- LIVE QUOTES

- LEARN

- HELP

Nasdaq

Nasdaq Wall Street Journal

Wall Street JournalEN

Assessing UDR (UDR) Valuation After Earnings Turnaround, 2026 Guidance And Ongoing Share Repurchases

UDR (UDR) drew fresh investor attention after reporting fourth quarter and full year 2025 results, issuing 2026 earnings guidance, and updating its share repurchase activity along with management commentary on rental trends and planned asset sales.

See our latest analysis for UDR.

At a latest share price of $38.09, UDR has seen a 10.47% 90 day share price return, while the 1 year total shareholder return of a 7.25% decline suggests recent momentum is building off a weaker longer term base.

If UDR’s recent earnings update has you rethinking where real assets fit in your portfolio, it could be a good moment to look at 23 top founder-led companies as a fresh set of ideas.

With earnings returning to profit, ongoing buybacks and analysts lifting price targets, UDR now trades below some estimates of intrinsic value. Is this a mispriced apartment REIT, or is the market already assuming future growth?

Most Popular Narrative: 5.7% Undervalued

With UDR last closing at $38.09 against a narrative fair value of about $40.38, the widely followed view suggests a modest valuation gap that hinges on specific growth and margin assumptions.

Analysts are assuming UDR's revenue will grow by 3.7% annually over the next 3 years.

Analysts assume that profit margins will increase from 7.4% today to 11.9% in 3 years time.

Want to see what sits behind that higher margin profile and steady top line build? The narrative leans on a tight mix of rent growth, occupancy, and a richer earnings multiple that is presented more like a growth story than a typical REIT. Curious which assumptions contribute most in that fair value stack?

Result: Fair Value of $40.38 (UNDERVALUED)

Have a read of the narrative in full and understand what's behind the forecasts.

However, you also need to weigh ongoing supply pressure in select Sunbelt and urban markets, as well as potential rent regulation in key coastal cities that could restrain growth.

Find out about the key risks to this UDR narrative.

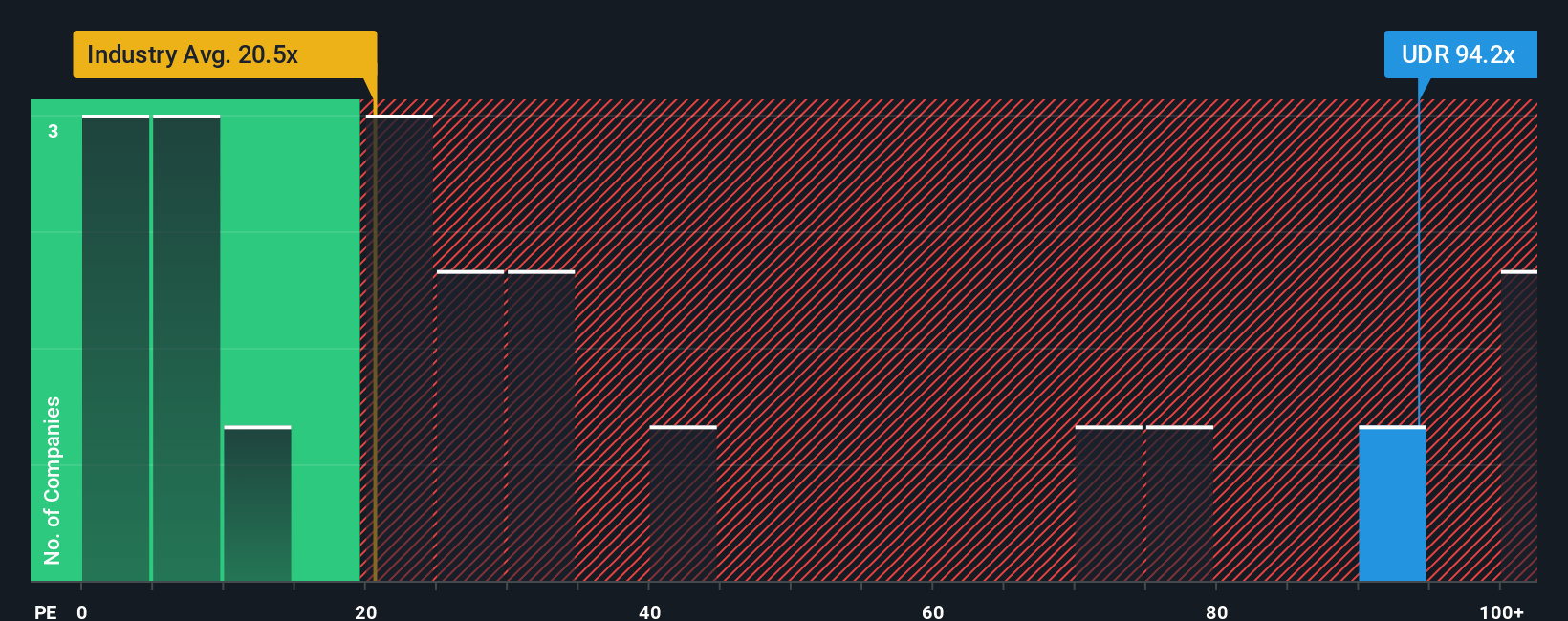

Another Angle on Valuation: P/E Tells a Tougher Story

The fair value narrative suggests UDR is 5.7% undervalued, but the current P/E of 33.5x paints a different picture. It sits well above the Residential REITs industry at 27.6x, the peer average at 27.7x, and a fair ratio of 25.6x, which implies meaningful valuation risk if sentiment cools. Which signal do you put more weight on?

See what the numbers say about this price — find out in our valuation breakdown.

Build Your Own UDR Narrative

If this take on UDR does not quite match your view, or you would rather lean on your own research, you can build a custom thesis grounded in the same data in just a few minutes, then stress test it with Do it your way.

A great starting point for your UDR research is our analysis highlighting 3 key rewards and 3 important warning signs that could impact your investment decision.

Ready to hunt for your next idea?

If UDR has sharpened your thinking about valuation, do not stop here. The real edge often comes from comparing several well chosen, data backed ideas side by side.

- Target potential mispricings by scanning 53 high quality undervalued stocks that pair solid fundamentals with prices that lag the underlying business quality.

- Strengthen your portfolio core with solid balance sheet and fundamentals stocks screener (45 results) focused on companies carrying manageable debt and resilient financial footing.

- Spot lesser known opportunities through our screener containing 23 high quality undiscovered gems that highlight quality businesses not yet crowded with attention.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

Have feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team@simplywallst.com