- LIVE QUOTES

- LEARN

- HELP

Nasdaq

Nasdaq Wall Street Journal

Wall Street JournalEN

How Investors May Respond To Southern Copper (SCCO) Record Earnings, Rising Short Interest, And Tia Maria Spend

- Southern Copper recently reported record 2025 net sales, adjusted EBITDA, and net income, supported by higher copper and by‑product output, improved metal prices, and confirmed progress on major projects such as Tia Maria in Peru, alongside quarterly cash and stock dividends to shareholders.

- An interesting angle is the simultaneous rise in short interest to 10.94% of float, which contrasts with strong earnings beats and richer capital returns, highlighting a sharp divide in investor expectations.

- Next, we’ll examine how record earnings combined with accelerated Tia Maria investment alter Southern Copper’s existing investment narrative and risk balance.

We've uncovered the 12 dividend fortresses yielding 5%+ that don't just survive market storms, but thrive in them.

Southern Copper Investment Narrative Recap

To own Southern Copper, you have to believe its large, low cost copper base and long project pipeline can justify today’s valuation despite cyclical and political uncertainty. The latest record 2025 results and higher dividends reinforce the near term earnings and cash return story, while the sharp rise in short interest keeps sentiment fragile. The biggest immediate swing factor remains execution and community stability around Tia Maria; recent news does not remove that risk, but it does not materially increase it either.

The clearest link between the news and Southern Copper’s catalyst path is the confirmation of accelerated capital spending on Tia Maria, now 24% complete and targeted to start operations in 2027. That update ties record earnings and richer dividends directly to a heavier, multi year capex burden, sharpening the trade off between growth and balance sheet resilience. It also raises the stakes for any future disruption, cost inflation, or permitting friction in Peru.

Yet behind the strong 2025 numbers and bigger dividends, investors should also be aware of the mounting capital and community pressures around Tia Maria and Los Chancas...

Read the full narrative on Southern Copper (it's free!)

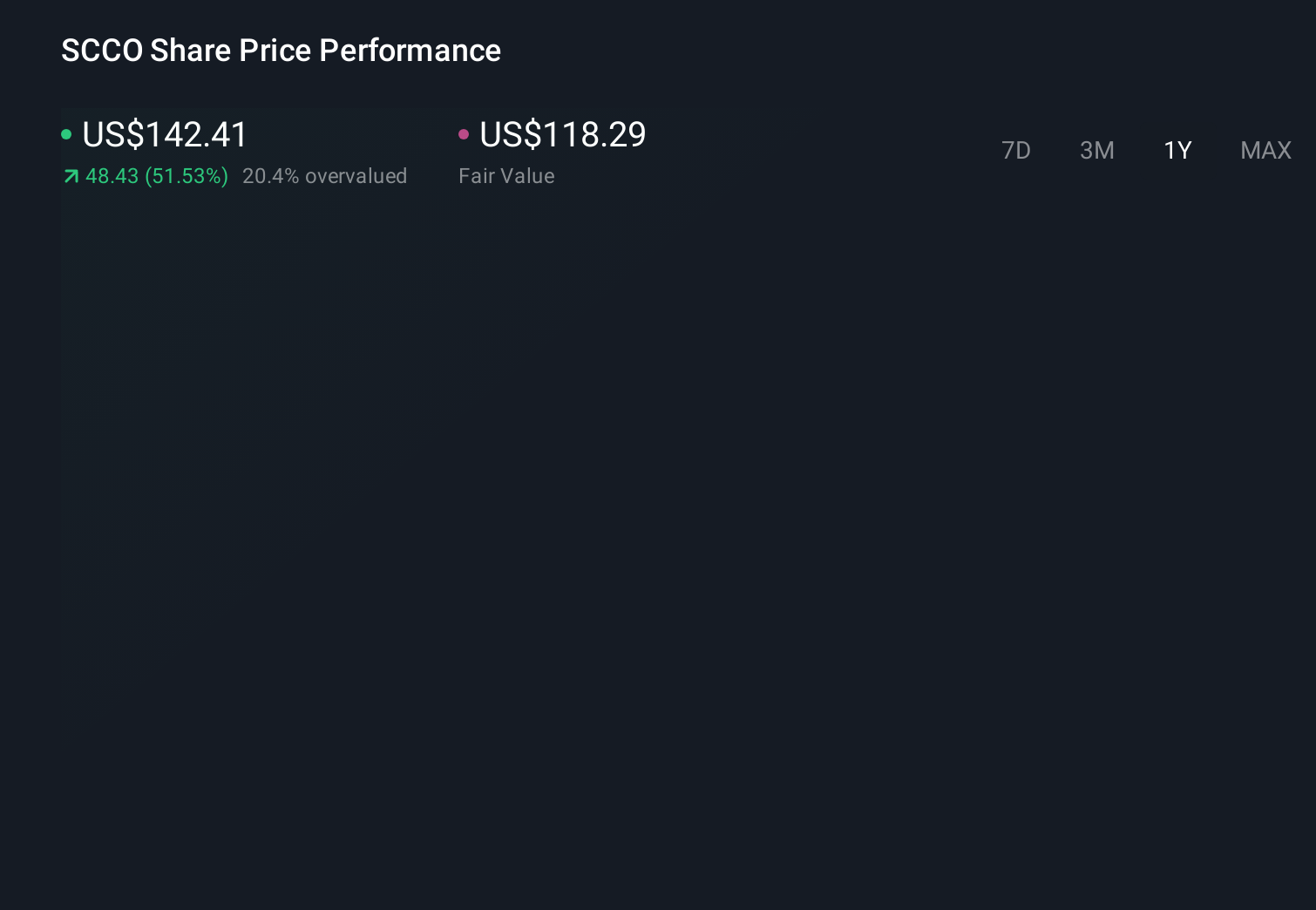

Southern Copper's narrative projects $13.0 billion revenue and $4.3 billion earnings by 2028. This requires 3.1% yearly revenue growth and a $0.7 billion earnings increase from $3.6 billion.

Uncover how Southern Copper's forecasts yield a $138.59 fair value, a 30% downside to its current price.

Exploring Other Perspectives

Some of the most optimistic analysts were already penciling in about US$13.7 billion in revenue and US$4.9 billion in earnings by 2028, but this latest earnings beat and faster Tia Maria spend could either support that bullish view or highlight how much must still go right in politically sensitive regions.

Explore 6 other fair value estimates on Southern Copper - why the stock might be worth less than half the current price!

Build Your Own Southern Copper Narrative

Disagree with existing narratives? Create your own in under 3 minutes - extraordinary investment returns rarely come from following the herd.

- A great starting point for your Southern Copper research is our analysis highlighting 2 key rewards and 2 important warning signs that could impact your investment decision.

- Our free Southern Copper research report provides a comprehensive fundamental analysis summarized in a single visual - the Snowflake - making it easy to evaluate Southern Copper's overall financial health at a glance.

Ready To Venture Into Other Investment Styles?

Opportunities like this don't last. These are today's most promising picks. Check them out now:

- Capitalize on the AI infrastructure supercycle with our selection of the 34 best 'picks and shovels' of the AI gold rush converting record-breaking demand into massive cash flow.

- Uncover the next big thing with 29 elite penny stocks that balance risk and reward.

- AI is about to change healthcare. These 25 stocks are working on everything from early diagnostics to drug discovery. The best part - they are all under $10b in market cap - there's still time to get in early.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

Have feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team@simplywallst.com