- LIVE QUOTES

- LEARN

- HELP

Nasdaq

Nasdaq Wall Street Journal

Wall Street JournalEN

Assessing Beacon Financial (BBT) Valuation After Recent Share Price Momentum And Merger Synergy Hopes

Beacon Financial (BBT) has caught investor attention after recent share price moves, with the stock showing a mix of short term pullback and stronger performance over the past month and past 3 months.

See our latest analysis for Beacon Financial.

With the share price at $30.68, Beacon Financial’s recent pullback over the last week sits against a much stronger backdrop, with a 30 day share price return of 14.52% and a 90 day share price return of 21.36%, pointing to building momentum even though the 1 year total shareholder return is 6.85%.

If this kind of move in a regional bank has you thinking about what else could be setting up for a rerating, it can be worth scanning our 23 top founder-led companies as a starting list of ideas.

With revenue at $511.6m, net income at $90.3m and some room to analyst targets plus a quoted intrinsic discount, the real question is whether Beacon Financial is still mispriced or if the market is already factoring in future growth.

Most Popular Narrative: 6.1% Undervalued

Beacon Financial’s most followed narrative pegs fair value at $32.67, a touch above the last close at $30.68. This helps put recent price moves into context.

Realization of merger cost synergies, including further headcount reductions and vendor consolidation after the core conversion, should reduce operating expenses toward the targeted quarterly run rate and support expanding net margins and earnings.

Curious what justifies that modest gap to fair value? The narrative leans on sharp revenue expansion, much higher profit margins and a very different earnings multiple by 2028.

Result: Fair Value of $32.67 (UNDERVALUED)

Have a read of the narrative in full and understand what's behind the forecasts.

However, this depends on successful merger integration and on credit costs for troubled assets and commercial real estate remaining within the ranges analysts currently expect.

Find out about the key risks to this Beacon Financial narrative.

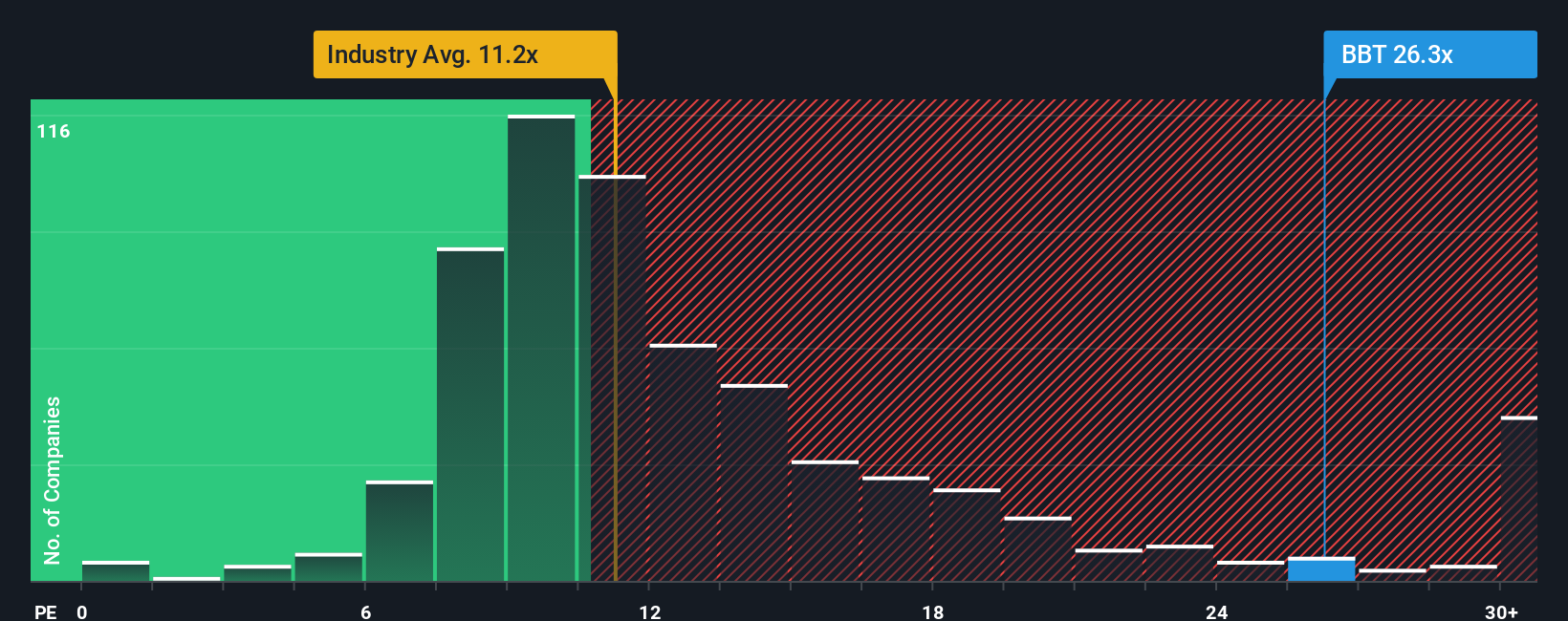

Another View: Earnings Multiple Sends A Different Signal

Those fair value models point to upside, but the current P/E of 28.6x tells a different story. That is more than double the US Banks industry at 11.8x and above the 12.2x peer average, and even sits above the 21.9x fair ratio our work suggests the market could move toward. For you, that gap raises a simple question: is this a rerating in progress or valuation risk building in plain sight?

See what the numbers say about this price — find out in our valuation breakdown.

Build Your Own Beacon Financial Narrative

If you look at these numbers and reach a different conclusion, that is the point. You can weigh the data yourself and Do it your way in just a few minutes.

A great starting point for your Beacon Financial research is our analysis highlighting 3 key rewards and 1 important warning sign that could impact your investment decision.

Looking for more investment ideas?

If Beacon Financial has sharpened your thinking, do not stop here, you could miss out on other opportunities lining up for your watchlist.

- Spot potential value plays early by running your filters through our 53 high quality undervalued stocks that match solid fundamentals with appealing prices.

- Secure a stream of income focused ideas by checking the 13 dividend fortresses that emphasise higher yields with durability in mind.

- Prioritise resilience by reviewing the 85 resilient stocks with low risk scores designed to highlight companies with more defensive characteristics.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

Have feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team@simplywallst.com