- LIVE QUOTES

- LEARN

- HELP

Nasdaq

Nasdaq Wall Street Journal

Wall Street JournalEN

A Look At GXO Logistics (GXO) Valuation After Q4 Beat And Upgraded Growth Guidance

GXO Logistics (GXO) is back in focus after its fourth quarter and full year 2025 results, paired with 2026 guidance calling for 4% to 5% organic revenue growth and management highlighting margin and technology priorities.

See our latest analysis for GXO Logistics.

Those earnings and guidance updates come on the back of strong share price momentum, with a 36.7% 3 month share price return and 66.2% 1 year total shareholder return. This suggests investors are reassessing growth prospects and risk around GXO’s logistics and automation push.

If this focus on logistics technology has your attention, it could be a good moment to broaden your watchlist with 32 robotics and automation stocks identified by the Simply Wall St screener.

With the share price already up strongly and analysts setting targets near the current level, the key question now is whether GXO is still trading below its fair value or if the market is already pricing in future growth.

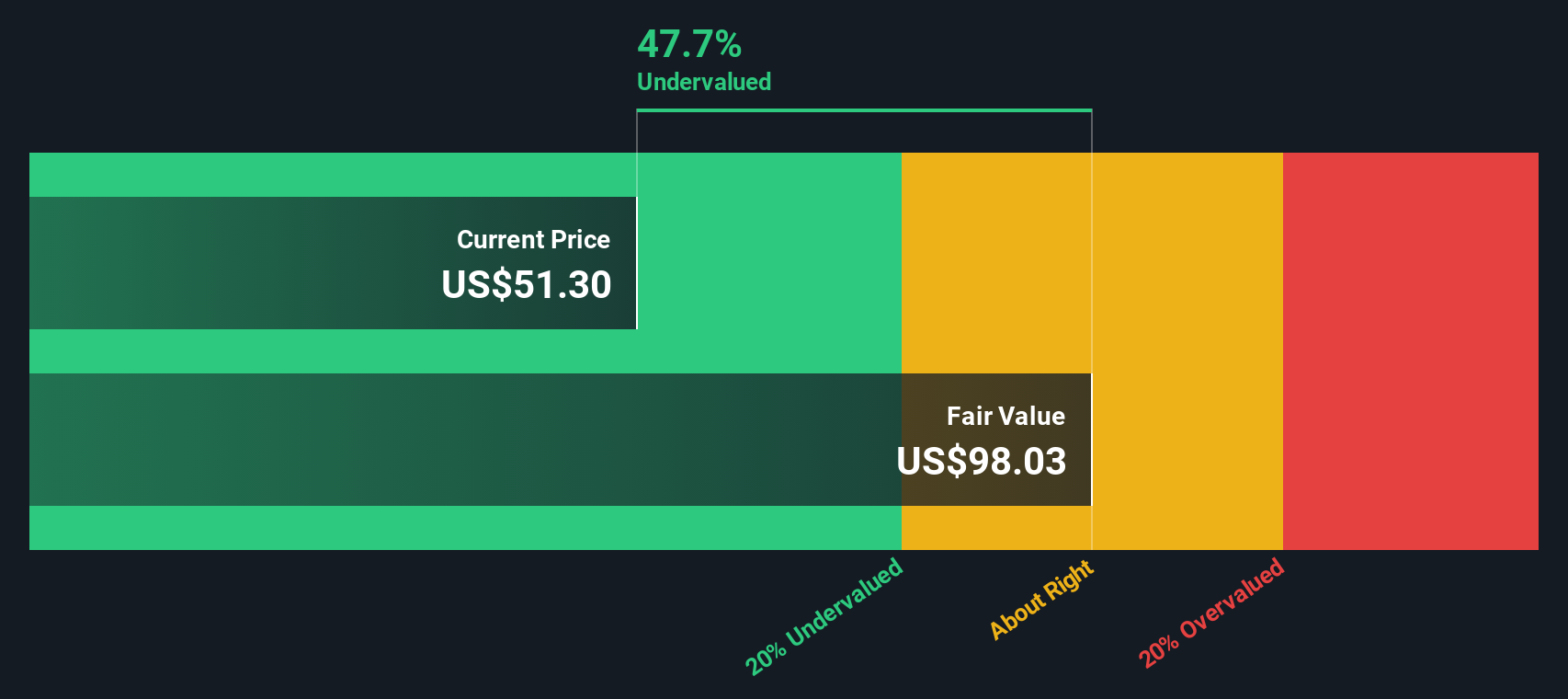

Most Popular Narrative: 1% Undervalued

GXO Logistics' most followed narrative pegs fair value at $66.00, almost in line with the last close of $65.51. This puts the spotlight on the assumptions beneath that tight gap.

The company's focus on long-term, multi-year, blue-chip customer contracts, coupled with record levels of new business wins and high customer retention (mid-90s%), underpins resilient and stable cash flows, reducing earnings volatility and providing a strong foundation for future capital returns and reinvestment.

Curious what kind of revenue path, margin lift and earnings power are built into that fair value, and how long it takes to get there? The full narrative lays out a detailed earnings ramp, revenue trajectory and profit multiple that many investors are using as their reference point.

Result: Fair Value of $66.00 (ABOUT RIGHT)

Have a read of the narrative in full and understand what's behind the forecasts.

However, there is still real execution risk around the Wincanton integration and leadership changes, which could pressure margins and unsettle the current growth narrative.

Find out about the key risks to this GXO Logistics narrative.

Another View: DCF Says Slightly Overvalued

While the popular narrative points to GXO being about 1% undervalued at $66.00, our DCF model comes out a touch lower, at $64.27. With the shares at $65.51, that suggests a small premium. The real question is which set of assumptions you find more realistic.

Look into how the SWS DCF model arrives at its fair value.

Simply Wall St performs a discounted cash flow (DCF) on every stock in the world every day (check out GXO Logistics for example). We show the entire calculation in full. You can track the result in your watchlist or portfolio and be alerted when this changes, or use our stock screener to discover 54 high quality undervalued stocks. If you save a screener we even alert you when new companies match - so you never miss a potential opportunity.

Next Steps

If this mix of strong momentum and tight valuation has you thinking hard about GXO, now is a good time to look through the numbers yourself and weigh both sides of the story before you act, starting with 2 key rewards and 3 important warning signs.

Looking for more investment ideas?

If GXO has sharpened your focus on where capital goes next, do not stop here. Use these idea lists to spin up your next round of research.

- Target stronger balance sheets and cleaner fundamentals by scanning our solid balance sheet and fundamentals stocks screener (44 results) so you can focus on companies with financial room to manoeuvre.

- Hunt for potential value opportunities using the 54 high quality undervalued stocks, which highlights companies our models flag as trading below their assessed worth.

- Stack your watchlist with potential long term income ideas through the 13 dividend fortresses, centred on higher yielding companies that may appeal to cash flow focused investors.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

Have feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team@simplywallst.com