February 2026, NOV Inc. reported fourth-quarter 2025 results showing quarterly revenue of US$2,277 million, a net loss of US$78 million, and US$70 million of goodwill and long-lived asset impairments, alongside guidance for a 1% to 3% year-over-year revenue decline in the first quarter of 2026.

- At the same time, management highlighted that tighter acquisition criteria, a completed buyback of 36,959,834 shares for US$544.64 million, and a focus on portfolio efficiency are intended to support higher-return growth, including carefully selected M&A opportunities.

- Against this backdrop of weaker earnings and stricter deal standards, we’ll assess how NOV’s renewed M&A focus may alter its investment narrative.

We've uncovered the 13 dividend fortresses yielding 5%+ that don't just survive market storms, but thrive in them.

NOV Investment Narrative Recap

To own NOV today, you need to believe its portfolio of oilfield equipment, services, and emerging energy technologies can still produce attractive returns despite cyclical headwinds and margin pressure. The latest quarter’s net loss and 1% to 3% revenue decline guidance keep near term earnings risk front and center, while the key short term catalyst remains whether NOV can stabilize margins as pricing pressure, tariffs, and lumpy orders continue to challenge profitability.

Against that backdrop, the completed repurchase of 36,959,834 shares for US$544.64 million stands out. It tightens the share base just as NOV works through weaker earnings and goodwill impairments, potentially amplifying the impact of any future earnings recovery. However, if order volatility or prolonged softness in key markets persists, this capital return could limit flexibility exactly when NOV may need balance sheet strength most to support its renewed M&A ambitions and portfolio efficiency efforts.

Yet while NOV is leaning into disciplined M&A and buybacks, investors should also weigh the risk that accelerating energy transition and policy shifts could reshape demand for its core offerings...

Read the full narrative on NOV (it's free!)

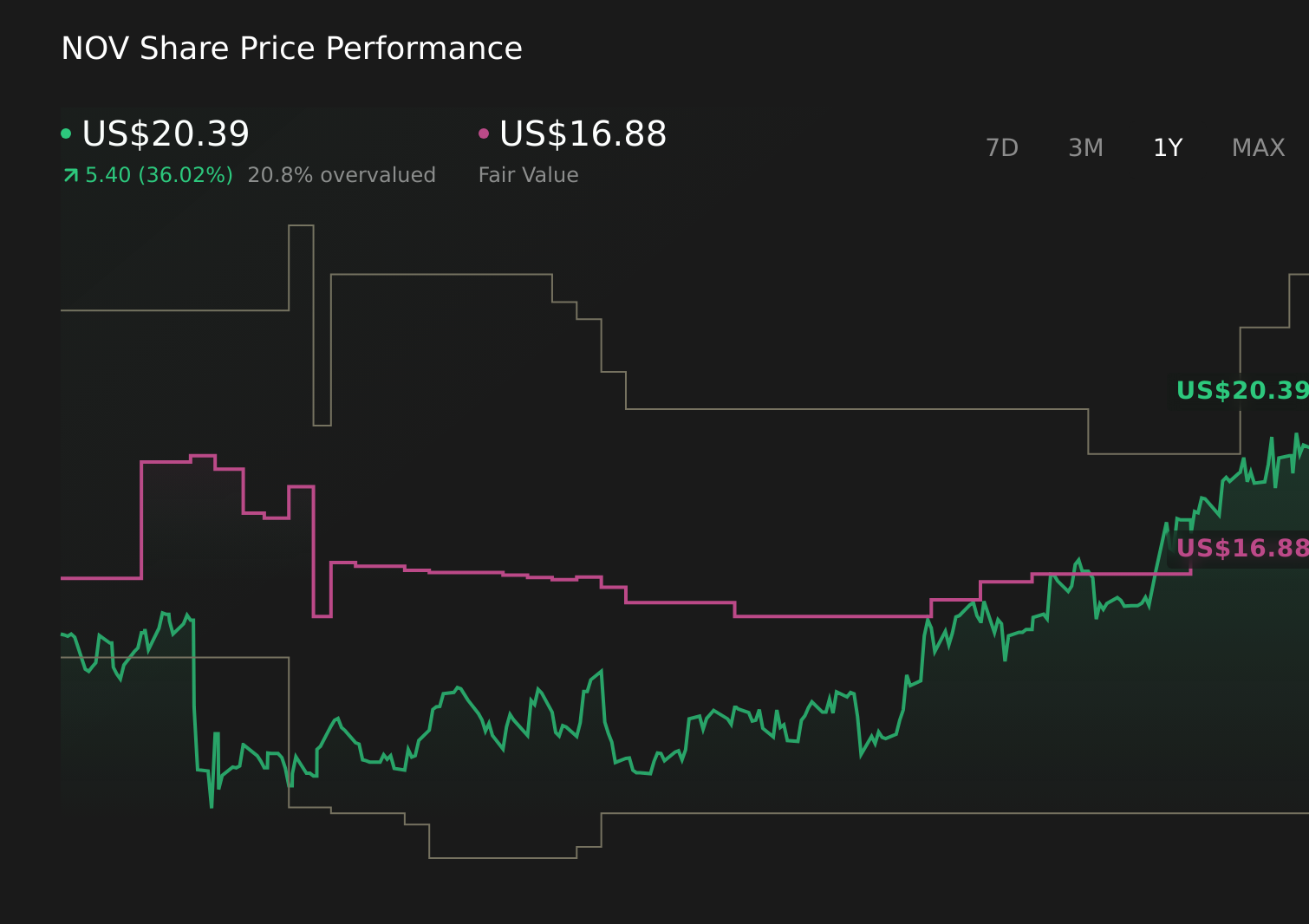

NOV's narrative projects $9.0 billion revenue and $546.3 million earnings by 2028.

Uncover how NOV's forecasts yield a $16.88 fair value, a 12% downside to its current price.

Exploring Other Perspectives

Before this update, the most optimistic analysts were modeling NOV’s earnings rising to about US$565 million by 2028, but the latest loss and tighter guidance may test that view and your comfort with very different opinions on how much regulatory and energy transition risks could slow that path.

Explore 6 other fair value estimates on NOV - why the stock might be worth as much as 51% more than the current price!

Reach Your Own Conclusion

Disagree with existing narratives? Extraordinary investment returns rarely come from following the herd, so go with your instincts.

- A great starting point for your NOV research is our analysis highlighting 2 key rewards and 3 important warning signs that could impact your investment decision.

- Our free NOV research report provides a comprehensive fundamental analysis summarized in a single visual - the Snowflake - making it easy to evaluate NOV's overall financial health at a glance.

Curious About Other Options?

Our top stock finds are flying under the radar-for now. Get in early:

- Uncover the next big thing with 29 elite penny stocks that balance risk and reward.

- The best AI stocks today may lie beyond giants like Nvidia and Microsoft. Find the next big opportunity with these 26 smaller AI-focused companies with strong growth potential through early-stage innovation in machine learning, automation, and data intelligence that could fund your retirement.

- Invest in the nuclear renaissance through our list of 85 elite nuclear energy infrastructure plays powering the global AI revolution.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

Have feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team@simplywallst.com