- LIVE QUOTES

- LEARN

- HELP

Nasdaq

Nasdaq Wall Street Journal

Wall Street JournalEN

Hawkins (HWKN) Valuation Check After NanoStack Membrane Win At Orange County Water District

Hawkins (HWKN) is in focus after subsidiary WaterSurplus completed a multi year NanoStack membrane pilot at Orange County Water District, which led OCWD to move ahead with 1,050 membranes for its groundwater system.

See our latest analysis for Hawkins.

At a share price of $144.15, Hawkins has seen a 10.91% 7 day share price return and a 13.93% 90 day share price return. Its 1 year and 5 year total shareholder returns of 28.80% and over 4x respectively suggest momentum that has been built over time rather than just recently.

If this water treatment progress has caught your attention, it could be a good moment to broaden your search and check out our screener of 24 power grid technology and infrastructure stocks as another way to find infrastructure related opportunities.

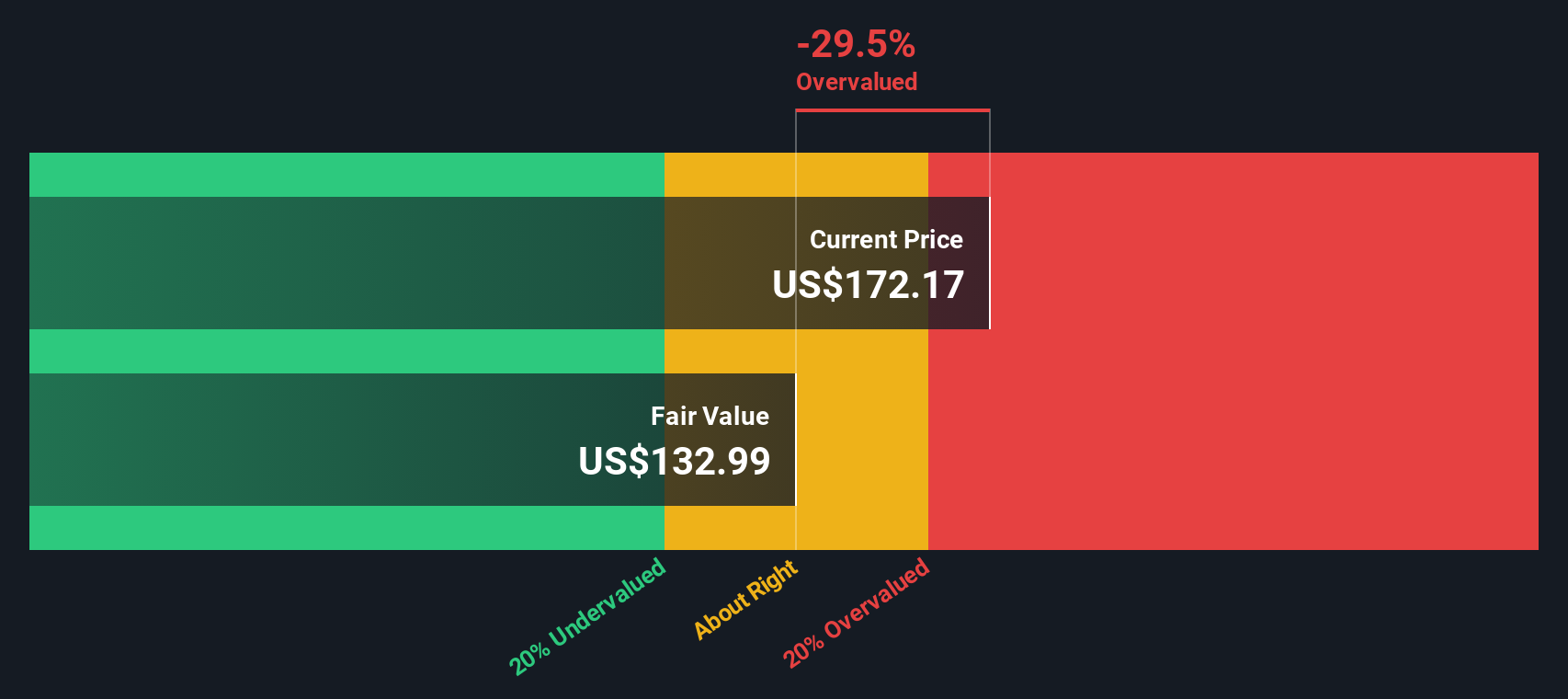

With Hawkins trading at $144.15, showing strong multi year total returns and a sizable discount to a $188 analyst target, you have to ask: is there still value on the table, or is the market already pricing in future growth?

Price to Earnings of 36.6x: Is it justified?

Hawkins finished at $144.15, and on a P/E of 36.6x it sits well above both its industry and peer averages. This points to an overvalued setup based on this lens.

The P/E ratio compares the current share price to earnings per share. A higher multiple usually reflects the market paying more for each dollar of earnings. For a chemicals and water treatment business like Hawkins, that often signals investors are comfortable tying a premium to its earnings profile and segment mix.

Here, the premium is clear. Hawkins is on a 36.6x P/E, compared with the US Chemicals industry at 26.6x and a peer average of 19.9x. The market is therefore assigning materially richer terms to Hawkins than to both its sector and closer peers. Relative to an estimated fair P/E of 18.2x, the current multiple also sits significantly higher. This is a level the market could move toward if sentiment or growth expectations cool.

Explore the SWS fair ratio for Hawkins

Result: Price-to-Earnings of 36.6x (OVERVALUED)

However, that premium P/E could be vulnerable if Hawkins’ revenue or net income growth rates of 5.6% and 9.3% slow, or if sector sentiment cools.

Find out about the key risks to this Hawkins narrative.

Another view through the SWS DCF model

The high P/E points to rich pricing, but our DCF model tells a similar story rather than easing those concerns. On that measure, Hawkins at $144.15 sits above an estimated future cash flow value of $111.58, which suggests the shares screen as overvalued on cash flows too. If both earnings and cash flow signals are this stretched, it raises the question of what the market is really paying up for.

Look into how the SWS DCF model arrives at its fair value.

Simply Wall St performs a discounted cash flow (DCF) on every stock in the world every day (check out Hawkins for example). We show the entire calculation in full. You can track the result in your watchlist or portfolio and be alerted when this changes, or use our stock screener to discover 55 high quality undervalued stocks. If you save a screener we even alert you when new companies match - so you never miss a potential opportunity.

Build Your Own Hawkins Narrative

If you look at these numbers and reach a different conclusion, or simply prefer to test the assumptions yourself, you can build a tailored Hawkins view in just a few minutes, starting with Do it your way.

A great starting point for your Hawkins research is our analysis highlighting 3 key rewards and 1 important warning sign that could impact your investment decision.

Ready to hunt for your next idea?

If Hawkins is already on your radar, do not stop there. Use the Simply Wall St screener to quickly surface other opportunities that fit your style.

- Target value potential by reviewing 55 high quality undervalued stocks that combine quality fundamentals with prices that may not fully reflect their profiles.

- Prioritise resilience by scanning 85 resilient stocks with low risk scores if you want businesses with fewer red flags on key risk checks.

- Spot under followed stories by using our screener containing 23 high quality undiscovered gems that the broader market may not be focusing on yet.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

Have feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team@simplywallst.com