- LIVE QUOTES

- LEARN

- HELP

Nasdaq

Nasdaq Wall Street Journal

Wall Street JournalEN

AGCO (AGCO) Valuation Check After Strong Results New Tech Launches And 2026 Earnings Guidance

Earnings and guidance reshape the AGCO (AGCO) story

AGCO (AGCO) has quickly moved into focus after reporting 2025 results, issuing 2026 guidance and detailing progress on digital and autonomous products that together point to meaningful shifts in its underlying business profile.

The latest earnings release showed quarterly sales of US$2,920.2 million and net income of US$95.5 million, compared with a net loss a year earlier, while full year net income reached US$726.5 million on sales of US$10,082 million.

Alongside these figures, AGCO guided 2026 net sales to a range of US$10.4 billion to US$10.7 billion and targeted earnings per share of roughly US$5.50 to US$6.00, giving investors a reference point for the year ahead.

See our latest analysis for AGCO.

AGCO’s recent earnings, 2026 guidance and the World Ag Expo product showcase appear to have reset expectations, with a 30 day share price return of 26.17% and a 1 year total shareholder return of 44.75% suggesting momentum has picked up.

If you are watching how agriculture and automation stories play out, it can be useful to compare AGCO with other equipment and technology names through our screen of 32 robotics and automation stocks.

With AGCO up 26.17% in 30 days and trading around US$140.49, yet still showing an implied intrinsic discount of roughly 20%, you have to ask: is there real value left here, or is the market already baking in future growth?

Most Popular Narrative: 18.6% Overvalued

Against AGCO’s last close at $140.49, the most followed narrative pegs fair value at $118.50. This implies the current price sits above that anchor and rests on a specific earnings and margin path.

The analysts have a consensus price target of $123.769 for AGCO based on their expectations of its future earnings growth, profit margins and other risk factors. However, there is a degree of disagreement amongst analysts, with the most bullish reporting a price target of $145.0, and the most bearish reporting a price target of just $97.0.

Want to see what is baked into that fair value gap? The narrative leans on steady top line growth, fatter margins and a future earnings multiple that assumes consistent execution.

Result: Fair Value of $118.50 (OVERVALUED)

Have a read of the narrative in full and understand what's behind the forecasts.

However, tariff pressure in Europe and a prolonged soft patch for farm equipment demand could easily challenge the margin and earnings path behind that fair value story.

Find out about the key risks to this AGCO narrative.

Another View: Earnings Multiple Points To Underpricing

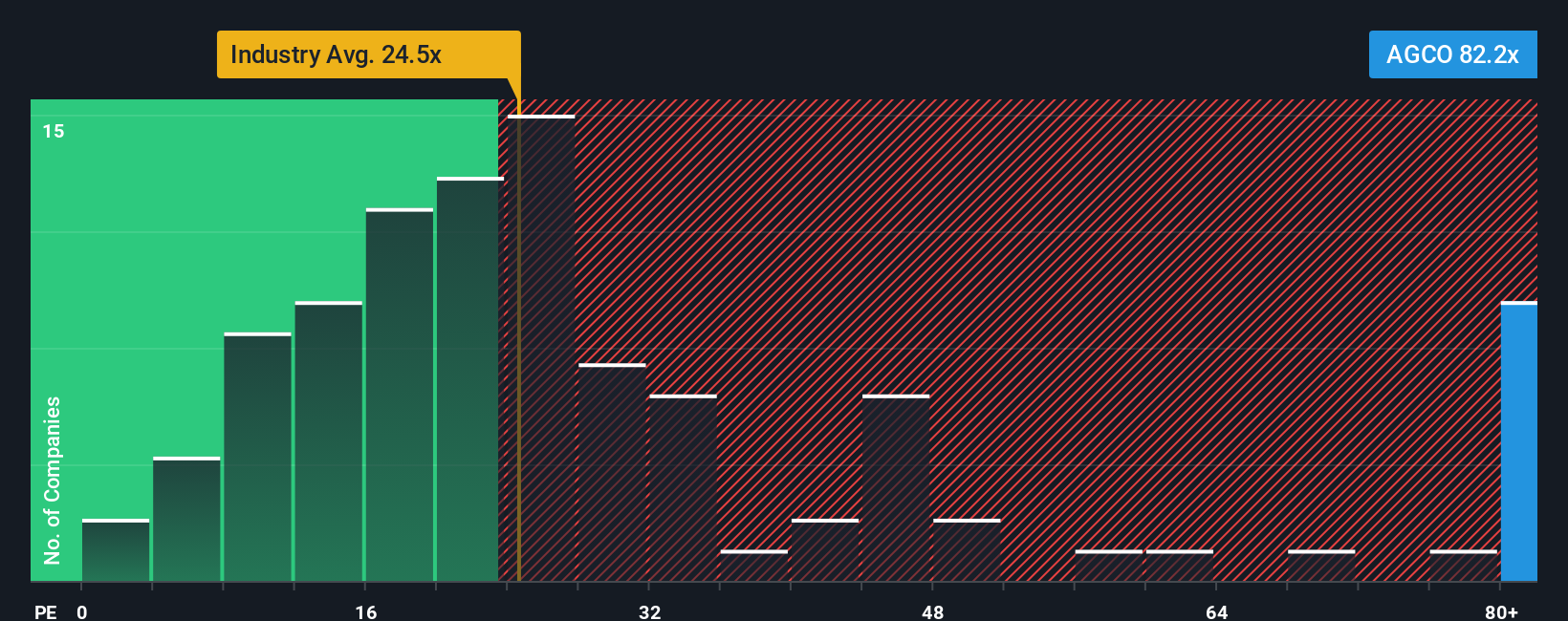

That 18.6% overvalued fair value of $118.50 sits awkwardly next to AGCO’s current P/E of 14x, which compares with a fair ratio of 26.1x and a peer and industry average nearer 24.7x to 29.9x. If the market drifts toward that fair ratio, is the real risk missing further upside?

See what the numbers say about this price — find out in our valuation breakdown.

Build Your Own AGCO Narrative

If you are not fully on board with these narratives or prefer to weigh the numbers yourself, you can pull the data together and shape your own view in a few minutes, then Do it your way

A great starting point for your AGCO research is our analysis highlighting 4 key rewards and 1 important warning sign that could impact your investment decision.

Looking for more investment ideas?

If AGCO has sharpened your interest, do not stop here. Use the Simply Wall Street Screener to surface fresh opportunities that fit your style.

- Spot potential mispricings by scanning our list of 54 high quality undervalued stocks that pair stronger fundamentals with appealing entry points.

- Build a foundation of stability by focusing on companies in our solid balance sheet and fundamentals stocks screener (44 results) that keep debt in check and liquidity in view.

- Hunt for future standouts by working through a screener containing 24 high quality undiscovered gems that many investors may still be overlooking.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

Have feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team@simplywallst.com