- LIVE QUOTES

- LEARN

- HELP

Nasdaq

Nasdaq Wall Street Journal

Wall Street JournalEN

Peabody Energy (BTU) Valuation Check After New U.S. Coal Support Initiative Spurs Investor Optimism

Peabody Energy (BTU) is back in focus after a new U.S. government initiative supporting coal, including long term federal power purchase agreements and US$175 million earmarked to upgrade coal plants.

See our latest analysis for Peabody Energy.

Even with the recent government support lifting sentiment and a post-announcement bounce, Peabody Energy’s share price return has cooled in the last week and month. However, the 90-day gain of 19.33% and very large 5-year total shareholder return of about 7x suggest longer-term momentum remains strong. Recent earnings showing a full-year net loss of US$52.9 million and the latest quarterly dividend declaration of US$0.075 per share are also in the background as investors reassess Peabody’s risk and income profile alongside the policy tailwind.

If this coal sector news has you thinking about other energy-related themes, it could be a good time to look at 85 nuclear energy infrastructure stocks as another way to source ideas in the wider power transition story.

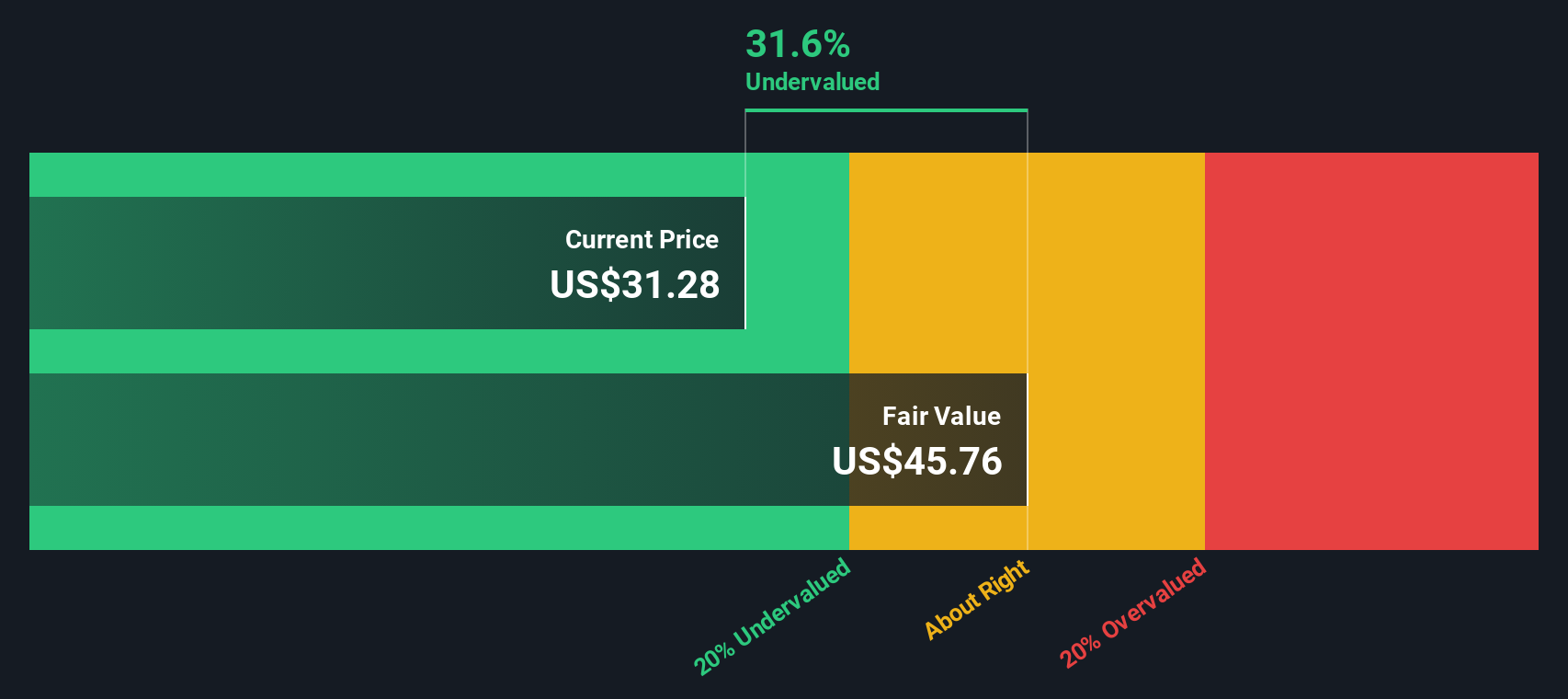

With a 90 day gain above 19%, an intrinsic value model suggesting a large discount, and mixed earnings that include a full year loss, the key question is whether Peabody is genuinely undervalued or if the market already reflects its prospects.

Most Popular Narrative: 100% Undervalued

Peabody Energy's most followed narrative pegs fair value at about $34.80, almost in line with the last close at $34.45, yet still labeling the shares as fully undervalued based on its cash flow potential and discount rate assumptions.

Ongoing global supply discipline exacerbated by limited financing for new mines, regulatory constraints abroad, and the curtailment/closure of legacy assets reinforces supply tightness in both thermal and met coal markets. This positions Peabody, with its diversified and existing asset base, to benefit from structurally higher pricing and more stable long-term revenues.

Curious how that view gets to a higher fair value than the market price today? The narrative leans heavily on revenue growth, richer margins and a lower future earnings multiple. If you want to see exactly how those moving parts fit together, the full narrative lays out the cash flow path in detail.

Result: Fair Value of $34.80 (UNDERVALUED)

Have a read of the narrative in full and understand what's behind the forecasts.

However, the narrative could easily break if global renewable adoption cuts into coal demand faster than expected, or if tighter environmental rules drive up Peabody’s costs.

Find out about the key risks to this Peabody Energy narrative.

Another View: Market Ratios Send A Mixed Signal

Our DCF model suggests Peabody Energy at $34.45 is trading well below an estimated fair value of $98.03, which points to a very large implied discount. Yet the P/S ratio of 1.1x sits above a fair ratio of 0.7x, hinting that cash flow assumptions really carry the load here. Which signal do you trust more?

Look into how the SWS DCF model arrives at its fair value.

Next Steps

Mixed messages on value and risk so far? Take a moment to review the full picture yourself and weigh both sides, including the 2 key rewards and 1 important warning sign.

Looking for more investment ideas?

If you are serious about building a stronger portfolio, do not stop at a single stock story, use the Simply Wall St screener to stack the odds in your favor.

- Target quality at a discount by scanning our 54 high quality undervalued stocks and see which companies currently stand out on both fundamentals and pricing.

- Strengthen your income stream by reviewing 13 dividend fortresses that could help anchor your portfolio with higher yielding names.

- Prioritise resilience with 83 resilient stocks with low risk scores and focus on businesses that score better on stability and financial risk metrics.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

Have feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team@simplywallst.com