- PRICING

- LIVE QUOTES

- LEARN

- HELP

EN

A Look At Under Armour (UAA) Valuation After Citi Downgrade And Mixed Earnings

Why Under Armour stock just drew fresh scrutiny

Citi's downgrade of Under Armour (UAA) to Sell after its mixed earnings and guidance has put fresh focus on the stock, highlighting rising North American pressures, high short interest, and expectations for negative free cash flow.

See our latest analysis for Under Armour.

Under Armour's share price has been volatile around these updates, with a 90 day share price return of 68.78% and year to date share price return of 35.92%, even as the 5 year total shareholder return is a 68.48% decline. This suggests shorter term momentum against a weaker long term record.

If Citi's downgrade has you reassessing your watchlist, it could be a good moment to broaden your search with our 23 top founder-led companies as potential long term compounders.

With the stock trading close to the average analyst price target, carrying a value score of 5, heavy short interest, and insider buying in the background, you have to ask: is there real upside left, or is the market already pricing in any future growth?

Most Popular Narrative: 10.5% Overvalued

Under Armour's most followed narrative pegs fair value at $6.51, which sits below the latest close at $7.19, so you are looking at a valuation gap that needs explaining.

Analysts are assuming Under Armour's revenue will grow by 1.5% annually over the next 3 years.

Analysts assume that profit margins will increase from 2.0% today to 3.6% in 3 years time.

Revenue only inches higher, yet earnings are expected to lift meaningfully, powered by margin recovery and a richer mix. This raises the question of how those moving parts translate into today’s fair value and the future earnings multiple the narrative uses.

Result: Fair Value of $6.51 (OVERVALUED)

Have a read of the narrative in full and understand what's behind the forecasts.

However, you also need to weigh ongoing margin pressure from tariffs and weak demand, along with underperforming footwear, which could cap earnings power and challenge the current narrative.

Find out about the key risks to this Under Armour narrative.

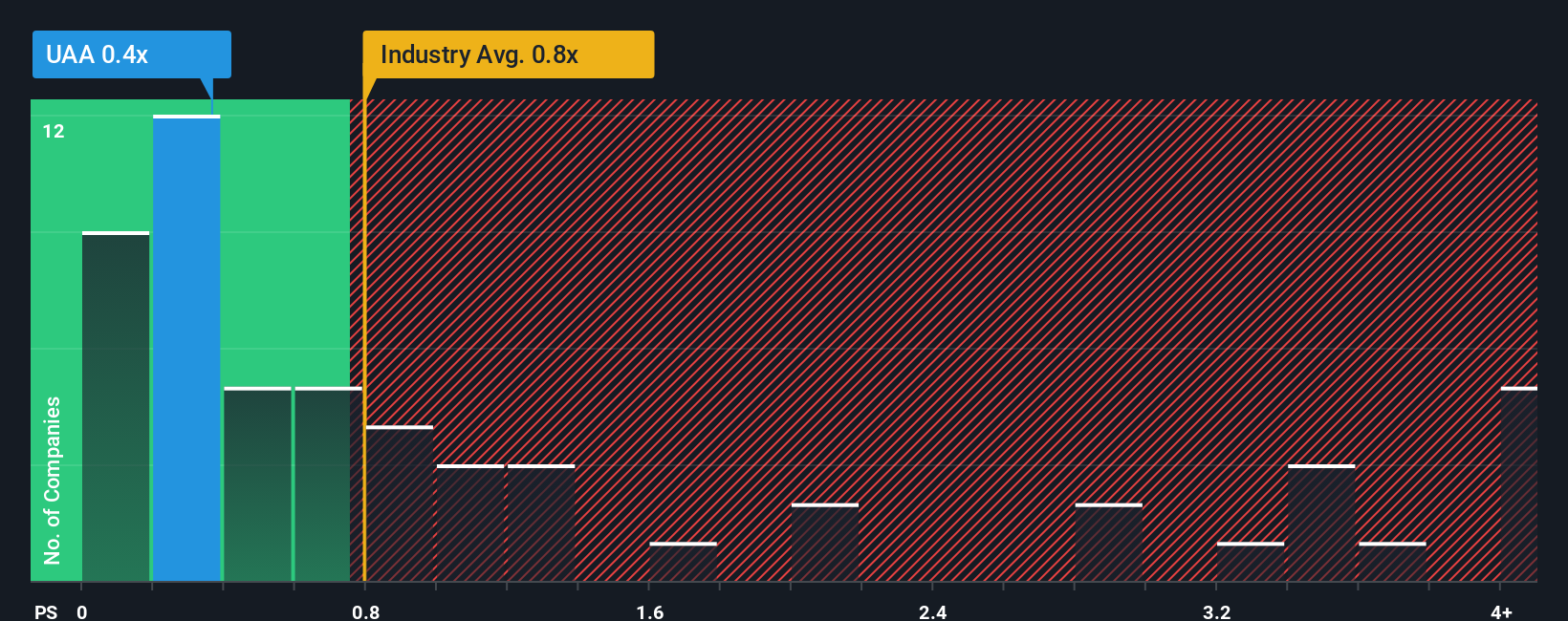

Another View: Multiples Point To Value Support

While the narrative model suggests Under Armour is 10.5% overvalued at $7.19 versus a fair value of $6.51, the current P/S of 0.6x tells a different story. It sits below both the US Luxury industry and peer averages at 0.8x, and below a fair ratio of 1x, which lowers valuation risk if sentiment weakens again. So which signal do you trust more: the narrative gap or the sales multiple discount?

See what the numbers say about this price — find out in our valuation breakdown.

Build Your Own Under Armour Narrative

If you look at the numbers and come to a different conclusion, or simply want to test your own assumptions, you can build a custom view in a few minutes, starting with Do it your way.

A good starting point is our analysis highlighting 3 key rewards investors are optimistic about regarding Under Armour.

Looking for more investment ideas?

If you stop with just one stock, you risk missing opportunities that match your style far better, so give yourself options with a few targeted screens.

- Target potential value opportunities by checking out our 53 high quality undervalued stocks, which filters for companies with solid fundamentals trading below our estimates of fair worth.

- Focus on resilience first by scanning our 84 resilient stocks with low risk scores, which highlights businesses with lower risk scores for investors who want fewer surprises.

- Spot earlier stage opportunities by using our 29 elite penny stocks with strong financials, which surfaces lower priced companies with stronger financial profiles than many peers.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

Have feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team@simplywallst.com