- LIVE QUOTES

- LEARN

- HELP

Nasdaq

Nasdaq Wall Street Journal

Wall Street JournalEN

Edwards Lifesciences (EW) Margin Compression To 17.5% Tests Premium P/E Narrative

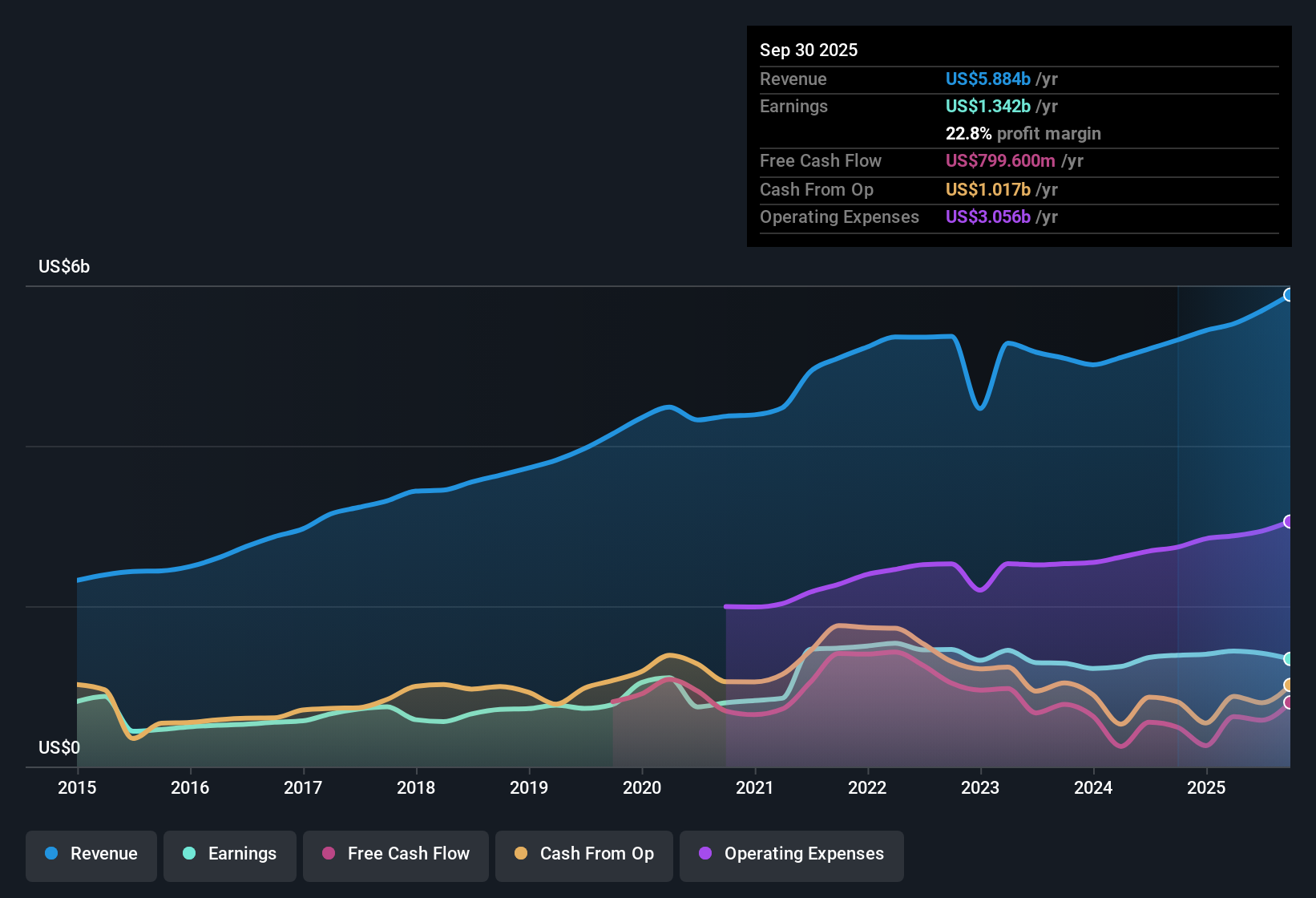

Edwards Lifesciences FY 2025 earnings snapshot

Edwards Lifesciences (EW) has wrapped up FY 2025 with fourth quarter revenue of US$1,569.6 million and basic EPS of US$0.11, setting the tone for how investors assess the latest stretch of results. The company has seen revenue move from US$1,385.8 million in Q4 2024 to US$1,569.6 million in Q4 2025, while basic EPS over that same period went from US$0.59 to US$0.11. This puts the focus squarely on how efficiently those sales are translating into profit. With trailing net profit margins now below last year’s level, this earnings season is really about how you feel regarding the trade off between growth and profitability.

