- LIVE QUOTES

- LEARN

- HELP

Nasdaq

Nasdaq Wall Street Journal

Wall Street JournalEN

A Look At Amentum Holdings (AMTM) Valuation After Q1 Earnings And Nuclear Contract Wins

Why Amentum’s latest earnings matter for investors

Amentum Holdings (AMTM) reported first quarter earnings with sales of US$3,237 million, compared with US$3,416 million a year earlier. Net income rose to US$44 million and earnings per share reached US$0.18, up from US$0.05.

See our latest analysis for Amentum Holdings.

Amentum’s latest results and reaffirmed 2026 revenue guidance landed after a choppy few weeks, with a 1-day share price return of 3.09% lifting the stock to US$31.00. This came even as the 7-day share price return of negative 17.40% and 30-day share price return of negative 10.92% contrasted with a stronger 90-day share price return of 44.25% and 1-year total shareholder return of 56.57%. Together, these figures indicate that recent momentum has cooled in the short term after a strong run into and around new contract wins and the deep borehole nuclear waste program.

If Amentum’s mix of digital and nuclear infrastructure has your attention, it could be a good moment to look across the sector using our list of 85 nuclear energy infrastructure stocks.

With earnings up, Q1 revenues reaffirmed for 2026 and the share price still trading at a discount to the average analyst target, the key question is whether Amentum is undervalued today or if the market already prices in future growth.

Most Popular Narrative: 7.3% Undervalued

At $31.00, Amentum’s share price sits below the most followed fair value estimate of $33.45, which is built off detailed long term earnings assumptions.

Ramp up of large, long duration awards such as the U.S. Space Force Range contract, Sellafield remediation and NASA Cosmos is set to convert the current $47 billion backlog and $20 billion of pending bids into higher run rate revenues and improved operating leverage, supporting sustained earnings growth.

Curious what kind of earnings profile those contracts imply, and what margin and growth mix backs that $33.45 fair value? The narrative leans on specific revenue, profit and valuation assumptions that tell a very different story from today’s P/E and headline results.

Result: Fair Value of $33.45 (UNDERVALUED)

Have a read of the narrative in full and understand what's behind the forecasts.

However, that story can change quickly if large contract awards are delayed by U.S. government funding shifts, or if execution issues on complex projects pressure margins.

Find out about the key risks to this Amentum Holdings narrative.

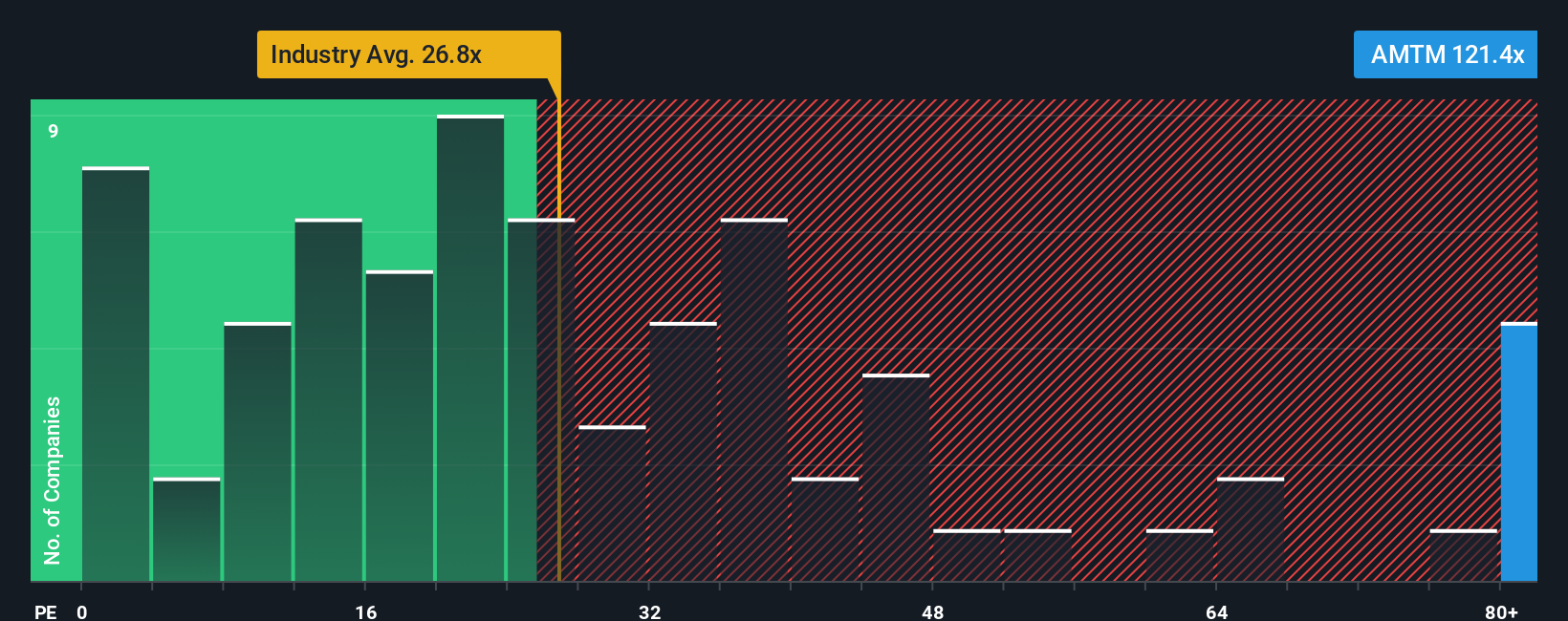

Another view: earnings multiples paint a tougher picture

While the consensus fair value points to a 7.3% undervaluation, Amentum’s current P/E of 77.2x is far higher than both the US Professional Services industry at 19.4x and its own fair ratio of 36.9x. That gap suggests meaningful valuation risk if sentiment or expectations cool from here, so which signal do you trust more?

See what the numbers say about this price — find out in our valuation breakdown.

Build Your Own Amentum Holdings Narrative

If parts of this story do not fully align with your view, or you would prefer to work directly from the numbers yourself, you can build a custom thesis in just a few minutes by starting with Do it your way.

A great starting point for your Amentum Holdings research is our analysis highlighting 3 key rewards and 2 important warning signs that could impact your investment decision.

Looking for more investment ideas?

If Amentum has sharpened your thinking, do not stop here. Use a focused screener to quickly surface other stocks that fit the kind of portfolio you want.

- Target potential upside by checking out our list of screener containing 23 high quality undiscovered gems that combine quality fundamentals with under-the-radar attention.

- Strengthen your foundation and see which companies pass our solid balance sheet and fundamentals stocks screener (45 results) so you can focus on businesses with robust financial footing.

- Lock in income ideas by reviewing our 12 dividend fortresses that highlight companies offering higher yields with an emphasis on stability.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

Have feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team@simplywallst.com