- LIVE QUOTES

- LEARN

- HELP

Nasdaq

Nasdaq Wall Street Journal

Wall Street JournalEN

Assessing Aura Minerals (NasdaqGS:AUGO) Valuation After Sagil Capital Stake And Strong Growth Narrative

Sagil Capital LLP’s new position in Aura Minerals (NasdaqGS:AUGO), roughly 156,000 shares worth about US$7.86 million, has put fresh attention on the miner following a very large share price move after its listing.

See our latest analysis for Aura Minerals.

The recent Sagil purchase comes on top of sharp share price momentum, with a 1 month share price return of 20.16% and a 90 day move of 108.89%. The 1 year total shareholder return of over 4x and the very large 3 and 5 year total shareholder returns signal strong longer term performance.

If Aura’s run has you looking across the precious metals space, it could be a good moment to see what else is moving among 21 elite gold producer stocks.

With Aura trading around US$72.36 and sitting above the current analyst price target, yet flagged with a sizeable intrinsic discount, it raises a key question for you: is there still a mispricing here, or is the market already banking on future growth?

Most Popular Narrative: 61.2% Overvalued

Compared to the narrative fair value of roughly $44.88, Aura’s last close at $72.36 sits well above that estimate, which is where the most followed storyline on the stock begins to take shape.

The planned development of Era Dorada and either Matupa or Guatemala, with relatively contained initial capital requirements, positions the portfolio for multi-year volume growth. This may improve earnings durability and return on invested capital.

Curious what kind of revenue climb and margin reset would need to play out to support that fair value gap? The narrative leans on aggressive growth, sharply higher profitability and a future earnings multiple that looks more like a mature compounder than a distressed miner. If you want to see exactly which assumptions have to land for this pricing view to hold, the full story lays it all out.

Result: Fair Value of $44.88 (OVERVALUED)

Have a read of the narrative in full and understand what's behind the forecasts.

However, there are also risks to this overvaluation call, including higher production from new projects and any successful cost resets that lift margins and cash generation.

Find out about the key risks to this Aura Minerals narrative.

Another View: Cash Flows Tell a Different Story

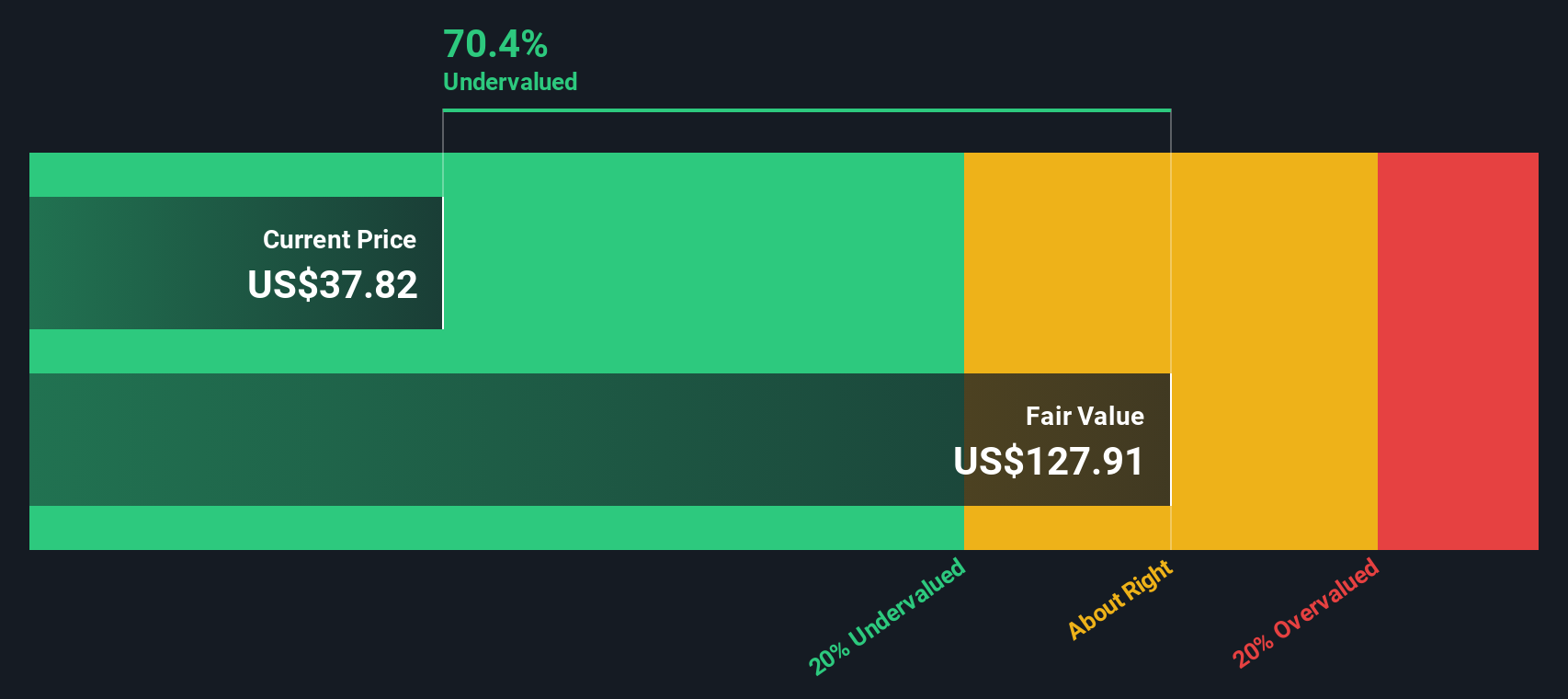

While the consensus narrative flags Aura as overvalued versus a $44.88 fair value, our DCF model points the other way, with an estimated future cash flow value of $154.71 per share compared with today’s $72.36. If the cash flow math holds up, is the crowd leaning too hard on near term earnings?

Look into how the SWS DCF model arrives at its fair value.

Simply Wall St performs a discounted cash flow (DCF) on every stock in the world every day (check out Aura Minerals for example). We show the entire calculation in full. You can track the result in your watchlist or portfolio and be alerted when this changes, or use our stock screener to discover 53 high quality undervalued stocks. If you save a screener we even alert you when new companies match - so you never miss a potential opportunity.

Build Your Own Aura Minerals Narrative

If you see the numbers differently or want to stress test your own assumptions, you can build a custom Aura thesis in just a few minutes: Do it your way.

A great starting point for your Aura Minerals research is our analysis highlighting 2 key rewards and 1 important warning sign that could impact your investment decision.

Looking for more investment ideas?

If Aura has sharpened your thinking, do not stop here. Cast a wider net with a few focused stock ideas that could sharpen your watchlist.

- Zero in on potential mispricings by scanning our 53 high quality undervalued stocks, which combines financial quality checks with attractive pricing signals.

- Strengthen your income stream by reviewing 12 dividend fortresses, which targets higher yielding companies with an emphasis on consistency.

- Sleep a little easier by checking 84 resilient stocks with low risk scores, which filters for companies with more resilient risk profiles and steadier fundamentals.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

Have feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team@simplywallst.com