- LIVE QUOTES

- LEARN

- HELP

Nasdaq

Nasdaq Wall Street Journal

Wall Street JournalEN

Assessing Fortinet (FTNT) Valuation After Earnings Beat Guidance Lift And FortiSIEM Upgrade

Why Fortinet’s latest earnings, guidance, and product moves matter now

Fortinet (FTNT) is back in focus after full year 2025 results topped expectations on key metrics, management issued firm 2026 revenue guidance, and the company rolled out a major FortiSIEM upgrade.

Together with recent analyst commentary highlighting billings guidance and Secure Access Service Edge traction, these updates give investors fresh data points on growth, profitability, and how product development may support Fortinet’s long term cybersecurity ambitions.

See our latest analysis for Fortinet.

The recent run of news around full year earnings, higher 2026 revenue guidance, the expanded buyback and the FortiSIEM upgrade has lined up with stronger momentum. The 30 day share price return is 13.5% and the 3 year total shareholder return is 41.09%, despite a 1 year total shareholder return decline of 23.36%.

If Fortinet’s cybersecurity story has you thinking more broadly about where growth could come from next, it might be worth scanning 34 AI infrastructure stocks as a starting list of AI infrastructure names to review.

With the stock up 13.5% over 30 days yet still showing a 23.36% 1 year total return decline and trading below the average analyst target, is Fortinet quietly undervalued here or already pricing in its next leg of growth?

Most Popular Narrative: 1.7% Undervalued

Fortinet’s most followed narrative pegs fair value at $87.04, slightly above the latest close at $85.56, so the story hinges on relatively fine valuation gaps.

Fortinet's successful pivot toward high margin, recurring software, subscription, and services revenue evidenced by rapid ARR growth in Unified SASE (22%), SecOps (35%), and attached/adjacent cloud based services is structurally expanding gross and operating margins, decreasing business cyclicality, and boosting long term earnings quality.

Curious how modest upside and a tight discount rate still support that fair value? The narrative leans on projected growth, margin resilience, and a premium future earnings multiple. The exact mix of those assumptions is where the story gets interesting.

Result: Fair Value of $87.04 (UNDERVALUED)

Have a read of the narrative in full and understand what's behind the forecasts.

However, there are still clear pressure points, including reliance on hardware refresh cycles and heavy infrastructure spend, that could limit upside if demand or execution disappoints.

Find out about the key risks to this Fortinet narrative.

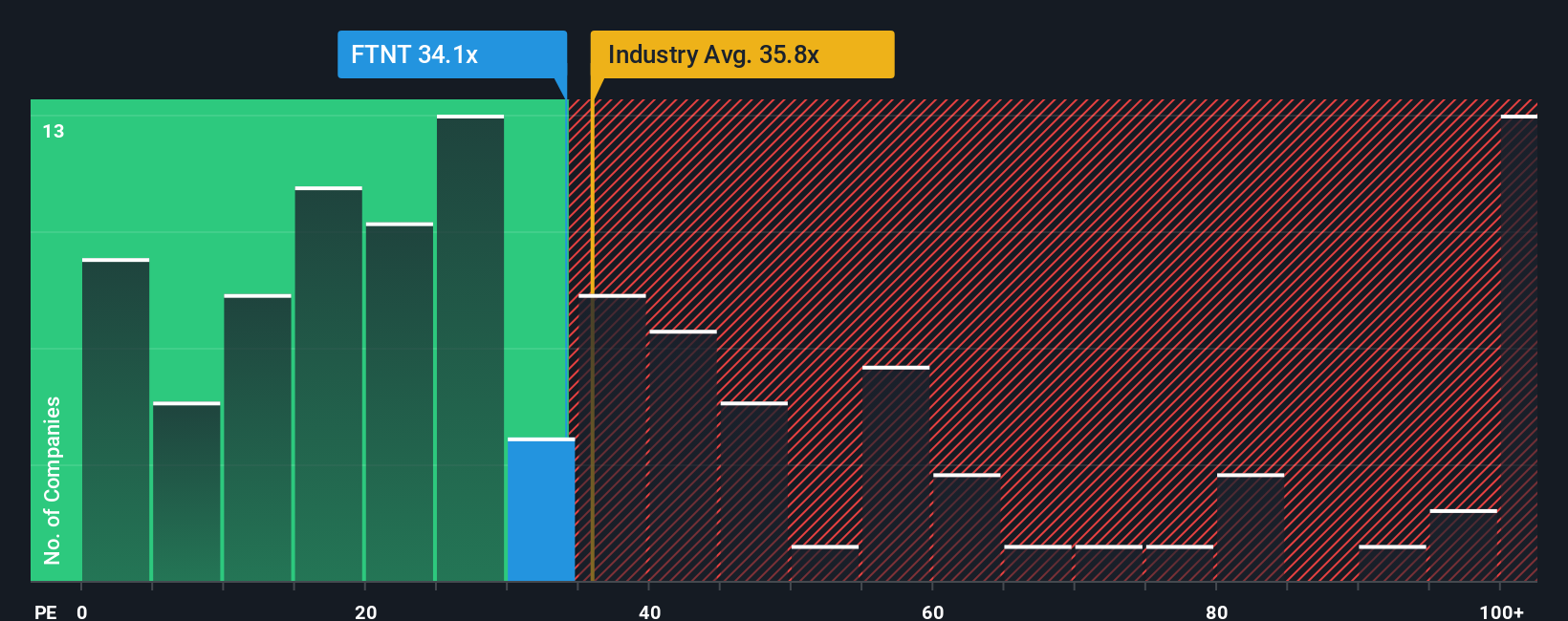

Another angle on value: earnings multiples send a different message

So far, the story leans on a fair value of $87.04 and a 1.7% discount, but the earnings multiple paints a less relaxed picture. Fortinet trades on a P/E of 34.3x, above the US Software industry at 26.4x and above its own fair ratio of 32.3x.

Peers on average sit much higher at 52.6x, which shows how wide the range of opinions is on what you should pay for this type of growth. If the market eventually gravitates closer to that 32.3x fair ratio, is today’s price a small premium worth paying or a signal to demand more of a cushion?

See what the numbers say about this price — find out in our valuation breakdown.

Build Your Own Fortinet Narrative

If you see the numbers differently or want to stress test these assumptions yourself, you can build a custom view of Fortinet in just a few minutes by starting with Do it your way.

A good starting point is our analysis highlighting 3 key rewards investors are optimistic about regarding Fortinet.

Ready for more investment ideas?

If Fortinet has sharpened your focus, do not stop here. Put a few minutes into scanning fresh opportunities so you are not relying on one story alone.

- Spot companies that look priced for pessimism and compare them using our 53 high quality undervalued stocks to see which ones deserve a closer look.

- Focus on resilience and capital preservation by starting with our 84 resilient stocks with low risk scores, especially if you want steadier profiles in your watchlist.

- Hunt for lesser known names with solid fundamentals by checking our screener containing 23 high quality undiscovered gems before they attract broader attention.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

Have feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team@simplywallst.com