- LIVE QUOTES

- LEARN

- HELP

Nasdaq

Nasdaq Wall Street Journal

Wall Street JournalEN

RH (RH) Valuation Check After Softer Inflation Revives Rate Cut Expectations

Macro tailwinds and RH’s recent move

RH (RH) moved after a softer January inflation reading, with shares gaining 5.4% as investors warmed to the idea of potential Federal Reserve rate cuts supporting consumer discretionary names.

This macro backdrop arrived shortly after RH announced its 2026 RH Outdoor Sourcebook, a catalog of more than 420 pages of outdoor collections that reinforces the company’s focus on design, materials, and brand positioning.

See our latest analysis for RH.

That inflation driven jump comes after a choppy spell, with a 30 day share price return of an 11.95% decline contrasting with a 44.87% gain over 90 days. At the same time, the 1 year total shareholder return shows a 46.37% decline, which points to longer term holders still being in the red.

If RH’s recent move has you thinking about where growth and leadership might show up next, it could be worth widening the lens to our screener of 23 top founder-led companies to see what else stands out.

With RH shares moving on macro news, trading near a modest discount to analyst targets and showing a very wide gap to some intrinsic value estimates, the key question is simple: is there a genuine opportunity here or is future growth already baked in?

Most Popular Narrative: 2.5% Undervalued

RH last closed at $205.06, a touch below the most followed fair value estimate of $210.35, which is built on detailed long term earnings and margin assumptions.

The company's plans to monetize assets, including real estate with an estimated equity value of approximately $500 million and excess inventory valued at $200 million to $300 million, could boost cash flow and help in reducing debt, potentially improving net margins and lowering interest expenses.

Curious how a modest 2.5% upside rests on ambitious revenue targets, fatter margins, and a very specific future P/E hurdle, all under an 11% discount rate? The full narrative spells out how these moving parts fit together and what has to go right for RH to justify that $210 fair value.

Result: Fair Value of $210.35 (UNDERVALUED)

Have a read of the narrative in full and understand what's behind the forecasts.

However, those assumptions could be tested if housing demand stays weak or if tariffs and input costs pressure margins more than analysts currently bake into their models.

Find out about the key risks to this RH narrative.

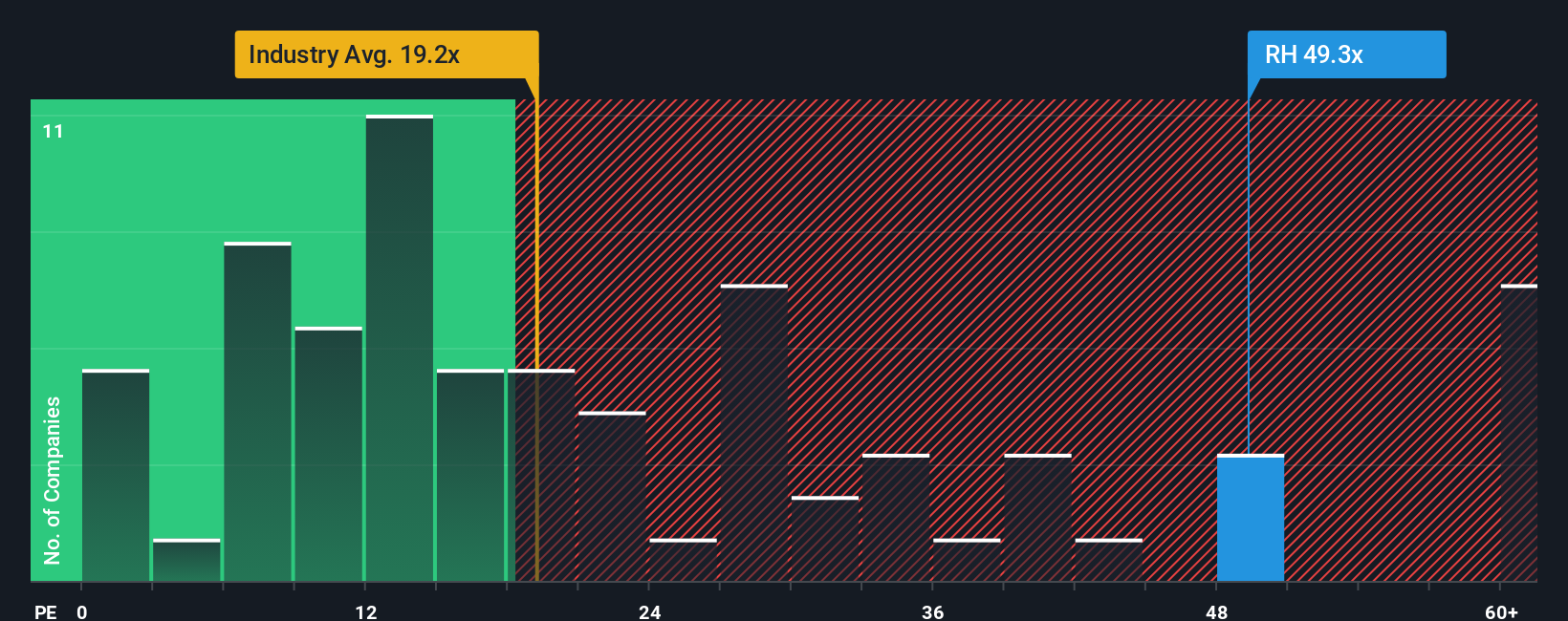

Another View: Valuation Through The P/E Lens

The narrative suggests RH is modestly undervalued, yet the current P/E of 35x tells a different story. That is higher than the US Specialty Retail industry at 21.4x, the peer average at 21x, and even above a fair ratio of 30.5x. For you, that gap might look more like valuation risk rather than hidden upside. Which signal feels more convincing?

See what the numbers say about this price — find out in our valuation breakdown.

Build Your Own RH Narrative

If you look at the numbers and come to a different conclusion, or simply want to stress test the assumptions yourself, you can build a version that reflects your own view in just a few minutes, Do it your way.

A great starting point for your RH research is our analysis highlighting 3 key rewards and 2 important warning signs that could impact your investment decision.

Looking for more investment ideas?

If you are weighing what comes next after RH, do not stop here. Broaden your watchlist with a few focused stock ideas built from our screeners.

- Spot opportunities that combine quality and a sensible entry point by checking out our 54 high quality undervalued stocks drawn from companies with strong fundamentals and constrained prices.

- Strengthen your focus on capital protection by reviewing a curated set of 83 resilient stocks with low risk scores that score well on our risk checks.

- Get ahead of the crowd by scanning a screener containing 24 high quality undiscovered gems that flags lesser known names with solid underlying metrics.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

Have feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team@simplywallst.com