- LIVE QUOTES

- LEARN

- HELP

Nasdaq

Nasdaq Wall Street Journal

Wall Street JournalEN

Assessing Textron (TXT) Valuation After New Share Buyback And Board Appointment

Textron’s new buyback and board appointment in focus

Textron (TXT) has drawn fresh attention after its Board authorized a new share repurchase program for up to 25,000,000 shares, alongside the upcoming addition of finance veteran Cristina Méndez to its Board of Directors.

See our latest analysis for Textron.

At a share price of $97.28, Textron has seen a 7.22% 7 day share price return and an 11.75% year to date share price return. Its 1 year total shareholder return of 33.76% and 5 year total shareholder return of 92.61% point to stronger longer term momentum that recent buyback and governance news appears to have brought back into focus.

If this kind of capital allocation news has you watching industrial names more closely, it might be a good time to scan our screener of 24 power grid technology and infrastructure stocks for other potential ideas.

With Textron trading close to its analyst price target and with recent returns already strong, the key question for investors is whether the buyback and board refresh leave room for further upside, or whether the market is already pricing in future growth.

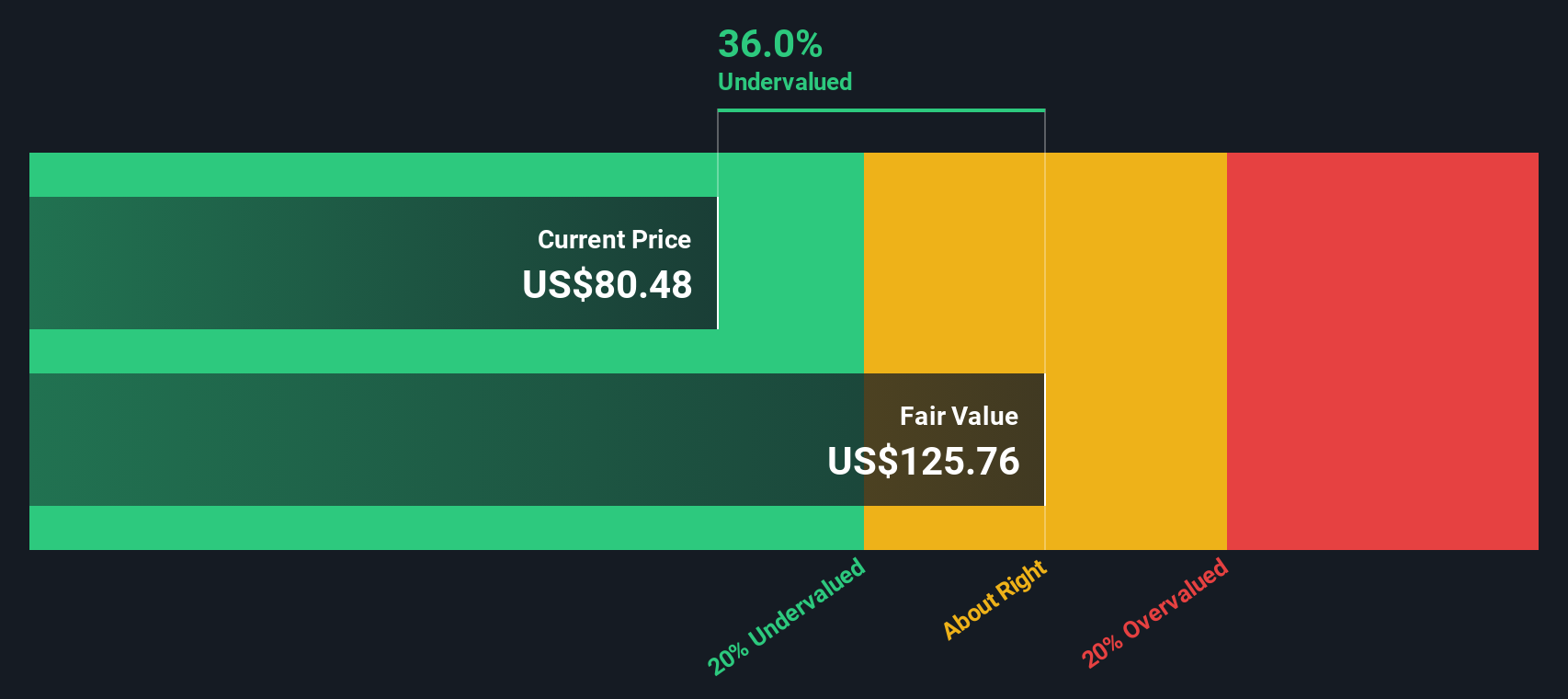

Most Popular Narrative: 1.1% Undervalued

Textron’s most followed valuation narrative points to a fair value of about $98.41, sitting just above the recent $97.28 share price and framing the buyback against a fairly tight valuation gap.

The FAA certification of the GE Aerospace Catalyst turboprop engine for the Beechcraft Denali program is set to significantly boost revenue as the program progresses toward completion, offering a new product line with expected strong market demand.

Bell's military and commercial segments are experiencing strong growth, driven by FLRAA program execution and recent new contracts for aircraft, which will positively impact revenue and potentially increase net margins through scale and efficiency improvements.

Curious how modest growth assumptions, slightly higher long term margins and a lower future earnings multiple still arrive near today’s price? The narrative lays out a detailed earnings track, share count path and discount rate logic that all need to hold together. If you want to see which combination of revenue, margin and valuation expectations is doing the heavy lifting here, the full story is worth a look.

Result: Fair Value of $98.41 (UNDERVALUED)

Have a read of the narrative in full and understand what's behind the forecasts.

However, the narrative can shift quickly if cost management issues persist or if weaker product mix in Aviation and softer industrial demand continue to pressure segment profits.

Find out about the key risks to this Textron narrative.

Another View: DCF Points To A Tighter Picture

While the popular narrative sees Textron as about 1.1% undervalued at a fair value of $98.41, our DCF model tells a different story. On that basis, the shares at $97.28 sit above an estimated future cash flow value of $93.26, which frames Textron as overvalued instead of slightly cheap.

DCF models lean heavily on long term cash flow, discount rates and terminal assumptions, so this gap is not huge in dollar terms but it does flip the conclusion. For you, the question is whether you put more weight on earnings based narratives or on this cash flow driven view.

Look into how the SWS DCF model arrives at its fair value.

Simply Wall St performs a discounted cash flow (DCF) on every stock in the world every day (check out Textron for example). We show the entire calculation in full. You can track the result in your watchlist or portfolio and be alerted when this changes, or use our stock screener to discover 51 high quality undervalued stocks. If you save a screener we even alert you when new companies match - so you never miss a potential opportunity.

Build Your Own Textron Narrative

If parts of this story do not quite fit your view, or you prefer to lean on your own research, you can pull the same data, adjust the assumptions and shape a personal thesis in just a few minutes, then Do it your way.

A good starting point is our analysis highlighting 4 key rewards investors are optimistic about regarding Textron.

Looking for more investment ideas?

If Textron has sharpened your focus, do not stop here. The next strong addition to your watchlist could be sitting in plain sight.

- Target companies with resilient income and steady cash flows by scanning our list of 13 dividend fortresses that may suit income focused portfolios.

- Hunt for potential mispricings by reviewing our collection of screener containing 24 high quality undiscovered gems that pair solid fundamentals with relatively low investor attention.

- Prioritise stability and capital protection by checking our set of 85 resilient stocks with low risk scores that score well on financial strength and volatility measures.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

Have feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team@simplywallst.com