- LIVE QUOTES

- LEARN

- HELP

Nasdaq

Nasdaq Wall Street Journal

Wall Street JournalEN

Patrick Industries (PATK) Valuation Check After Strong Q4 Results Dividend Hike And Recent Acquisitions

Patrick Industries (PATK) is back in focus after its latest quarterly update, which combined stronger fourth quarter results with a higher dividend and ongoing acquisition activity. This has put its capital allocation approach under the spotlight for investors.

See our latest analysis for Patrick Industries.

The latest earnings update, higher dividend and completed multi year buyback have arrived alongside strong momentum in the share price, with a 30 day share price return of 19.06%, a 90 day share price return of 43.10% and a 1 year total shareholder return of 51.94% at a last close of US$143.10.

If this mix of capital returns and acquisitions has caught your attention, it could be a good moment to broaden your search and look at 23 top founder-led companies as potential next ideas.

With the shares near US$143 and recent returns well ahead of the wider market, plus an internal estimate pointing to roughly a 20% discount to intrinsic value, you have to ask: is there still a buying opportunity here, or is the market already pricing in future growth?

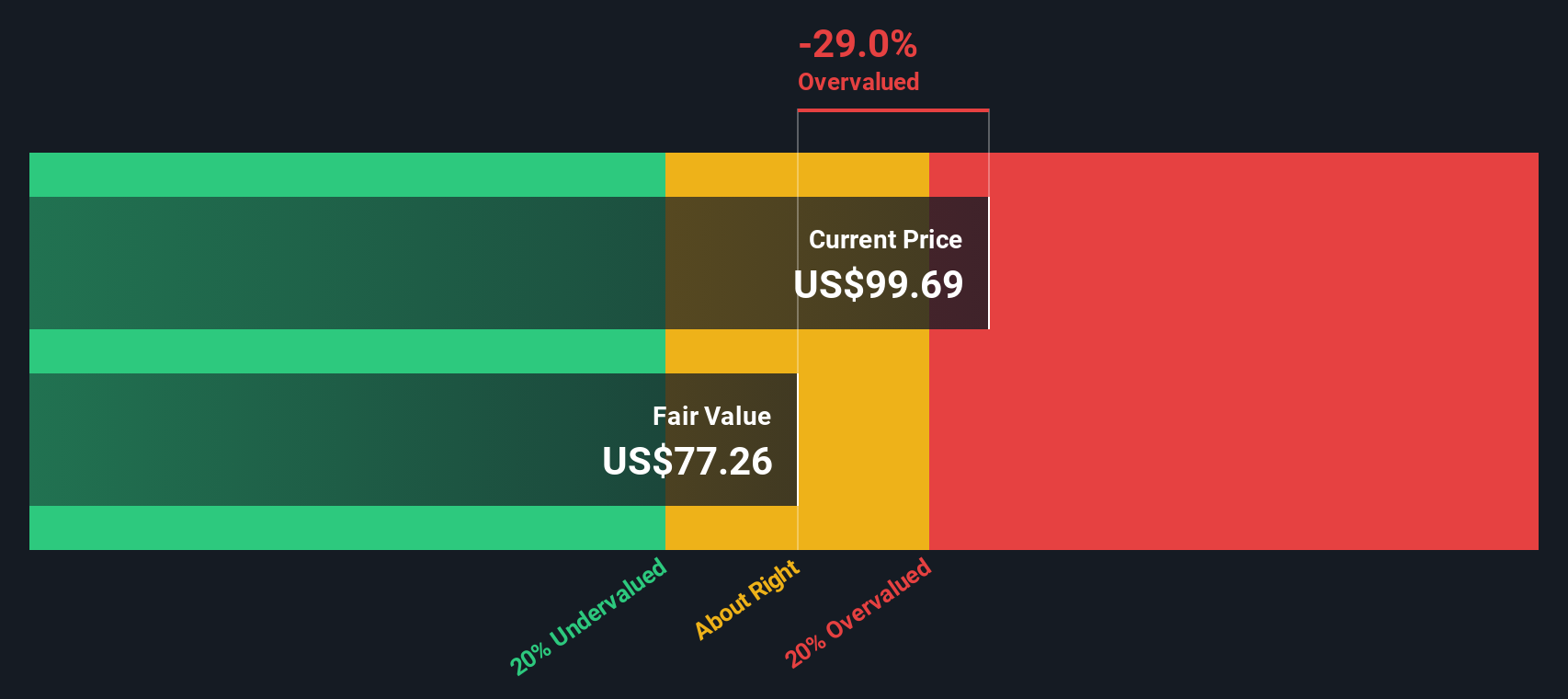

Most Popular Narrative: 7.6% Overvalued

Patrick Industries’ current share price of $143.10 sits above the most followed fair value estimate of $133, which rests on detailed cash flow and earnings assumptions.

Strategic investments in automation, advanced manufacturing processes, and full solution models (e.g., greater integration of technology and materials across business units) are expected to yield operational efficiencies and scale benefits, supporting gross margin improvement and higher earnings over time.

Curious how this focus on efficiency supports that $133 figure? The narrative leans heavily on profit margins, steadier aftermarket revenue and a reset earnings multiple. The discount rate is already set. The real question is whether those assumptions feel ambitious or comfortable to you.

Based on this narrative, the fair value of $133 is built using an 8.79% discount rate, earnings and margin forecasts, and a future earnings multiple that sits below earlier estimates but above the current analyst target of $137.20. The result is a view that the recent share price strength has moved the stock beyond that fair value anchor, even though Simply Wall St’s own discounted cash flow work and separate value checks still flag Patrick Industries as trading below some intrinsic value estimates.

Result: Fair Value of $133 (OVERVALUED)

Have a read of the narrative in full and understand what's behind the forecasts.

However, remember that exposure to cyclical RV and marine markets, along with the execution risk around ongoing acquisitions, could quickly challenge those fair value assumptions if conditions turn.

Find out about the key risks to this Patrick Industries narrative.

Another View: Cash Flows Point To Undervaluation

While the most followed fair value narrative suggests Patrick Industries is 7.6% overvalued at around $143, our DCF model tells a different story. On that cash flow view, the shares trade roughly 20% below an estimated intrinsic value of about $180. Which lens feels more convincing to you?

Look into how the SWS DCF model arrives at its fair value.

Simply Wall St performs a discounted cash flow (DCF) on every stock in the world every day (check out Patrick Industries for example). We show the entire calculation in full. You can track the result in your watchlist or portfolio and be alerted when this changes, or use our stock screener to discover 55 high quality undervalued stocks. If you save a screener we even alert you when new companies match - so you never miss a potential opportunity.

Build Your Own Patrick Industries Narrative

If you see the numbers differently, or simply prefer to test your own assumptions, you can build a fresh Patrick Industries thesis in just a few minutes by starting with Do it your way.

A great starting point for your Patrick Industries research is our analysis highlighting 2 key rewards and 2 important warning signs that could impact your investment decision.

Looking for more investment ideas?

If you are serious about tightening up your watchlist, now is the time to broaden your search with a few focused screeners that surface very different kinds of opportunities.

- Target potential mispricing by reviewing companies our system flags as 55 high quality undervalued stocks based on their cash flows and balance sheet strength.

- Strengthen the core of your portfolio with names from our solid balance sheet and fundamentals stocks screener (45 results) that aim to prioritize financial resilience.

- Spot under followed opportunities before they hit the mainstream using our screener containing 23 high quality undiscovered gems that highlight companies with strong fundamentals.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

Have feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team@simplywallst.com