- LIVE QUOTES

- LEARN

- HELP

Nasdaq

Nasdaq Wall Street Journal

Wall Street JournalEN

Pilgrim's Pride (PPC) Q4 EPS Drop Reinforces Bearish Earnings Decline Narratives

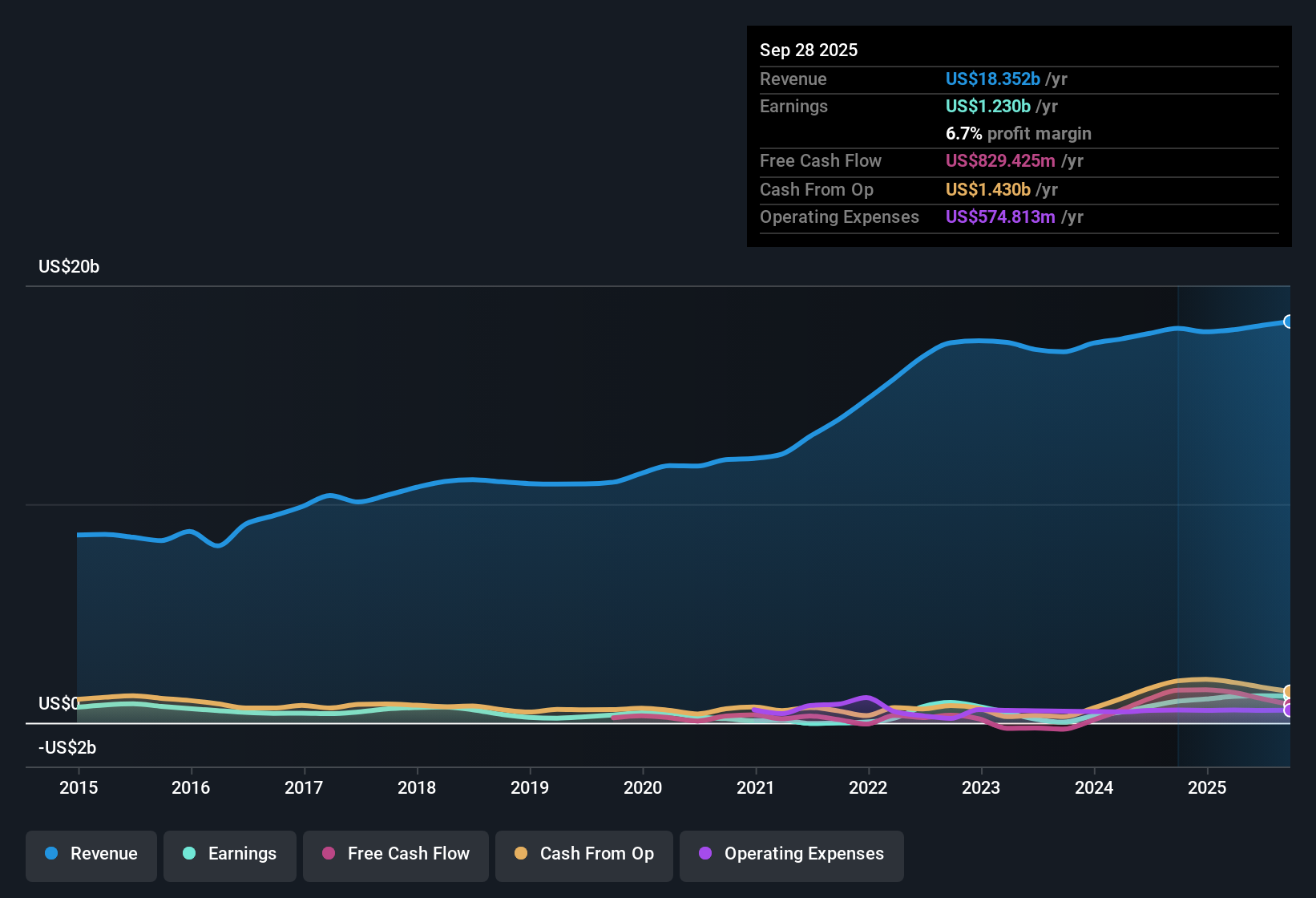

Pilgrim's Pride FY 2025 earnings snapshot

Pilgrim's Pride (PPC) has rounded out FY 2025 with Q4 revenue of US$4.5b and EPS of US$0.37, capping a year where trailing 12 month EPS came in at US$4.56 on revenue of US$18.5b. Over recent periods the company has seen quarterly revenue move from US$4.4b in Q4 2024 to roughly US$4.8b in Q2 and Q3 2025 before landing at US$4.5b in Q4 2025, while quarterly EPS has ranged from US$0.99 to US$1.50 through 2024 and early 2025 before the latest print. With trailing net margins holding in the mid single digits, this set of results places more attention on how sustainable profitability looks from here.

