- LIVE QUOTES

- LEARN

- HELP

Nasdaq

Nasdaq Wall Street Journal

Wall Street JournalEN

Assessing EchoStar (SATS) Valuation After Recent Share Price Volatility

Why EchoStar Is On Investors’ Radar Now

EchoStar (SATS) has caught attention after a sharp share price swing, with the stock up 2.4% over the past day and 1.4% over the past week, against mixed recent returns.

See our latest analysis for EchoStar.

That recent 2.4% 1 day share price return and 1.4% 7 day share price return sit against a 30 day share price return of an 8.2% decline, as well as a 90 day share price return of 69.1% and a very large 1 year total shareholder return. Together, these figures suggest that momentum has been strong over the longer stretch even with short term pullbacks.

If this kind of sharp move has your attention, it could be a good moment to scan for other potential opportunities using our screener of 23 top founder-led companies.

With EchoStar posting a very large 1 year total return, a recent 8.2% 30 day pullback and trading roughly 10% below analyst targets, investors may wonder whether this represents a fresh entry point or whether the market is already pricing in future growth.

Most Popular Narrative: 6.3% Undervalued

EchoStar’s most followed valuation narrative puts fair value at about $120.71 per share, compared with the latest close of $113.15, which catches the eye given the recent volatility.

As global cloud-based application and data consumption accelerates, EchoStar's technology leadership in satellite-enabled, enterprise-grade connectivity, including in-flight and mobility solutions, positions it to capture a larger share of enterprise and government contracts, which are typically high-value and high-margin, supporting long-term revenue and earnings growth.

Curious what sits behind that valuation gap? The narrative leans heavily on future profitability, a different earnings mix, and a higher earnings multiple than today. The exact combination matters.

Result: Fair Value of $120.71 (UNDERVALUED)

Have a read of the narrative in full and understand what's behind the forecasts.

However, you also need to weigh FCC spectrum uncertainty in addition to EchoStar’s sizable debt and funding needs, which could pressure cash flow and reshape the current earnings story.

Find out about the key risks to this EchoStar narrative.

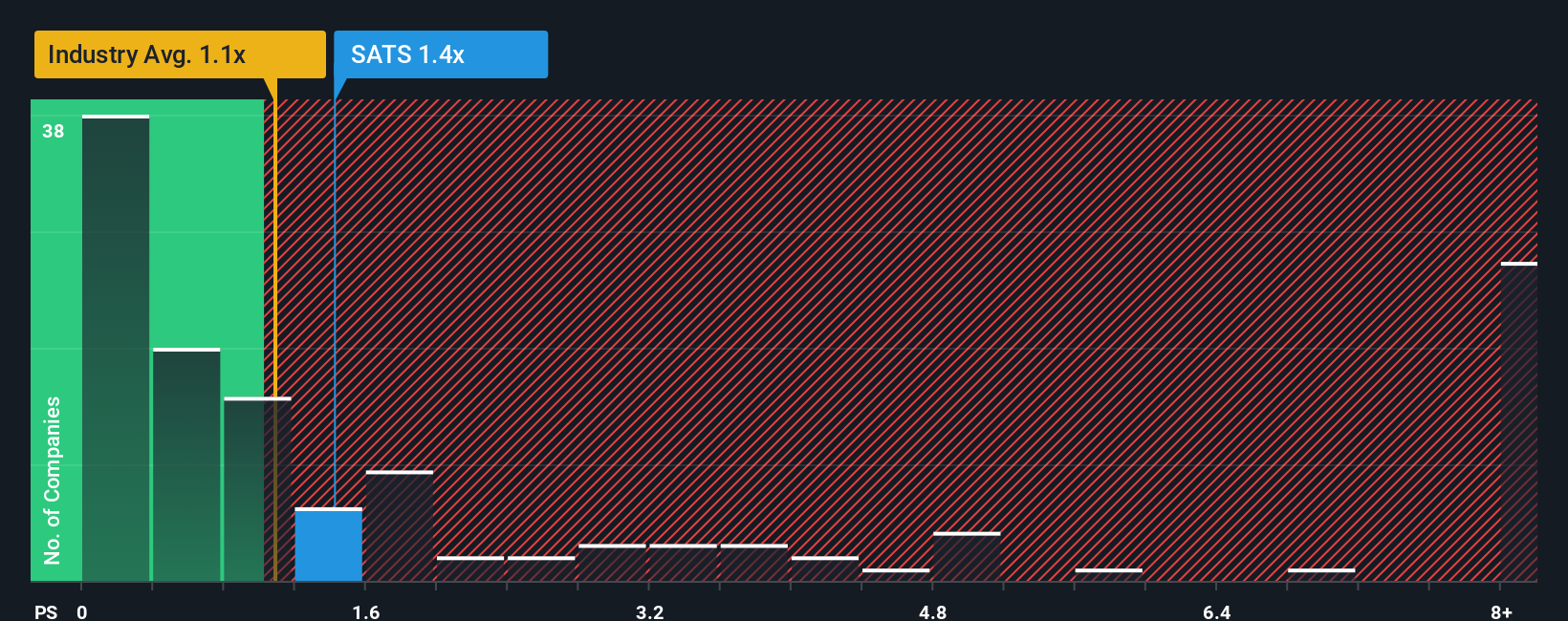

Another View: Market Multiple Sends A Different Signal

That $120.71 fair value hinges on future earnings improving, but the current P/S of 2.1x tells a tougher story. It sits well above the US Media industry at 0.9x and the fair ratio of 1.5x, which implies less room for error if growth or margins fall short. Which signal do you trust more right now?

See what the numbers say about this price — find out in our valuation breakdown.

Build Your Own EchoStar Narrative

If you are not fully on board with these views or prefer to test the numbers yourself, you can build a custom thesis in minutes by starting with Do it your way.

A great starting point for your EchoStar research is our analysis highlighting 2 important warning signs that could impact your investment decision.

Ready For More Investment Ideas?

If EchoStar has sparked your interest, do not stop here. Use the Simply Wall St screener to surface fresh ideas that match your style and keep your watchlist sharp.

- Target potential value opportunities by reviewing our list of 53 high quality undervalued stocks that combine quality fundamentals with attractive pricing.

- Prioritise resilience by scanning 84 resilient stocks with low risk scores that score well on balance sheet strength and overall risk metrics.

- Get ahead of the crowd by checking our screener containing 23 high quality undiscovered gems before they draw wider attention from the market.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

Have feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team@simplywallst.com