- LIVE QUOTES

- LEARN

- HELP

Nasdaq

Nasdaq Wall Street Journal

Wall Street JournalEN

A Look At Mach Natural Resources (MNR) Valuation After Its New Q4 2025 Cash Distribution Announcement

Mach Natural Resources (MNR) has put income front and center, with its board declaring a fourth quarter 2025 cash distribution of $0.53 per common unit to unitholders of record on February 26, 2026.

See our latest analysis for Mach Natural Resources.

The latest distribution news lands after a stretch of firm share price momentum, with a 30 day share price return of 19.2% and a 90 day share price return of 10.74%. This comes even though the 1 year total shareholder return is a 6.69% decline, which may hint at changing sentiment ahead of the upcoming full year 2025 results announcement on March 12, 2026.

If this income update has you thinking about where else cash generating energy names might sit, it could be a good time to scan 85 nuclear energy infrastructure stocks as a starting list of infrastructure focused ideas.

With units at $13.10, an indicated intrinsic discount of roughly 55% and a value score of 4, the key question is simple: Is Mach Natural Resources still underappreciated, or are markets already pricing in future growth?

Most Popular Narrative: 32.5% Undervalued

With Mach Natural Resources at $13.10 against a widely followed fair value estimate of $19.40, the current price sits well below that narrative anchor, which is built on detailed assumptions about future earnings, revenue and margins.

Strategic acquisitions of cash-flowing, low-decline assets in core U.S. basins at discounts to PDP PV-10, combined with disciplined reinvestment rates below 50% and rapid integration of operational synergies, are set to enhance free cash flow and expand operating margins, allowing for consistent, attractive returns to unitholders and future EPS growth.

Want to see what sits behind that confidence in future cash flows? The narrative leans heavily on specific revenue growth, margin expectations and a higher future earnings multiple. Curious how those moving parts stack up against the current unit price and analyst targets without you having to build a full model yourself?

Result: Fair Value of $19.40 (UNDERVALUED)

Have a read of the narrative in full and understand what's behind the forecasts.

However, heavier reliance on natural gas and an acquisition-driven model leaves the story exposed if commodity prices, capital access, or deal economics turn less favorable.

Find out about the key risks to this Mach Natural Resources narrative.

Another View: Earnings Multiple Paints a Tighter Picture

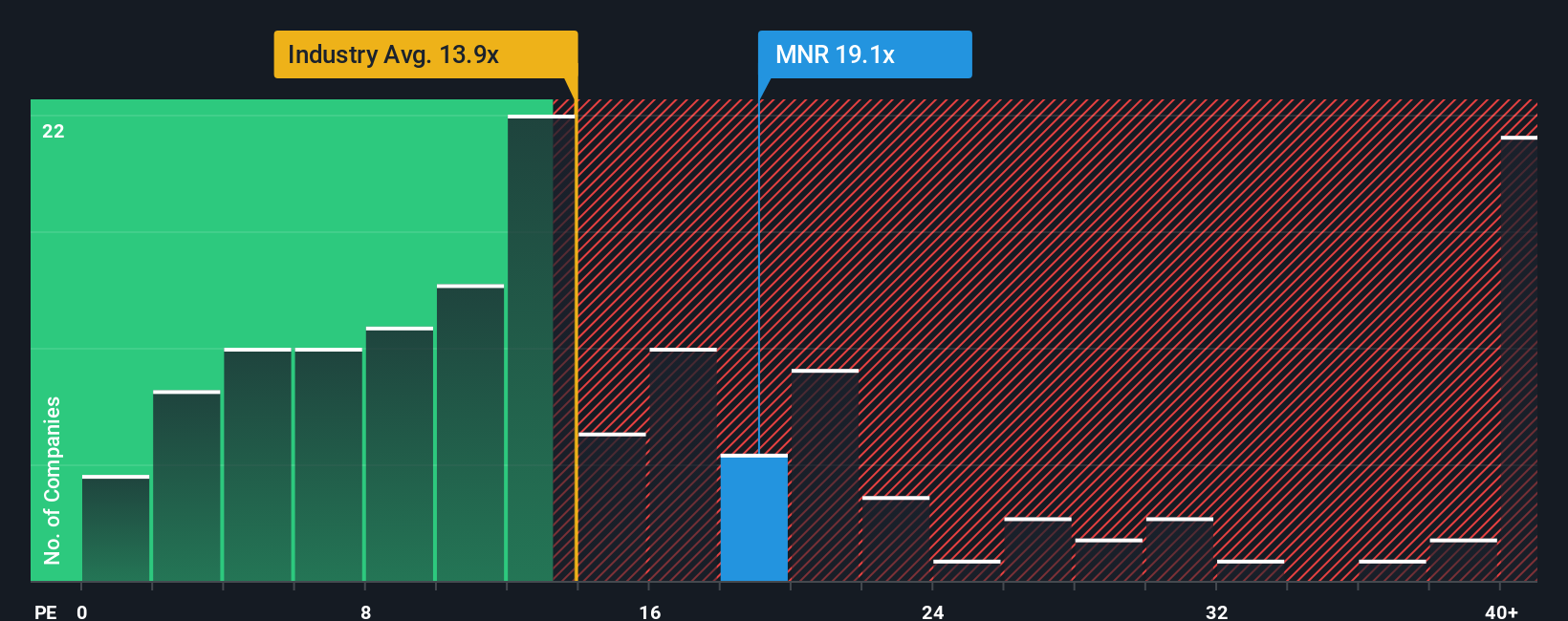

Here is where the story becomes more nuanced. On a P/E of 20.7x, Mach Natural Resources trades above the US Oil and Gas industry at 14.5x and above its own fair ratio of 18.6x, yet below a peer average of 47.3x. This raises a simple question: how much margin of safety is really left here?

See what the numbers say about this price — find out in our valuation breakdown.

Build Your Own Mach Natural Resources Narrative

If parts of this story do not match your own view, or you simply prefer to work from your own assumptions, you can test different scenarios, stress the numbers that matter most to you, and shape a view that fits your investment style with Do it your way.

A great starting point for your Mach Natural Resources research is our analysis highlighting 4 key rewards and 4 important warning signs that could impact your investment decision.

Looking for more investment ideas?

If you are weighing up Mach Natural Resources, it can pay to broaden your watchlist and compare it with other income and total return candidates.

- Spot potential value by scanning our list of 53 high quality undervalued stocks, which pair solid fundamentals with prices that may not fully reflect their strengths yet.

- Prioritise resilience by reviewing 84 resilient stocks with low risk scores, which score well on stability metrics, so short term swings are less likely to derail your long term plan.

- Hunt for off the radar opportunities through our screener containing 23 high quality undiscovered gems, which many investors may not be watching closely yet.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

Have feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team@simplywallst.com