- LIVE QUOTES

- LEARN

- HELP

Nasdaq

Nasdaq Wall Street Journal

Wall Street JournalEN

Assessing Eastern Bankshares (EBC) Valuation After Recent Share Price Momentum

Why Eastern Bankshares is on investors’ radar today

Eastern Bankshares (EBC) has drawn attention after recent share performance, with the stock showing gains over the past month and past 3 months, prompting investors to reassess its valuation and earnings profile.

See our latest analysis for Eastern Bankshares.

While the share price slipped 0.5% over the last session, Eastern Bankshares has a 30 day share price return of 12.3% and a 90 day gain of 21.6%, alongside a 1 year total shareholder return of 19.5%. This points to improving momentum as investors reassess its earnings and risk profile around the current US$21.42 level.

If this bank stock has caught your eye, it can be useful to widen the lens and check out other financial names too, including our screener of 23 top founder-led companies.

With Eastern Bankshares trading at US$21.42 and an estimated intrinsic value suggesting a sizeable discount, the key question is whether the recent share gains still leave room for upside or if the market is already pricing in future growth.

Most Popular Narrative: 8.5% Undervalued

Eastern Bankshares last closed at $21.42, compared with a widely followed fair value estimate of about $23.42, which puts the current price below that narrative view and turns attention to what is driving that gap.

The analysts have a consensus price target of $19.5 for Eastern Bankshares based on their expectations of its future earnings growth, profit margins and other risk factors. However, there is a degree of disagreement amongst analysts, with the most bullish reporting a price target of $21.0, and the most bearish reporting a price target of just $17.0.

Want to see what sits behind that higher fair value than the consensus target range? Revenue, margins and the future earnings multiple all pull in different directions. The full narrative lays out how those moving parts come together.

Result: Fair Value of $23.42 (UNDERVALUED)

Have a read of the narrative in full and understand what's behind the forecasts.

However, that fair value case can come under pressure if office related credit issues flare up again, or if higher reserves weigh more heavily on profitability than expected.

Find out about the key risks to this Eastern Bankshares narrative.

Another way to look at the valuation

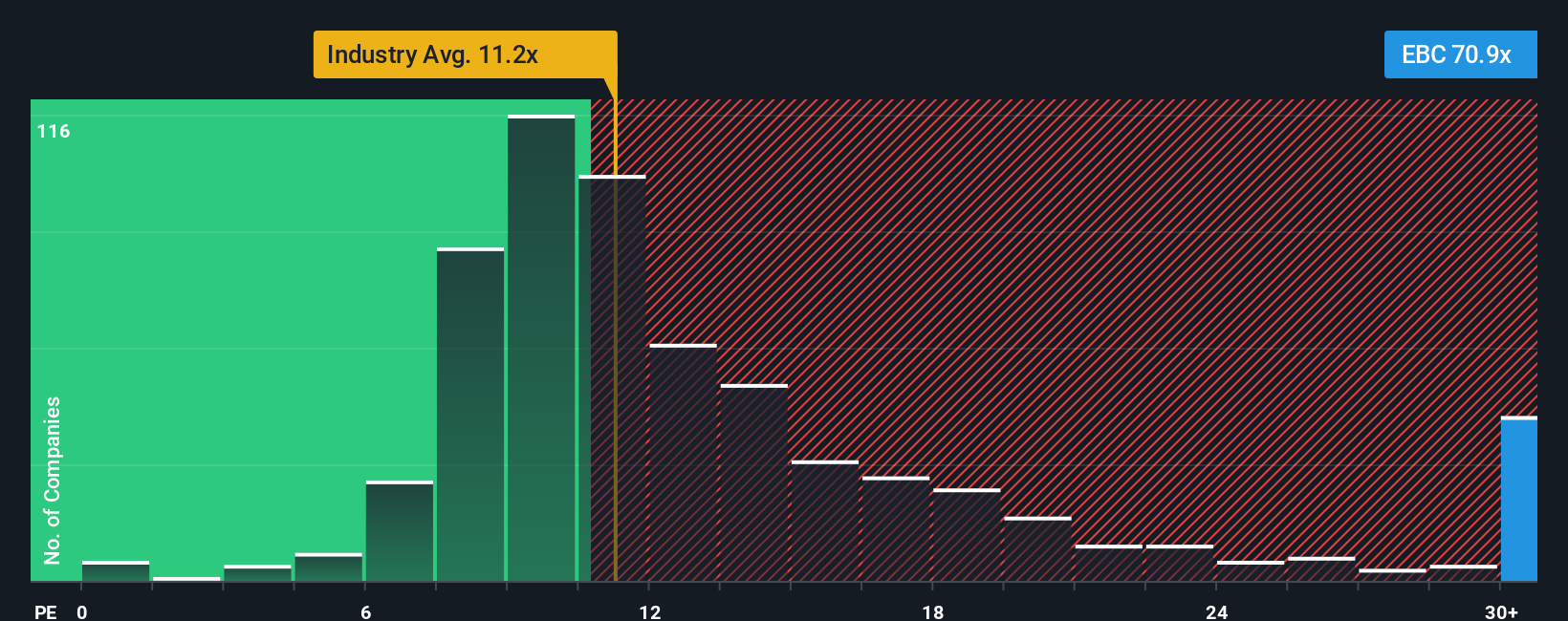

The fair value narrative paints Eastern Bankshares as 8.5% undervalued, but its P/E of 54.8x tells a very different story. That is far above the US Banks industry at 11.8x, the peer average at 37.5x, and even the fair ratio of 25.8x that the market could move toward.

In practice, that kind of premium P/E can mean valuation risk if earnings or sentiment cool, even if some models still point to upside. The question for you is whether you see this as justified by the growth outlook or as a sign expectations are already running hot.

See what the numbers say about this price — find out in our valuation breakdown.

Build Your Own Eastern Bankshares Narrative

If you see the numbers differently or would rather test your own assumptions directly in the model, you can build a tailored view in minutes: Do it your way.

A great starting point for your Eastern Bankshares research is our analysis highlighting 2 key rewards and 2 important warning signs that could impact your investment decision.

Looking for more investment ideas?

If Eastern Bankshares has sharpened your focus, do not stop here; broaden your watchlist and give yourself more quality options to compare before you commit.

- Target potential mispricings by scanning 55 high quality undervalued stocks that pair solid fundamentals with attractive entry points.

- Strengthen your income stream by checking out 16 dividend fortresses that aim for higher yields with a focus on resilience.

- Prioritise capital protection by reviewing 85 resilient stocks with low risk scores built to keep overall risk scores in check.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

Have feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team@simplywallst.com