See our full analysis for Pilgrim's Pride.With the headline numbers on the table, the next step is to see how this latest report lines up with the prevailing narratives about Pilgrim's Pride's growth, earnings power, and risks.

See what the community is saying about Pilgrim's Pride

Margin picture: 5.9% net on US$18.5b

- On a trailing 12 month basis, Pilgrim's Pride generated US$18.5b of revenue and US$1.08b of net income, which works out to a 5.9% net margin compared with 6.1% a year earlier.

- Bulls focus on the long run, arguing that the strong five year earnings growth of 41.8% per year and investments in higher value Prepared Foods and branded products could support healthier margins over time. The small pullback from 6.1% to 5.9% highlights that execution on new plants and cost programs needs to work well for that optimistic view to line up with the current profitability profile.

- Supporters of the bullish view point to the mix shift toward Case Ready and Prepared Foods as a way to support EBITDA and net margins, while the latest margin level shows only a modest change so far.

- They also highlight ongoing operational efficiency efforts and capacity expansion in markets like Mexico and Europe, which they expect to translate into earnings resilience even though trailing margins are currently slightly below last year.

After a year with mid single digit net margins, bulls argue that the real story is how new case ready and prepared capacity could reshape Pilgrim's Pride's earnings power over time, not just this quarter's dip. 🐂 Pilgrim's Pride Bull Case

Earnings swing: Q4 net income at US$88m

- Quarterly net income went from US$355.5m in Q2 2025 and US$342.8m in Q3 2025 to US$88.0m in Q4 2025, with EPS moving from around US$1.50 and US$1.44 earlier in the year to US$0.37 in Q4.

- Bears argue that this pattern lines up with forecasts for earnings to decline by about 7.7% per year over the next three years, and they question whether factors like higher industry chicken supply, integration risk at new facilities, and possible feed cost swings could keep profitability closer to the lower end of recent quarters rather than the higher Q2 and Q3 levels.

- Critics highlight that analysts see earnings stepping down from roughly US$1.2b today to around US$678.0m in more cautious scenarios, which is directionally consistent with a quarter like Q4 producing much lower net income than the mid year peaks.

- They also point to margin compression concerns in bearish assumptions, where profit margins move from about 6.7% to 3.6%, and see the Q4 earnings volatility as an example of how sensitive results can be to pricing, utilization, and input costs.

For more cautious investors, the sharp move from Q2 and Q3 profit levels to Q4's lower net income is exactly the kind of earnings volatility they are watching. 🐻 Pilgrim's Pride Bear Case

P/E of 9.1x versus 19.4x market

- On trailing 12 month numbers, Pilgrim's Pride trades on a P/E of 9.1x, compared with about 19.4x for the US market and 23.9x for the US Food industry, while earnings are forecast to decline around 7.7% per year and revenue to grow roughly 1.3% per year over the next three years.

- Consensus narrative notes that this combination, a lower multiple and relatively modest revenue growth expectations, asks investors to weigh a data flagged valuation discount against an outlook where earnings are projected to move from about US$1.2b today to roughly US$874.8m by 2028 and profit margins are modeled to compress from around 6.8% to 4.6%.

- Supporters of the balanced view see the current P/E gap to the market and sector as one reason some investors may still be interested, even with slower forecast revenue growth of 1.5% per year and an expected step down in earnings.

- At the same time, the consensus analyst price target of US$43.57 is close to the current share price of US$41.65, which suggests the market is already weighing that lower growth and margin path against the apparent valuation discount Next Steps

To see how these results tie into long-term growth, risks, and valuation, check out the full range of community narratives for Pilgrim's Pride on Simply Wall St. Add the company to your watchlist or portfolio so you'll be alerted when the story evolves.

See the numbers differently? Take a couple of minutes to test your own view against the data and shape a narrative that fits how you see Pilgrim's Pride, Do it your way.

A great starting point for your Pilgrim's Pride research is our analysis highlighting 2 key rewards and 2 important warning signs that could impact your investment decision.

See What Else Is Out There

Pilgrim's Pride is contending with a sharp step down in quarterly net income, earnings volatility, and analyst expectations for lower profit margins in coming years.

If that earnings uncertainty makes you cautious, take a moment to scan our 85 resilient stocks with low risk scores and see companies where results and risk profiles look more stable right now.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

Have feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team@simplywallst.com