- LIVE QUOTES

- LEARN

- HELP

Nasdaq

Nasdaq Wall Street Journal

Wall Street JournalEN

A Look At ReNew Energy Global (RNW) Valuation As Q3 2026 Earnings Approach

ReNew Energy Global (RNW) heads into its Q3 2026 earnings release and earnings call on February 16, 2026, with investors closely watching whether results and guidance align with current expectations.

See our latest analysis for ReNew Energy Global.

At a share price of US$5.35, ReNew Energy Global has seen short term share price pressure, with a 90 day share price return of 28.67% decline and a 1 year total shareholder return of 18.07% decline. This suggests that momentum has been fading ahead of this earnings update after earlier EPS underperformance.

If you are watching how earnings updates can shift sentiment around renewables, it could be a good moment to scan 25 power grid technology and infrastructure stocks as potential beneficiaries of long term energy infrastructure spending themes.

With RNW trading at US$5.35 against an average analyst target of about US$7.68 and a weak recent return profile, you have to ask yourself: is this punished renewables name now mispriced, or is the market already discounting future growth?

Most Popular Narrative: 32.7% Undervalued

With ReNew Energy Global closing at $5.35 against a narrative fair value of $7.95, the current price sits well below that long term story.

Ongoing technological advancements in both renewables and the company's manufacturing vertical, such as ramping up high-efficiency TOPCon products and increasing module/cell capacity, are boosting operational efficiency and margins, with manufacturing EBITDA guidance revised upward, supporting future earnings expansion.

Curious why this narrative still supports a higher value despite softer growth assumptions and cautious earnings forecasts? The key hinges on how revenue mix, margins, and the chosen discount rate interact over time.

Result: Fair Value of $7.95 (UNDERVALUED)

Have a read of the narrative in full and understand what's behind the forecasts.

However, this story can change quickly if intense renewables bidding pressure squeezes margins, or if project delays and regulatory hurdles disrupt the expected earnings path.

Find out about the key risks to this ReNew Energy Global narrative.

Another Angle on Valuation

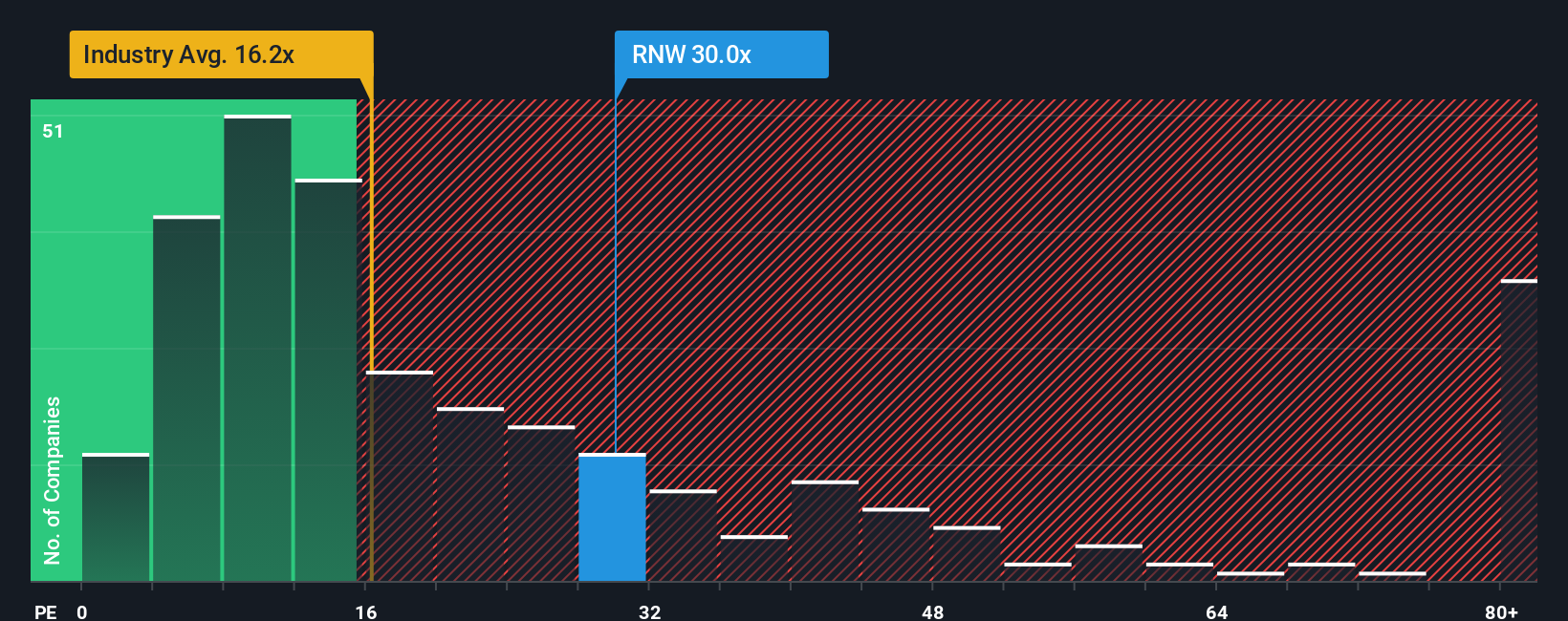

The narrative model points to RNW being 32.7% undervalued, but the earnings multiple tells a more cautious story. At a P/E of 20.9x, RNW trades cheaper than the US renewable energy group at 57.2x and peers at 50.3x, yet richer than the global sector at 16.3x and above its fair ratio of 11.4x. That mix of discount and premium raises a simple question for you: is the market offering a margin of safety here, or just pricing in extra risk?

See what the numbers say about this price — find out in our valuation breakdown.

Build Your Own ReNew Energy Global Narrative

If you are not fully on board with this storyline or prefer to weigh the numbers yourself, you can create a custom view in just a few minutes, starting with Do it your way.

A great starting point for your ReNew Energy Global research is our analysis highlighting 4 key rewards and 3 important warning signs that could impact your investment decision.

Looking for more investment ideas?

If ReNew has caught your attention, do not stop here. Broaden your watchlist with a few focused ideas that could sharpen how you think about risk and reward.

- Hunt for quality at a discount by checking companies in our 54 high quality undervalued stocks that pair fundamentals with more grounded pricing.

- Build a sturdier core in your portfolio by reviewing businesses from the solid balance sheet and fundamentals stocks screener (44 results) that prioritize financial strength.

- Spot potential standouts early by scanning the screener containing 24 high quality undiscovered gems that the market may not be paying full attention to yet.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

Have feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team@simplywallst.com