- LIVE QUOTES

- LEARN

- HELP

Nasdaq

Nasdaq Wall Street Journal

Wall Street JournalEN

A Look At Lamb Weston (LW) Valuation After Recent Executive Chair And CFO Appointments

Leadership changes reshape the story around Lamb Weston

Lamb Weston Holdings (LW) has drawn fresh attention after its board appointed Jan Eli B. Craps as Executive Chair and named James D. Gray as incoming Chief Financial Officer, signaling a possible shift in how the company is led and how its capital is managed.

See our latest analysis for Lamb Weston Holdings.

Those leadership and capital moves come as Lamb Weston’s share price sits at US$49.82, with a 1 month share price return of 14.98% and year to date share price return of 17.81%. The 1 year total shareholder return of 12.37% and 3 year total shareholder return of 47.30% point to weaker longer term results that investors may be weighing against any change in growth expectations or risk profile.

If this leadership reset has you thinking about where else change could matter, it might be a good moment to scan 23 top founder-led companies and see which founder led names are starting to stand out.

With Lamb Weston trading at US$49.82, sitting close to analysts’ average price target and flagged by some models as trading at a discount to estimated intrinsic value, you have to ask: is there still upside here, or is the market already baking in future growth?

Most Popular Narrative: 8.8% Undervalued

The most followed narrative puts Lamb Weston’s fair value at about $54.64 per share, modestly above the last close at $49.82. It anchors that view in a detailed earnings path and profit margin profile.

The analysts have a consensus price target of $63.727 for Lamb Weston Holdings based on their expectations of its future earnings growth, profit margins and other risk factors. However, there is a degree of disagreement amongst analysts, with the most bullish reporting a price target of $80.0, and the most bearish reporting a price target of just $57.0.

Want to see what underpins that fair value gap? The narrative leans on moderate revenue growth, firmer margins and a lower future earnings multiple than many food peers. The mix may surprise you.

Result: Fair Value of $54.64 (UNDERVALUED)

Have a read of the narrative in full and understand what's behind the forecasts.

However, this depends on restaurant traffic stabilising and price pressure easing. Both trends could remain challenging for longer, particularly in lower margin emerging markets.

Find out about the key risks to this Lamb Weston Holdings narrative.

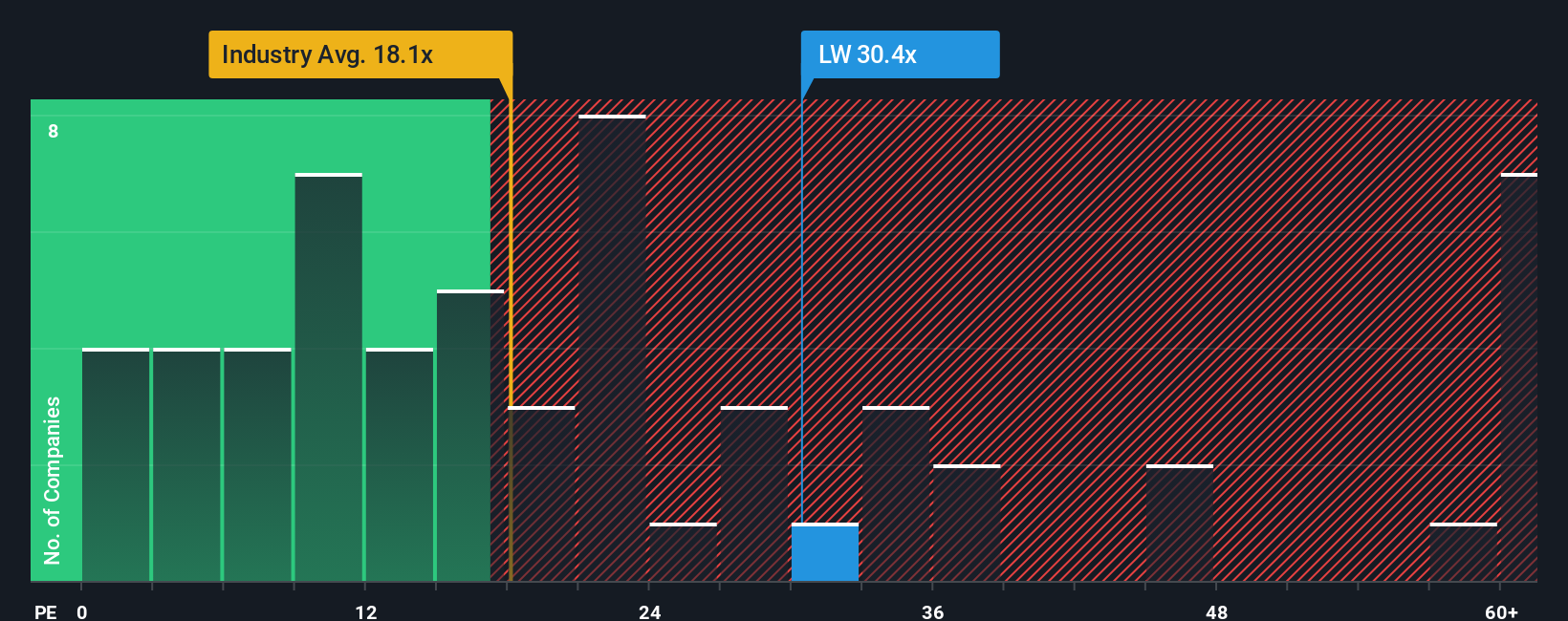

Another angle: what earnings multiples are saying

The story looks different when you just look at the P/E. Lamb Weston trades on 17.6x earnings, above peers at 13x, yet below the wider US Food group at 24.4x and under its own fair ratio of 23.1x. That mix points to both premium risk and potential opportunity. Which side matters more to you?

See what the numbers say about this price — find out in our valuation breakdown.

Build Your Own Lamb Weston Holdings Narrative

If you read this and think the story looks different when you check the numbers yourself, you can pull up the data, test your own assumptions, and shape a fresh Lamb Weston view in just a few minutes. Then Do it your way.

A great starting point for your Lamb Weston Holdings research is our analysis highlighting 3 key rewards and 1 important warning sign that could impact your investment decision.

Looking for more investment ideas?

If Lamb Weston has sharpened your thinking, do not stop here. The screener can surface ideas that fit your style and keep your watchlist evolving.

- Target dependable income streams by checking out 12 dividend fortresses that might suit an income focused approach.

- Hunt for quality at a price that could appeal to you through our 53 high quality undervalued stocks grounded in fundamentals.

- Focus on financial strength first and scan the solid balance sheet and fundamentals stocks screener (45 results) so you do not overlook sturdier balance sheets.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

Have feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team@simplywallst.com