- LIVE QUOTES

- LEARN

- HELP

Nasdaq

Nasdaq Wall Street Journal

Wall Street JournalEN

Assessing Ensign Group (ENSG) Valuation After Strong Results Guidance And Skilled Nursing Expansion

Ensign Group (ENSG) shares were in focus after the company paired strong fourth quarter and full year 2025 results with fresh 2026 guidance, as well as an expanded skilled nursing footprint across multiple states.

See our latest analysis for Ensign Group.

Those results and the new 2026 guidance arrived alongside an acceleration in share price momentum, with a 1-month share price return of 20.54% and year to date share price return of 23.28%, while the 1-year total shareholder return sits at 65.75% on the back of steady acquisition activity and expanding skilled nursing capacity.

If this kind of sustained strength has your attention, it could be a good moment to see what else is working in healthcare. You can start with our screener of 24 healthcare AI stocks.

With Ensign shares up sharply over 1 year and the stock now trading close to the US$220.40 analyst price target, the key consideration is whether there is still a buying opportunity or if the market is already pricing in future growth.

Preferred P/E of 36x: Is it justified?

At a last close of $214.41, Ensign Group is trading on a P/E of 36x, which screens as expensive compared with both its peers and the wider US Healthcare sector.

The P/E multiple tells you how many dollars investors are paying today for each dollar of current earnings, and it is a common yardstick for healthcare service operators with consistent profitability. For Ensign, this sits against earnings that have grown 12.9% per year over the past 5 years and are forecast to grow 13.22% per year.

That growth profile is positive, yet the gap between price and fundamentals is clear. The current 36x P/E is well above the US Healthcare industry average of 23.5x and also ahead of the peer average of 20.3x, suggesting the market is paying a premium compared to similar companies. Our fair P/E estimate of 27.2x points to a level the market could move towards if enthusiasm for the stock cools and pricing tracks closer to earnings strength.

Explore the SWS fair ratio for Ensign Group

Result: Price-to-Earnings of 36x (OVERVALUED)

However, the premium 36x P/E leaves little room for disappointment if earnings or acquisition driven expansion underperform expectations, or if sector wide sentiment cools.

Find out about the key risks to this Ensign Group narrative.

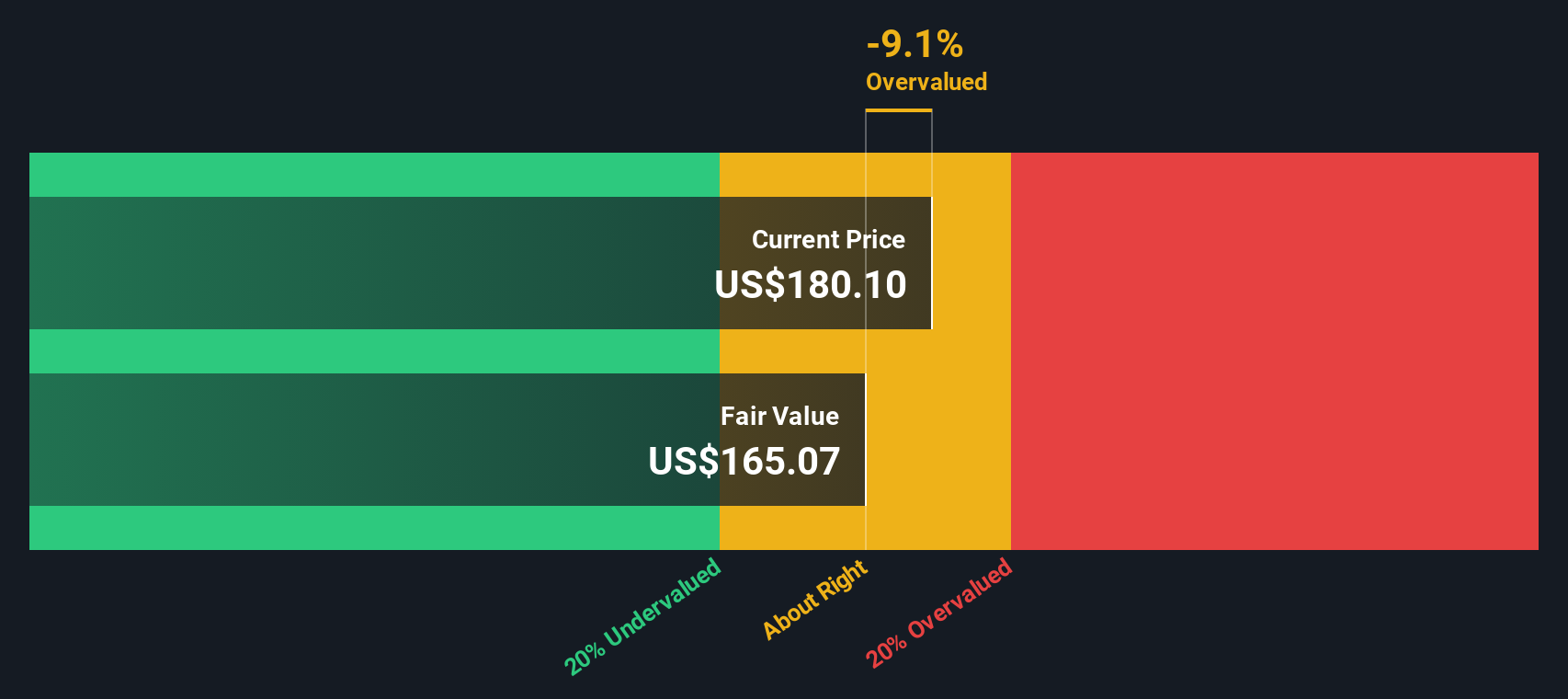

Another View: Cash Flows Point To A Different Story

While the P/E of 36x makes Ensign Group look expensive against peers, our DCF model goes a step further and values the shares at $148.89 based on future cash flows. With the current price at $214.41, that implies the stock is trading well above that estimate. This raises the question of which signal you might consider more informative.

Look into how the SWS DCF model arrives at its fair value.

Simply Wall St performs a discounted cash flow (DCF) on every stock in the world every day (check out Ensign Group for example). We show the entire calculation in full. You can track the result in your watchlist or portfolio and be alerted when this changes, or use our stock screener to discover 55 high quality undervalued stocks. If you save a screener we even alert you when new companies match - so you never miss a potential opportunity.

Build Your Own Ensign Group Narrative

If you look at this and feel you would rather trust your own view, you can pull the same data, shape your own story and Do it your way in under 3 minutes.

A good starting point is our analysis highlighting 2 key rewards investors are optimistic about regarding Ensign Group.

Ready for more investment ideas?

If Ensign has sharpened your thinking, do not stop here. Use the Simply Wall St Screener to quickly spot other opportunities that fit your style.

- Target value upfront by scanning our list of 55 high quality undervalued stocks that combine price appeal with underlying business strength.

- Prioritise resilience by reviewing 84 resilient stocks with low risk scores that score well on stability and downside protection.

- Get ahead of the crowd by checking our screener containing 23 high quality undiscovered gems that the wider market may not be focusing on yet.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

Have feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team@simplywallst.com