- LIVE QUOTES

- LEARN

- HELP

Nasdaq

Nasdaq Wall Street Journal

Wall Street JournalEN

A Look At Snap On (SNA) Valuation After 2025 Earnings And Steady Dividend Commitment

Snap-on (SNA) has just reported fourth quarter and full year 2025 results, giving investors fresh numbers on sales, earnings and cash returns, including another quarterly dividend that extends its long dividend record.

See our latest analysis for Snap-on.

After these results, Snap-on’s recent share price moves have been fairly resilient, with the stock at US$378.55 and a 90 day share price return of 14.72%, alongside a 1 year total shareholder return of 14.46% and 5 year total shareholder return of 124.74%. This suggests that long term holders have so far been rewarded even as near term sentiment shifts around demand and product mix.

If Snap-on’s steady profile has you thinking about where else durable growth and income stories might be hiding, it could be a good time to broaden your search with our 23 top founder-led companies.

With earnings steady, a long dividend record and the share price already near some analyst targets, the key question now is whether Snap-on is still trading below its intrinsic value or whether the market is already pricing in future growth.

Most Popular Narrative: 35.5% Overvalued

Robbo’s narrative pegs Snap-on’s fair value at $279.41, which sits well below the recent $378.55 share price, setting up a clear valuation gap to unpack.

Over the past two to three decades, Chinese manufacturing has supplied the world with cheap and generally reliable tools. For an American business to not only survive this period but prosper is impressive, and worth a closer look. With the shift toward more protectionist policies aimed at encouraging domestic manufacturing, US companies already producing on home soil may now be well positioned. Snap-on fits this description and is the focus of today’s deep dive.

Curious what sits behind that lower fair value despite strong margins and a long history of steady progress? The narrative leans heavily on conservative growth, firm profitability assumptions and a disciplined profit multiple that contrasts with how the market is currently pricing the stock.

Result: Fair Value of $279.41 (OVERVALUED)

Have a read of the narrative in full and understand what's behind the forecasts.

However, shifts in automotive demand or financial strain on franchisees could put pressure on Snap-on’s sales model and challenge the idea that current margins and pricing power are durable.

Find out about the key risks to this Snap-on narrative.

Another View on Valuation

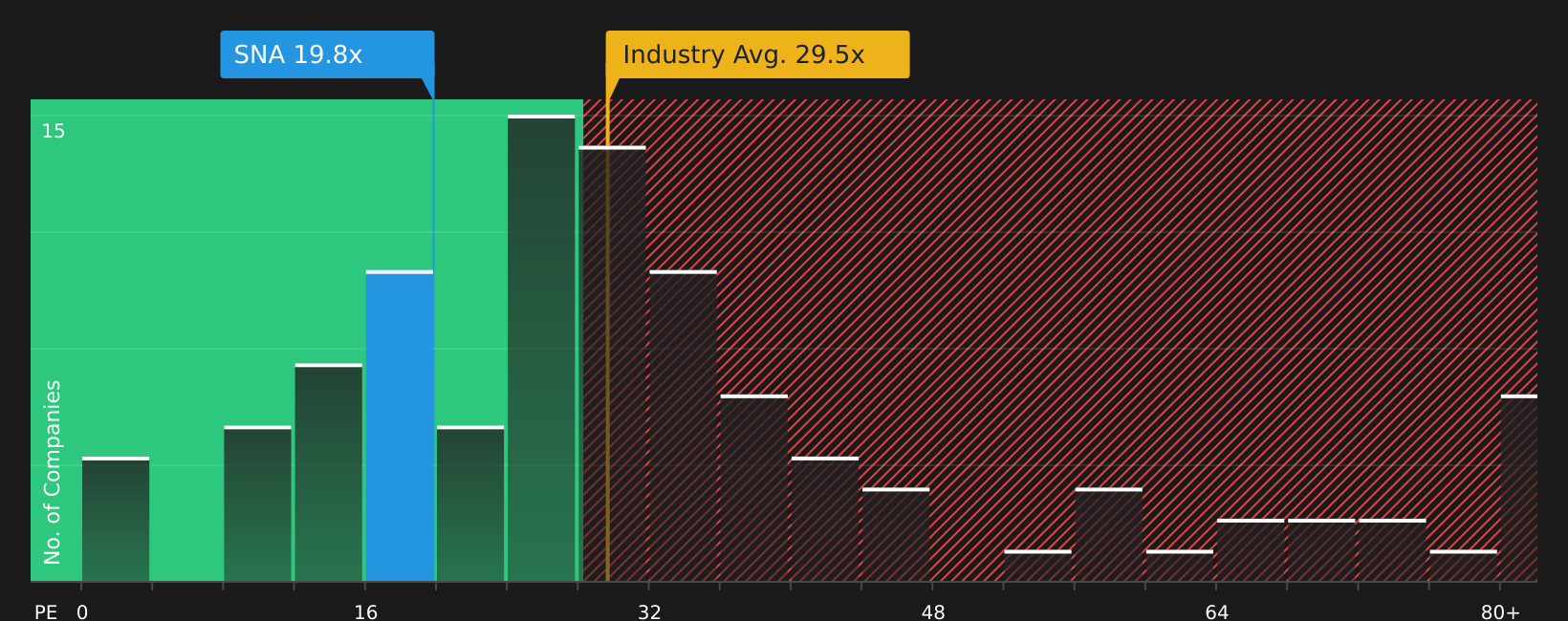

Robbo’s narrative flags Snap-on as about 35.5% overvalued against a $279.41 fair value, but our P/E work tells a different story. At 19.4x earnings, the shares sit well below the US Machinery average of 29.8x, a peer average of 32.4x, and a fair ratio of 24.1x that the market could move towards.

That mix of a premium share price versus one narrative fair value and a discount versus sector and fair ratio benchmarks leaves you with a practical question: is the risk that the valuation compresses toward Robbo’s number, or that the multiple drifts closer to where similar businesses trade?

See what the numbers say about this price — find out in our valuation breakdown.

Build Your Own Snap-on Narrative

If you look at these numbers and reach a different conclusion, or simply prefer to test the assumptions yourself, you can build a custom Snap-on thesis in just a few minutes with Do it your way.

A great starting point for your Snap-on research is our analysis highlighting 4 key rewards and 1 important warning sign that could impact your investment decision.

Looking for more investment ideas?

If Snap-on is on your radar but you want a broader watchlist, it makes sense to line up a few other ideas that match your style and risk comfort.

- Target potential mispricings by scanning a curated set of 55 high quality undervalued stocks that pair quality fundamentals with prices that may not fully reflect them.

- Strengthen your income stream by checking out 16 dividend fortresses that focus on higher yielding payers with more robust profiles.

- Protect your downside first by reviewing 85 resilient stocks with low risk scores built around companies with lower risk scores and steadier fundamentals.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

Have feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team@simplywallst.com