- LIVE QUOTES

- LEARN

- HELP

Nasdaq

Nasdaq Wall Street Journal

Wall Street JournalEN

A Look At Virtu Financial (VIRT) Valuation After EPS More Than Doubles In 2025 Results

Virtu Financial (VIRT) has drawn fresh attention after reporting full year 2025 results, with revenue of US$3,632.12 million, net income of US$468.36 million, and earnings per share more than doubling compared with the prior year.

See our latest analysis for Virtu Financial.

The latest results and dividend affirmation come after a strong run, with a 16.35% year to date share price return and a 3 year total shareholder return of 107.41%. This suggests momentum has been building over time, despite a recent 3.68% one day pullback.

If Virtu’s move has you thinking about where else trading and market infrastructure themes could play out, take a look at our screener of 34 AI infrastructure stocks as a starting point for fresh ideas.

With earnings per share more than doubling and the stock up strongly over 3 years, yet trading at what some models flag as a sizeable intrinsic discount, is this a genuine buying opportunity, or is the market already pricing in future growth?

Most Popular Narrative: 254.2% Overvalued

Compared with the last close at $37.93, the most followed narrative puts Virtu Financial’s fair value at $10.71, creating a sharp gap that grabs attention.

VIRT "stock ticker name" or better known as Vertiv Holdings. Is one of them companies, that is continually making Global Headlines. Any company let alone with a Positive Cash Flow of 302%+, is one that should be talked about.

Curious how this narrative gets to such a low fair value? The key ingredients are its margin assumptions and the profit multiple baked into the model. Want to see which numbers are pulling that price target away from today’s share price? Read on in the full narrative to unpack the logic behind that gap.

Result: Fair Value of $10.71 (OVERVALUED)

Have a read of the narrative in full and understand what's behind the forecasts.

However, this story could change quickly if Virtu’s revenue contraction continues, or if trading conditions shift in ways that pressure its market making economics.

Find out about the key risks to this Virtu Financial narrative.

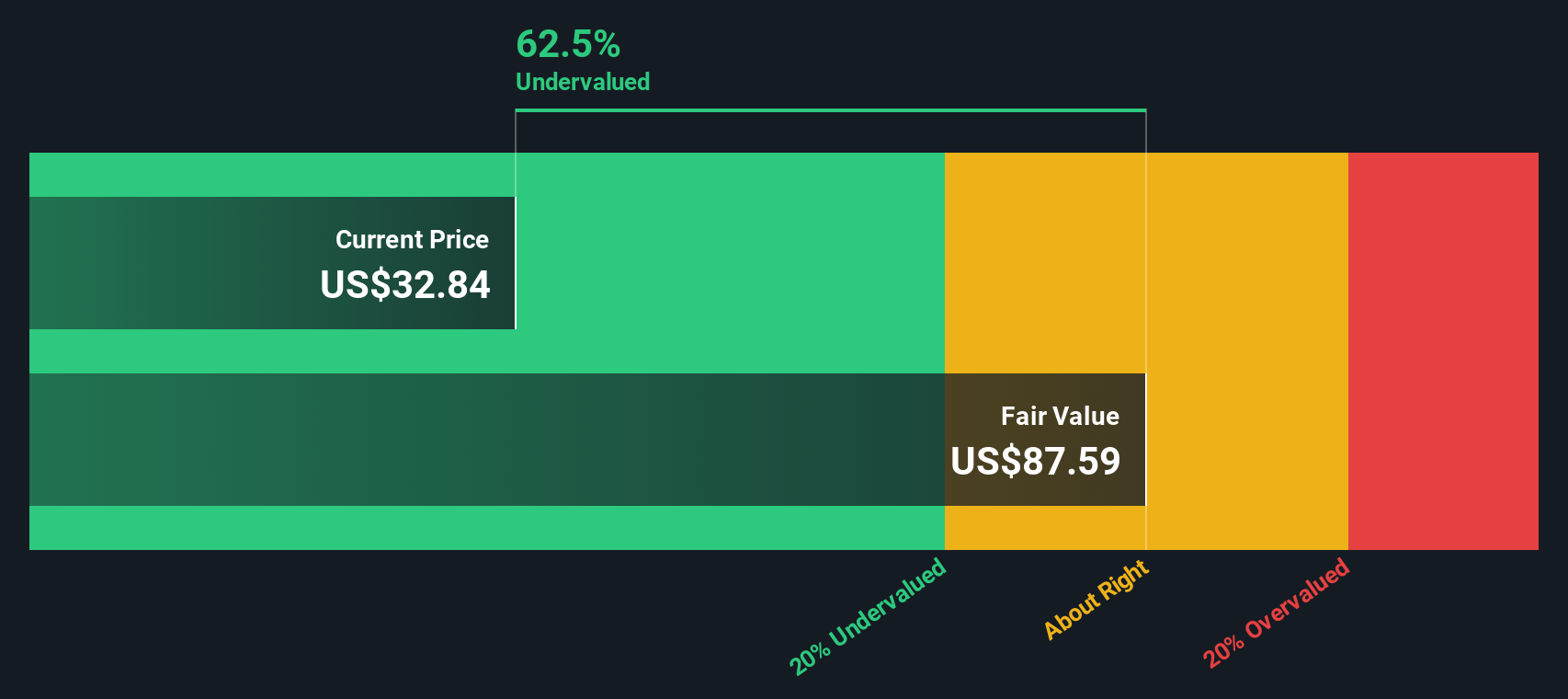

Another Take On Virtu’s Value

The user narrative pegs fair value at $10.71 and calls VIRT heavily overvalued, but our DCF model points the other way, with a future cash flow value of $80.17 and the shares trading at a 52.7% discount. Which story fits better with the risks you care about most?

Look into how the SWS DCF model arrives at its fair value.

Build Your Own Virtu Financial Narrative

If you are not convinced by these viewpoints or prefer to lean on your own research and assumptions, you can quickly build a custom thesis in just a few minutes, starting with Do it your way.

A good starting point is our analysis highlighting 5 key rewards investors are optimistic about regarding Virtu Financial.

Looking for more investment ideas?

If Virtu has sharpened your thinking, do not stop here. Broaden your watchlist with ideas filtered by quality, income, and risk using our screeners.

- Target dependable income by checking out 13 dividend fortresses that focus on companies with higher dividend yields.

- Hunt for value by scanning 51 high quality undervalued stocks that highlight companies with solid fundamentals trading below some fair value estimates.

- Prioritize capital preservation by reviewing 85 resilient stocks with low risk scores that spotlight businesses with lower assessed risk profiles.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

Have feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team@simplywallst.com