- LIVE QUOTES

- LEARN

- HELP

Nasdaq

Nasdaq Wall Street Journal

Wall Street JournalEN

Assessing CVS Health (CVS) Valuation As Earnings Rebuild And Restructuring Shape Expectations

What CVS Health’s latest numbers say about the business

CVS Health (CVS) has been in focus as investors weigh its recent share performance alongside fresh financial figures, including annual revenue of about US$399.8b and net income of roughly US$1.8b.

Over the past year, the stock’s total return sits near 24%, while year to date it reflects a loss of about 2%. Returns over the past 3 months are close to flat, with the one-month performance also little changed.

In that context, CVS Health currently carries a value score of 3. This can help you benchmark it against other health care names that also blend insurance, pharmacy benefit management and retail pharmacy operations.

See our latest analysis for CVS Health.

With the share price at US$78.48, CVS Health’s recent 1-day and 1-year share price returns differ sharply from its 1-year total shareholder return of about 24%, which highlights how dividends have contributed meaningfully while shorter term share price momentum has been softer.

If this update has you reassessing your health care exposure, it could be a good moment to see what else is out there through our screener of 25 healthcare AI stocks.

With CVS Health trading around US$78.48 and sitting on a value score of 3, you might be wondering if this is a solid entry point or if markets are already factoring in the company’s next leg of growth.

Most Popular Narrative: 24.5% Undervalued

Compared with the last close at $78.48, the most followed narrative pegs CVS Health’s fair value closer to $104, which frames the current share price as a discount.

CVS Health’s recent stock drop reveals a deeply undervalued healthcare giant with strong upside potential if its $2 billion restructuring plan succeeds in boosting profitability and stabilizing growth.

Curious what sits behind that valuation gap? The narrative leans heavily on a multiyear earnings rebuild, revenue expansion in health benefits, and a profitability reset that is anything but straightforward.

Result: Fair Value of $104.01 (UNDERVALUED)

Have a read of the narrative in full and understand what's behind the forecasts.

However, this hinges on CVS containing medical cost pressures in its Health Care Benefits segment and successfully executing its US$2b restructuring without further profit hits.

Find out about the key risks to this CVS Health narrative.

Another angle on valuation

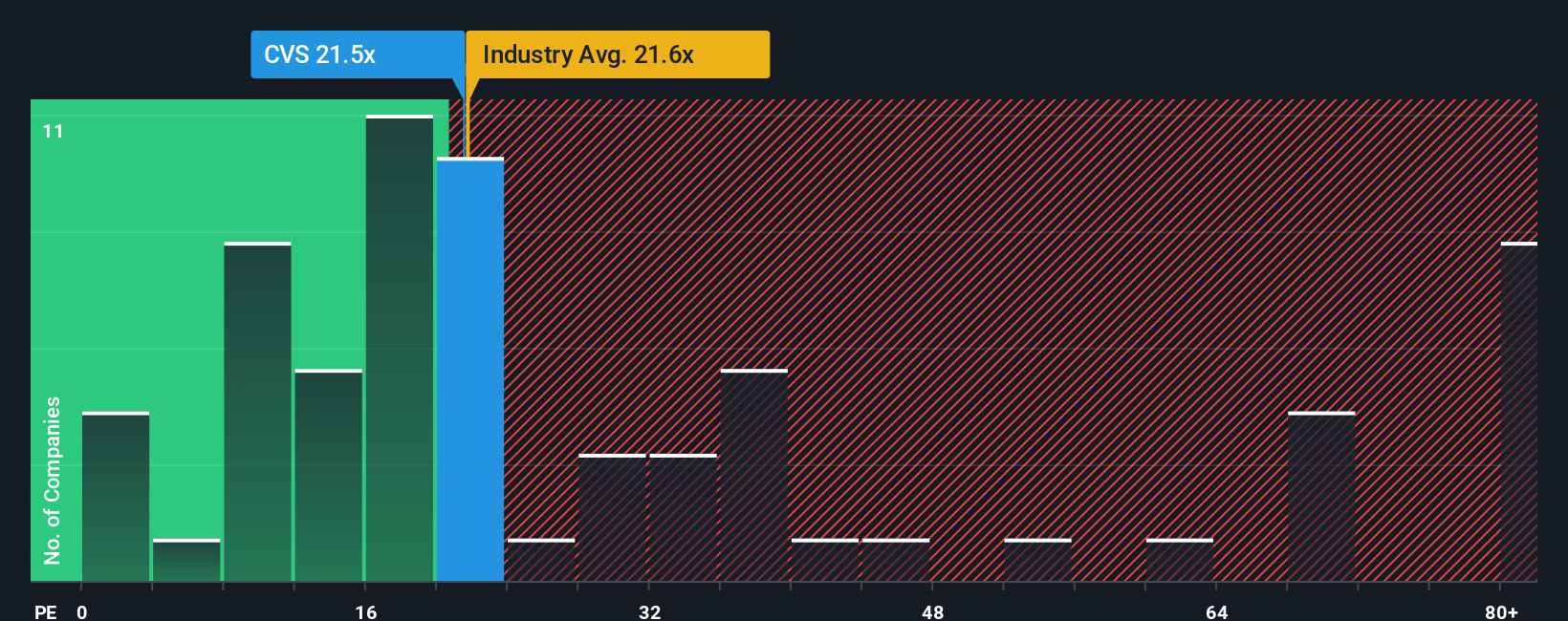

The user narrative leans heavily on earnings and a low P/E to frame CVS Health as undervalued, but our multiples work tells a different story. On the latest numbers, CVS trades at a P/E of 56.5x, compared with 23.6x for the US Healthcare industry and 19.3x for peers, and a fair ratio of 42.9x. That gap points to a richer pricing that could limit upside if earnings do not rebuild quickly. The key question is how much confidence investors place in the earnings recovery story.

See what the numbers say about this price — find out in our valuation breakdown.

Build Your Own CVS Health Narrative

If you see the numbers differently or prefer to base your view on your own work, you can build a tailored CVS Health story in just a few minutes, starting with Do it your way.

A great starting point for your CVS Health research is our analysis highlighting 3 key rewards and 4 important warning signs that could impact your investment decision.

Ready to find your next investment idea?

Once you have a view on CVS Health, do not stop there. Your next opportunity could be sitting in plain sight among other stocks that fit your criteria.

- Target potential bargains by scanning companies that combine quality fundamentals with room for a better price using our 53 high quality undervalued stocks.

- Strengthen your income stream by focusing on companies with yields above 5% using our curated list of 12 dividend fortresses.

- Sleep easier at night by filtering for companies with steadier profiles and fewer red flags through our 84 resilient stocks with low risk scores.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

Have feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team@simplywallst.com