- LIVE QUOTES

- LEARN

- HELP

Nasdaq

Nasdaq Wall Street Journal

Wall Street JournalEN

A Look At ServiceTitan (TTAN) Valuation After Renewed Analyst Support And AI Resilience Focus

Recent analyst commentary on ServiceTitan (TTAN) has drawn fresh attention to the stock, highlighting positive views on its ability to handle AI related pressure and recession risk, even as the broader sector outlook appears more cautious.

See our latest analysis for ServiceTitan.

The recent 1 day share price return of 2.55% to US$62.74 comes after a sharp 30 day share price decline of 35.31% and a 1 year total shareholder return of 37.29% in the red. This suggests sentiment has been under pressure, even as fresh analyst support and the expanded revolving credit facility have put a spotlight back on the longer term story.

If AI related software names are on your radar, it could be worth scanning beyond ServiceTitan and checking out 57 profitable AI stocks that aren't just burning cash as a starting list of cash generating AI focused opportunities.

With the shares down 38.24% year to date and trading at an implied 27.46% discount to one intrinsic value estimate, plus an analyst target that sits well above the current US$62.74 price, you have to ask: is this a genuine opportunity, or are markets already baking in the growth story?

Most Popular Narrative: 54% Undervalued

With ServiceTitan last closing at $62.74 against a widely followed fair value estimate of $136.33, the current price sits well below that narrative view and puts the focus squarely on the growth and margin assumptions underpinning that gap.

Deeper penetration of AI driven Pro products such as Field Pro, Dispatch Pro, virtual agents and the MAX program is expected to automate more of the workflow from call to cash, supporting faster subscription growth and higher usage based revenue over time.

Want to see what kind of revenue ramp and margin shift that assumes? The narrative leans on stronger subscription traction, richer payments economics and higher earnings power than today. Curious which specific growth and profitability milestones need to line up to support that $136.33 fair value and the implied future earnings multiple? The full narrative breaks down those moving parts in detail.

Result: Fair Value of $136.33 (UNDERVALUED)

Have a read of the narrative in full and understand what's behind the forecasts.

However, this hinges on AI driven Pro tools and fintech adoption successfully delivering clear customer ROI, and on expansion into commercial and construction not stalling against entrenched competitors.

Find out about the key risks to this ServiceTitan narrative.

Another Way To Look At It

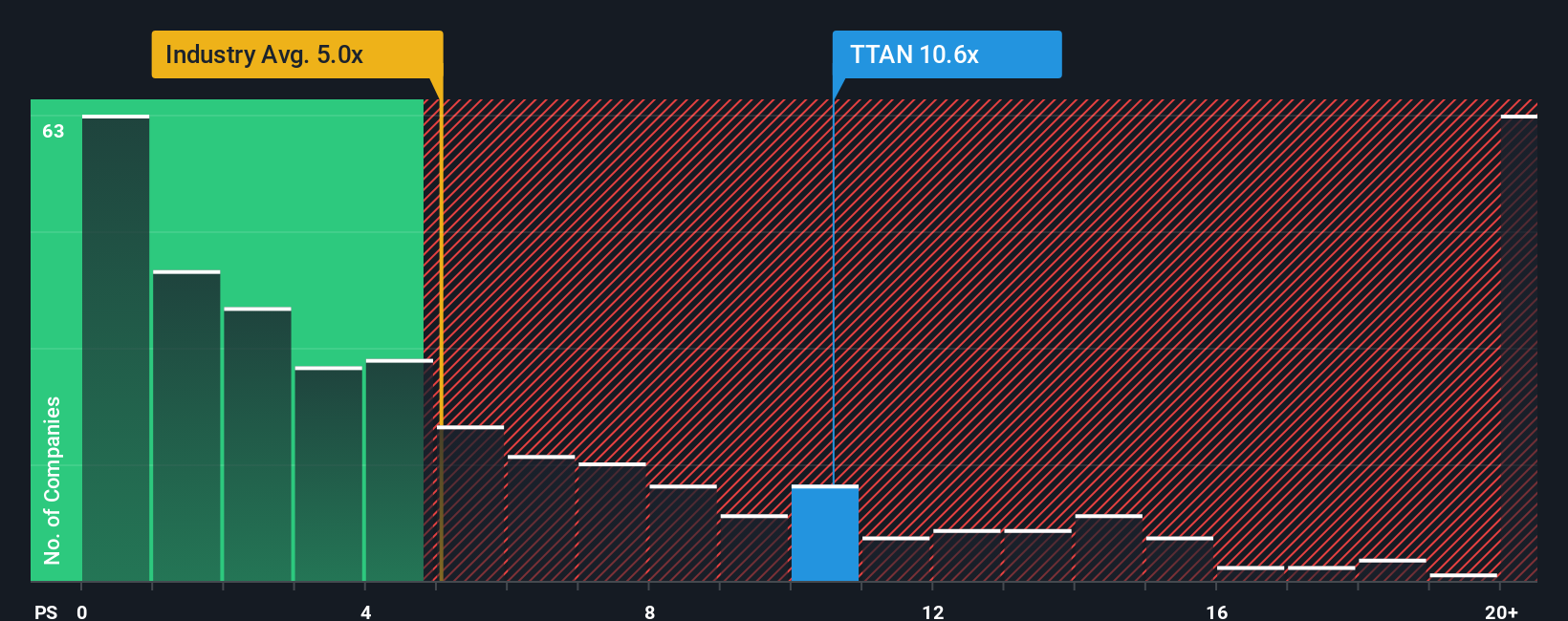

On sales, ServiceTitan does not look cheap. The shares trade on a P/S of 6.4x, compared with 3.5x for the wider US software group and a fair ratio of 5x from our model. That gap suggests less margin for error if the growth and margin story slips.

See what the numbers say about this price — find out in our valuation breakdown.

Build Your Own ServiceTitan Narrative

If you look at these numbers and reach a different conclusion, or simply want to test your own assumptions against the data, you can build and stress test a custom ServiceTitan storyline in just a few minutes. Then you can refine it further as new information comes through, all by choosing to Do it your way.

A great starting point for your ServiceTitan research is our analysis highlighting 4 key rewards and 2 important warning signs that could impact your investment decision.

Looking for more investment ideas?

If you stop your research with a single stock, you risk missing other opportunities that could fit your goals even better. Widen your search with a few targeted screens.

- Spot potential value opportunities early by scanning our 53 high quality undervalued stocks, which pairs quality fundamentals with prices that may not fully reflect them.

- Prioritise resilience by checking companies in the 85 resilient stocks with low risk scores, where business models and balance sheets score well on our risk checks.

- Hunt for potential future leaders using the screener containing 23 high quality undiscovered gems and see which quieter names share traits with already successful businesses.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

Have feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team@simplywallst.com