- LIVE QUOTES

- LEARN

- HELP

Nasdaq

Nasdaq Wall Street Journal

Wall Street JournalEN

Assessing Paylocity Holding (PCTY) Valuation After Recent Share Price Rebound And Ongoing Growth Concerns

Why Paylocity Holding (PCTY) is on investors’ radar today

Recent trading in Paylocity Holding (PCTY) has drawn attention after a period of pressure on the share price. This has prompted investors to reassess how the company’s current valuation lines up with its fundamentals.

See our latest analysis for Paylocity Holding.

At a share price of US$107.13, Paylocity’s recent 2.8% 1-day share price gain follows a 30-day share price return of 24% and a 1-year total shareholder return decline of 51%, which points to pressure rather than momentum building.

If this kind of pullback has you looking for other opportunities in software and automation, it could be a good moment to scan 32 robotics and automation stocks for potential fresh ideas beyond payroll and HR platforms.

With Paylocity’s share price under pressure and its current level implying a steep discount to some valuation estimates, you have to ask: is this a mispriced payroll and HR platform, or is the market already factoring in its future growth?

Most Popular Narrative: 37.1% Undervalued

With Paylocity’s fair value narrative sitting at $170.38 against a last close of $107.13, the gap between price and modeled value is hard to ignore.

Expansion of Paylocity's unified HR and finance platform, coupled with advanced AI-powered features, is enhancing automation and streamlining complex workflows for clients, positioning the company to capture growing demand from businesses undergoing digital transformation, which may drive higher recurring revenue and average revenue per client over time.

Curious what sits behind that optimism on recurring revenue and margins? The narrative leans on steady growth assumptions and a rich future earnings multiple. Want to see how those moving parts combine into a $170.38 fair value line against a $107.13 share price?

Result: Fair Value of $170.38 (UNDERVALUED)

Have a read of the narrative in full and understand what's behind the forecasts.

However, the company is guiding for slower revenue growth of 7% to 9%, and intense competition from larger HCM and payroll players could challenge those optimistic earnings and valuation assumptions.

Find out about the key risks to this Paylocity Holding narrative.

Another View: Earnings Multiple Tells a Different Story

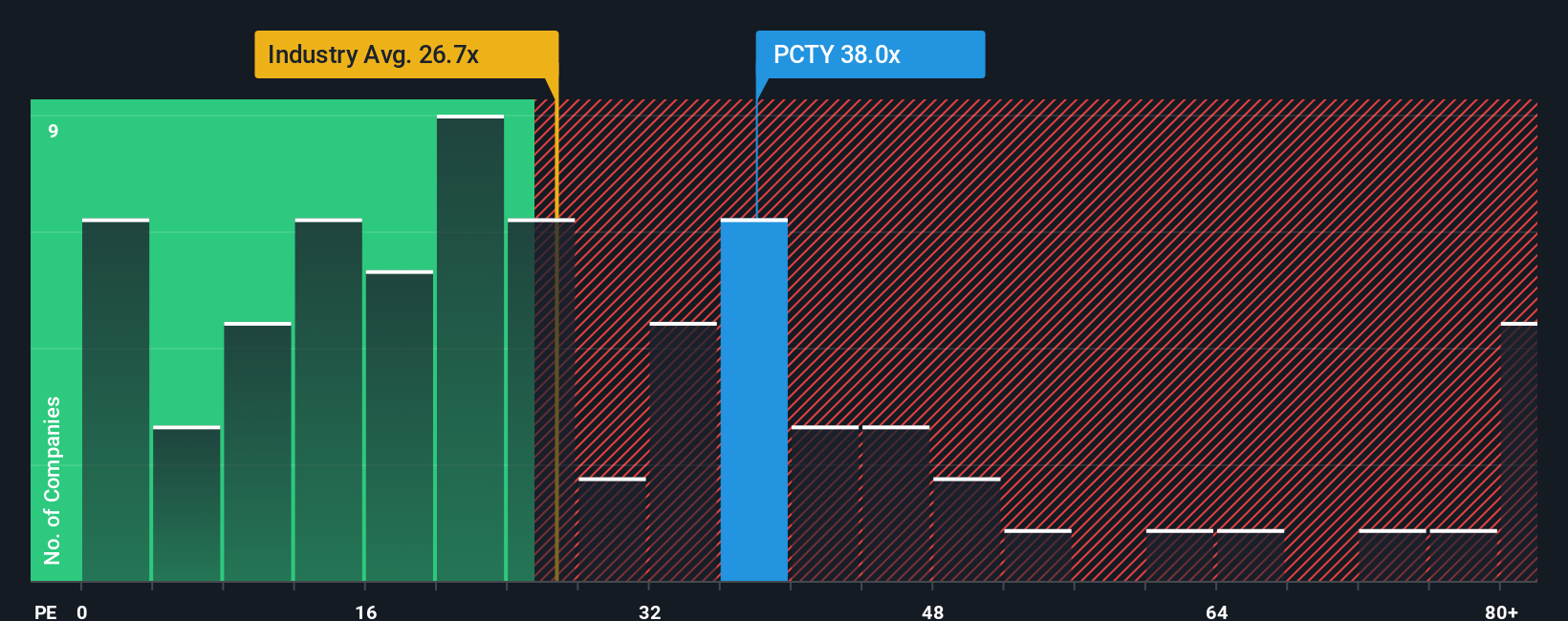

Our DCF work points to a large gap between price and modeled cash flows, yet the earnings multiple presents a more cautious picture. Paylocity trades on a P/E of 24.2x, which is higher than the US Professional Services industry at 19.4x and above peers at 16.2x, even though it sits slightly below its fair ratio of 26.1x. That combination of an apparent discount on cash flows and a premium on earnings raises a simple question for you: is the risk skewed toward multiple compression or a catch up in the share price?

See what the numbers say about this price — find out in our valuation breakdown.

Build Your Own Paylocity Holding Narrative

If you see the numbers differently or want to stress test your own assumptions, you can pull the key data together and build a custom view in just a few minutes, then Do it your way.

A good starting point is our analysis highlighting 3 key rewards investors are optimistic about regarding Paylocity Holding.

Ready to hunt for your next idea?

If Paylocity has sparked fresh thinking, do not stop here. The screener can surface other stocks that fit your style before the market fully catches on.

- Spot potential bargains that line up with quality and value by scanning our 54 high quality undervalued stocks and seeing which businesses match your checklist.

- Prioritise resilience by checking companies in the 84 resilient stocks with low risk scores that may better fit your comfort with volatility and downside.

- Get ahead of the crowd by reviewing our screener containing 24 high quality undiscovered gems, where lesser known names with strong fundamentals could be waiting for a closer look.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

Have feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team@simplywallst.com