- LIVE QUOTES

- LEARN

- HELP

Nasdaq

Nasdaq Wall Street Journal

Wall Street JournalEN

Assessing Mercury Systems (MRCY) Valuation After Improved Q2 Sales And Narrower Loss

Mercury Systems (MRCY) has drawn fresh attention after reporting second quarter and six month results to December 26, 2025, with higher sales and a smaller net loss than the prior year.

See our latest analysis for Mercury Systems.

The earnings update comes after a volatile stretch for Mercury Systems, with a 30 day share price return of 20.05% decline, a 90 day share price return of 21.22% gain, and a 1 year total shareholder return of 85.29%. This suggests that longer term momentum has been positive even as shorter term sentiment has cooled.

If this earnings move has you looking beyond a single defense electronics name, it could be a good moment to check out 25 power grid technology and infrastructure stocks as potential beneficiaries of similar spending themes.

With sales growing, losses narrowing and the share price already up strongly over 1 year, the key question now is whether Mercury Systems at about US$82 is still mispriced or if the market is already banking on further improvement.

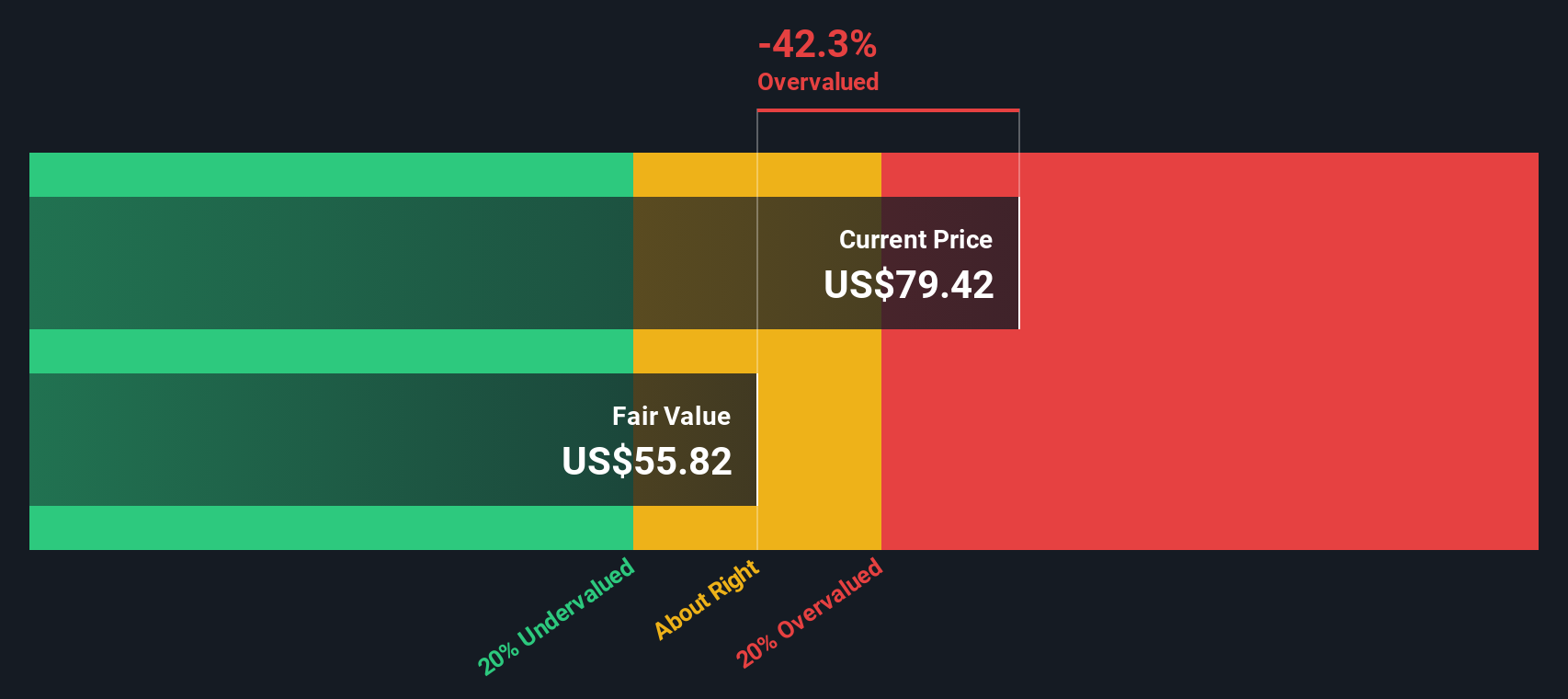

Most Popular Narrative: 4.2% Undervalued

Mercury Systems last closed at about $82, slightly under the most followed fair value estimate of $86. This frames the recent results in a tighter valuation range.

Expanding penetration into programs that require secure, high-performance embedded processing and open-architecture modular solutions positions Mercury to benefit from the defense sector's shift toward greater digitization and AI/ML adoption. This supports higher-margin, higher-value contracts and improved long-term gross and net margins.

Curious what kind of revenue path and margin lift would justify that fair value and almost triple digit future earnings multiple assumption? The full narrative lays out the growth pacing, profitability targets and timeframes that sit behind the $86 figure, and how much improvement needs to show up before that price really makes sense.

Result: Fair Value of $86 (UNDERVALUED)

Have a read of the narrative in full and understand what's behind the forecasts.

However, there is still the overhang of low margin legacy contracts and uncertainty around future defense budgets, which could challenge the upbeat fair value story.

Find out about the key risks to this Mercury Systems narrative.

Another View: Cash Flows Paint A Tougher Picture

While the popular narrative points to a fair value of $86 and describes Mercury Systems as undervalued, our DCF model lands closer to $69 per share, which is below the current $82.36 price. If cash flows are the primary focus, is the recent optimism already more than priced in?

Look into how the SWS DCF model arrives at its fair value.

Simply Wall St performs a discounted cash flow (DCF) on every stock in the world every day (check out Mercury Systems for example). We show the entire calculation in full. You can track the result in your watchlist or portfolio and be alerted when this changes, or use our stock screener to discover 54 high quality undervalued stocks. If you save a screener we even alert you when new companies match - so you never miss a potential opportunity.

Build Your Own Mercury Systems Narrative

If you see the story differently or like to work from your own numbers, you can pull the data, test your assumptions and Do it your way in just a few minutes.

A good starting point is our analysis highlighting 1 key reward investors are optimistic about regarding Mercury Systems.

Ready For More Investment Ideas?

Do not stop your research at one defense name. Broaden your watchlist with a few focused stock ideas that match how you like to invest.

- Target long term value hunters by checking out 54 high quality undervalued stocks that combine quality fundamentals with prices that may not fully reflect their financial strength.

- Prioritise sleep at night stability with 83 resilient stocks with low risk scores that score well on resilience and may suit investors who want fewer surprises.

- Get ahead of the crowd by scanning our screener containing 24 high quality undiscovered gems and see which under followed names line up with your own research checklist.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

Have feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team@simplywallst.com