- LIVE QUOTES

- LEARN

- HELP

Nasdaq

Nasdaq Wall Street Journal

Wall Street JournalEN

A Look At Digi International (DGII) Valuation After Earnings Beat And Positive 2026 Growth Guidance

Digi International (DGII) is back in focus after reporting first quarter results that showed higher revenue and net income year over year, along with fresh guidance outlining expected revenue and annual recurring revenue growth for 2026.

See our latest analysis for Digi International.

The earnings beat and updated guidance appear to be feeding into strong momentum, with a 27.77% 90 day share price return and a 39.88% one year total shareholder return pointing to growing optimism around Digi International’s long term story.

If Digi’s recent move has you thinking about other connected tech opportunities, you might want to scan our list of 34 AI infrastructure stocks as a starting point for further ideas.

With Digi now trading near its analyst target and showing annual revenue and net income growth, the key question is whether that 41% intrinsic discount hints at mispricing or if the market is already baking in the 2026 outlook.

Most Popular Narrative: 2% Overvalued

Compared with Digi International’s last close at $48.26, the widely followed fair value narrative of $47.33 points to a small premium that hinges on future execution.

The accelerating transition of customers to Digi's subscription-based and recurring revenue solutions, combined with increased demand for secure edge solutions, is boosting revenue stability, margins, and customer retention. Increased adoption of cloud and hybrid infrastructure, especially as enterprises and data centers pursue AI and edge deployments, is creating heightened demand for Digi's edge connectivity and remote management solutions, supporting higher sales volumes and more premium-priced contracts, which positively impact topline revenue and net margins.

Curious what kind of revenue path, margin lift and future earnings multiple are baked into that fair value? The full narrative lays out the numbers in detail.

Result: Fair Value of $47.33 (OVERVALUED)

Have a read of the narrative in full and understand what's behind the forecasts.

However, there are still pressure points, including flat 2025 revenue guidance and regional demand softness in APAC and Europe, that could challenge this upbeat fair value story.

Find out about the key risks to this Digi International narrative.

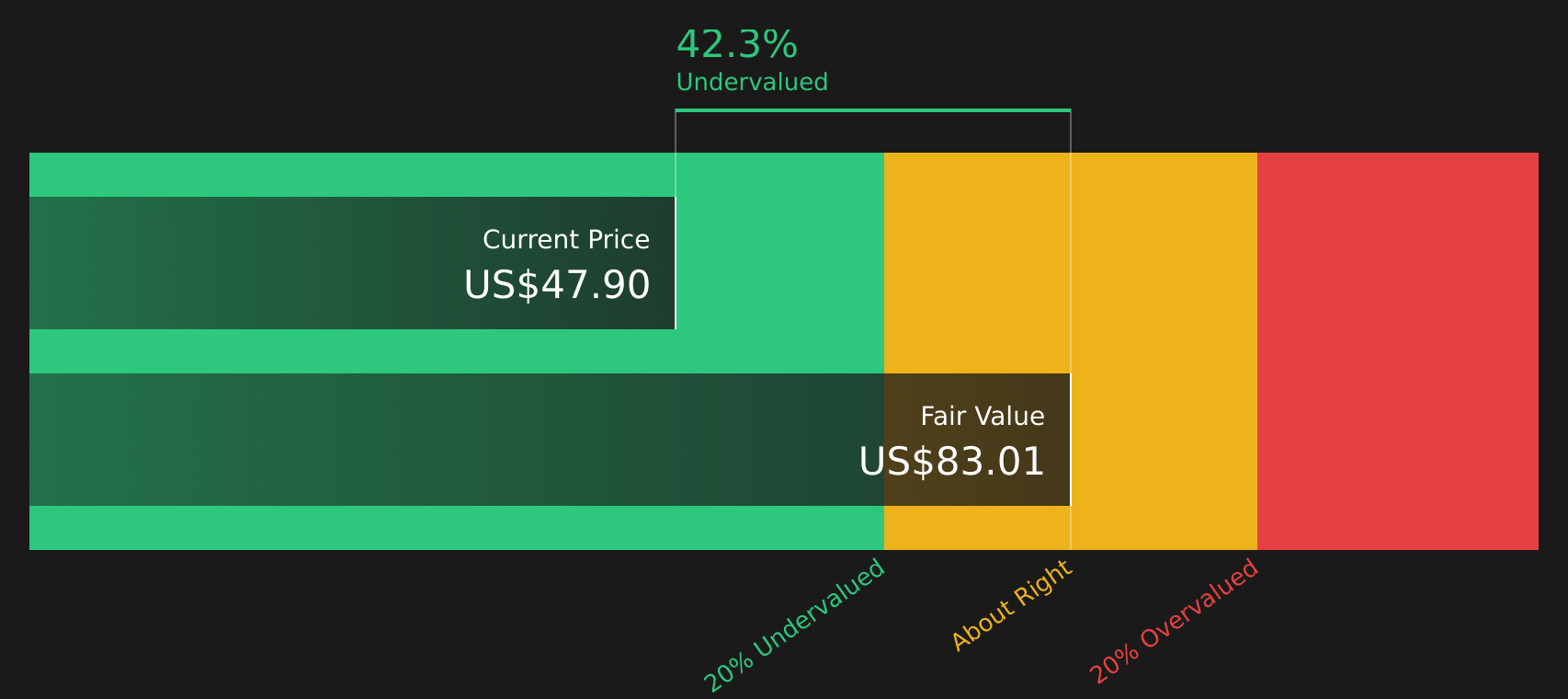

Another View: Cash Flows Tell A Different Story

While some observers reference a share price of around $47.33 for Digi International and describe the stock as slightly overvalued, our DCF model provides a different perspective. It calculates an estimated future cash flow value of $82.75 per share, which indicates that the current trading price may represent a significant discount. Which version of fair value do you think better reflects the risks and growth assumptions being considered?

Look into how the SWS DCF model arrives at its fair value.

Simply Wall St performs a discounted cash flow (DCF) on every stock in the world every day (check out Digi International for example). We show the entire calculation in full. You can track the result in your watchlist or portfolio and be alerted when this changes, or use our stock screener to discover 53 high quality undervalued stocks. If you save a screener we even alert you when new companies match - so you never miss a potential opportunity.

Build Your Own Digi International Narrative

If you see Digi’s story differently or prefer to weigh the assumptions yourself, you can develop your own view in a few minutes and Do it your way.

A great starting point for your Digi International research is our analysis highlighting 3 key rewards and 1 important warning sign that could impact your investment decision.

Looking for more investment ideas?

If Digi has sharpened your focus, do not stop here. The right watchlist mix starts with scanning a few high quality stock shortlists before the crowd catches on.

- Target stronger value opportunities by checking our list of 53 high quality undervalued stocks that combine quality fundamentals with pricing that may appeal to disciplined buyers.

- Prioritise resilience first and see whether any of the 84 resilient stocks with low risk scores fit the kind of steadier profile you want at the core of your portfolio.

- Add potential upside to your research pipeline by reviewing the screener containing 23 high quality undiscovered gems before they sit squarely on everyone else's radar.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

Have feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team@simplywallst.com