See our full analysis for Edwards Lifesciences.With the headline numbers on the table, the next step is to see how this earnings profile lines up with the prevailing narratives around Edwards Lifesciences, and where the recent results push back against those stories.

See what the community is saying about Edwards Lifesciences

Margins Under Pressure at 17.5%

- Over the last 12 months, Edwards Lifesciences reported a trailing net profit margin of 17.5%, compared with 25.8% a year earlier, alongside trailing net income from ongoing operations of US$1,060.1 million on US$6,067.6 million of revenue.

- Analysts' consensus view expects earnings to grow about 14.9% per year while accepting slightly lower margins. This sits in tension with the recent margin step down from 25.8% to 17.5% as investors weigh how much profit each dollar of future revenue might produce.

- The consensus narrative highlights new therapies like TAVR expansions, EVOQUE and Sapien M3 as potential growth drivers. However, the current margin level shows that adding revenue did not translate into the same profit share as last year.

- Ongoing spending on R&D and acquisitions such as JenaValve, along with tariff headwinds that are expected to hit EPS by US$0.05 in 2025, helps explain why reported profitability sits below the earlier 25.8% margin even as revenue reached US$6.1b.

EPS Swings Across FY 2025

- Across FY 2025, basic EPS moved from US$0.62 in Q1 to US$0.11 in Q4, while quarterly net income from ongoing operations ranged between US$365.2 million in Q1 and US$64.2 million in Q4 on revenue that stayed between US$1,412.7 million and US$1,569.6 million.

- Bulls point to product approvals and wider indications as reasons earnings can scale over time, but the pattern of quarterly EPS and net income in 2025 shows that higher quarterly revenue alone did not consistently line up with higher per share earnings.

- For example, revenue of US$1,569.6 million in Q4 came alongside basic EPS of US$0.11, whereas Q1 revenue of US$1,412.7 million supported basic EPS of US$0.62, so the higher top line in Q4 coincided with much lower EPS.

- Earnings from discontinued operations also shifted from a loss of US$7.2 million in Q1 to income of US$27 million in Q4, which means part of the bottom line pattern is tied to portfolio changes rather than just the core cardiovascular franchises.

Premium P/E of 43.4x

- Edwards Lifesciences trades on a trailing P/E of 43.4x, compared with a peer average of 30.2x and an industry average of 30.9x, while the current share price of US$79.33 sits below a DCF fair value of about US$90.15 and an analyst price target of US$96.64.

- Bears focus on that higher P/E and the drop in net margin from 25.8% to 17.5%, arguing the stock carries a premium valuation while profitability runs below last year, even though the DCF fair value and price target both sit above the current market price.

- The DCF fair value being around 12% above US$79.33 and the analyst target roughly 22% higher both imply some headroom. However, they also assume earnings growth around 14.9% per year from a margin base that is currently lower than a year ago.

- To match the analyst target, the company would need to reach earnings of about US$1.8b and trade on a 35.1x P/E, which is still above the current industry P/E of 29.7x and shows how much of the thesis rests on delivering that earnings path.

Next Steps

To see how these results tie into long-term growth, risks, and valuation, check out the full range of community narratives for Edwards Lifesciences on Simply Wall St. Add the company to your watchlist or portfolio so you'll be alerted when the story evolves.

See the numbers differently? Take a couple of minutes to test your own view against the data and shape the story you think fits best: Do it your way

A great starting point for your Edwards Lifesciences research is our analysis highlighting 3 key rewards and 2 important warning signs that could impact your investment decision.

See What Else Is Out There

Edwards Lifesciences is working through compressed net margins, sharp EPS swings across quarters, and a premium 43.4x P/E compared to peers.

If those pressure points make you hesitate, put them side by side with our 85 resilient stocks with low risk scores to quickly spot businesses where earnings stability and risk scores look more comfortable.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

Have feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team@simplywallst.com