- LIVE QUOTES

- LEARN

- HELP

Nasdaq

Nasdaq Wall Street Journal

Wall Street JournalEN

A Look At Magnolia Oil & Gas (MGY) Valuation As Buybacks Expand And Operations Show Resilience

Magnolia Oil & Gas (MGY) is back in focus after expanding its share repurchase authorization to 60,000,000 shares, along with fresh 2026 production guidance, recent winter storm recovery details, and full year 2025 earnings.

See our latest analysis for Magnolia Oil & Gas.

These buyback moves and the latest production and earnings updates come after a strong run, with a 19.1% year to date share price return and a 187.3% five year total shareholder return. This suggests momentum has been building over both shorter and longer periods.

If Magnolia’s recent momentum has caught your attention, this could be a good moment to look across the energy space using our list of 85 nuclear energy infrastructure stocks as another potential source of ideas.

With Magnolia trading near its recent gains, buybacks ramping up and earnings slightly softer than last year, the key question is whether the current price still leaves room for upside or if the market is already pricing in future growth.

Most Popular Narrative: 10% Undervalued

Magnolia’s most followed narrative sees fair value at $26.81, sitting slightly above the last close of $26.78, which frames today’s buyback story in valuation terms.

Ongoing bolt-on acquisitions and successful appraisal programs are expanding Magnolia's core Giddings acreage at low cost, increasing the duration and scale of its high-return inventory. This supports longer-term production growth, more robust free cash flows, and ultimately higher revenue visibility.

Want to see what is baked into that fair value? The narrative leans heavily on measured revenue growth, slightly higher margins, and a future earnings multiple that lines up with the wider oil and gas group.

Result: Fair Value of $26.81 (UNDERVALUED)

Have a read of the narrative in full and understand what's behind the forecasts.

However, this depends on Magnolia staying on track, as its concentrated South Texas footprint and fully unhedged production both leave the story exposed to setbacks.

Find out about the key risks to this Magnolia Oil & Gas narrative.

Another View: Market Multiple Check

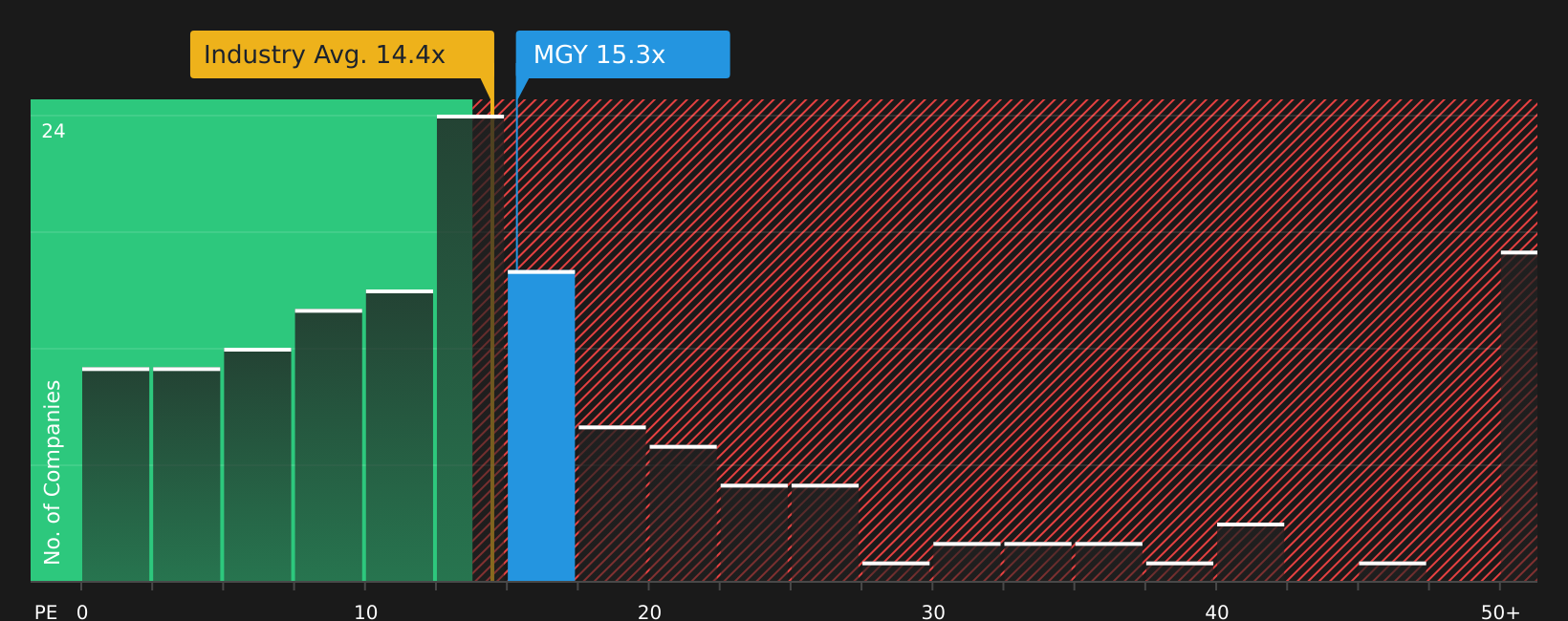

While the narrative and DCF work suggest Magnolia is undervalued, the market’s own P/E signals a different tone. The current 15.1x P/E sits above the US Oil and Gas industry at 14.5x, yet below the peer group at 18.3x and under the 18.4x fair ratio.

In practice, that means the stock is not obviously cheap or expensive on this simple yardstick. Any future move toward the fair ratio would matter a lot for your returns. Which signal do you trust more right now: the cash flow model or the market’s current multiple?

See what the numbers say about this price — find out in our valuation breakdown.

Build Your Own Magnolia Oil & Gas Narrative

If you are not fully on board with this view or prefer to lean on your own work, you can build a fresh story in just a few minutes using Do it your way.

A good starting point is our analysis highlighting 2 key rewards investors are optimistic about regarding Magnolia Oil & Gas.

Looking for more investment ideas?

If Magnolia has you thinking about what else could fit your portfolio, now is the time to line up a few more well researched candidates.

- Zero in on quality at a discount by scanning our list of 54 high quality undervalued stocks that pair fundamentals with pricing that may still be catching up.

- Lock in potential income streams by reviewing 13 dividend fortresses, where yields and payout profiles help you focus on companies built for regular cash returns.

- Sleep a little easier by checking 83 resilient stocks with low risk scores, highlighting companies with metrics that point to resilience when conditions turn choppy.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

Have feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team@simplywallst.com