- LIVE QUOTES

- LEARN

- HELP

Nasdaq

Nasdaq Wall Street Journal

Wall Street JournalEN

Argan (AGX) Valuation Check After Strong Quarter And Power Infrastructure Pipeline Optimism

Argan (AGX) is attracting fresh attention after robust quarterly results, supportive management commentary on power and infrastructure projects, and a balance sheet that includes net cash, along with a project backlog and future pipeline that analysts describe as constructive.

See our latest analysis for Argan.

The latest quarterly update appears to have shifted sentiment quickly, with a 13.7% 1 day share price return and a 36.6% 30 day share price return, contributing to a very large 1 year total shareholder return and double digit multiple total shareholder return over three and five years. This suggests investors are reassessing both growth prospects and perceived risk around Argan’s project pipeline and net cash position.

If Argan’s surge has you thinking about other opportunities in power and infrastructure, it could be a good time to check out 24 power grid technology and infrastructure stocks as a starting list of ideas.

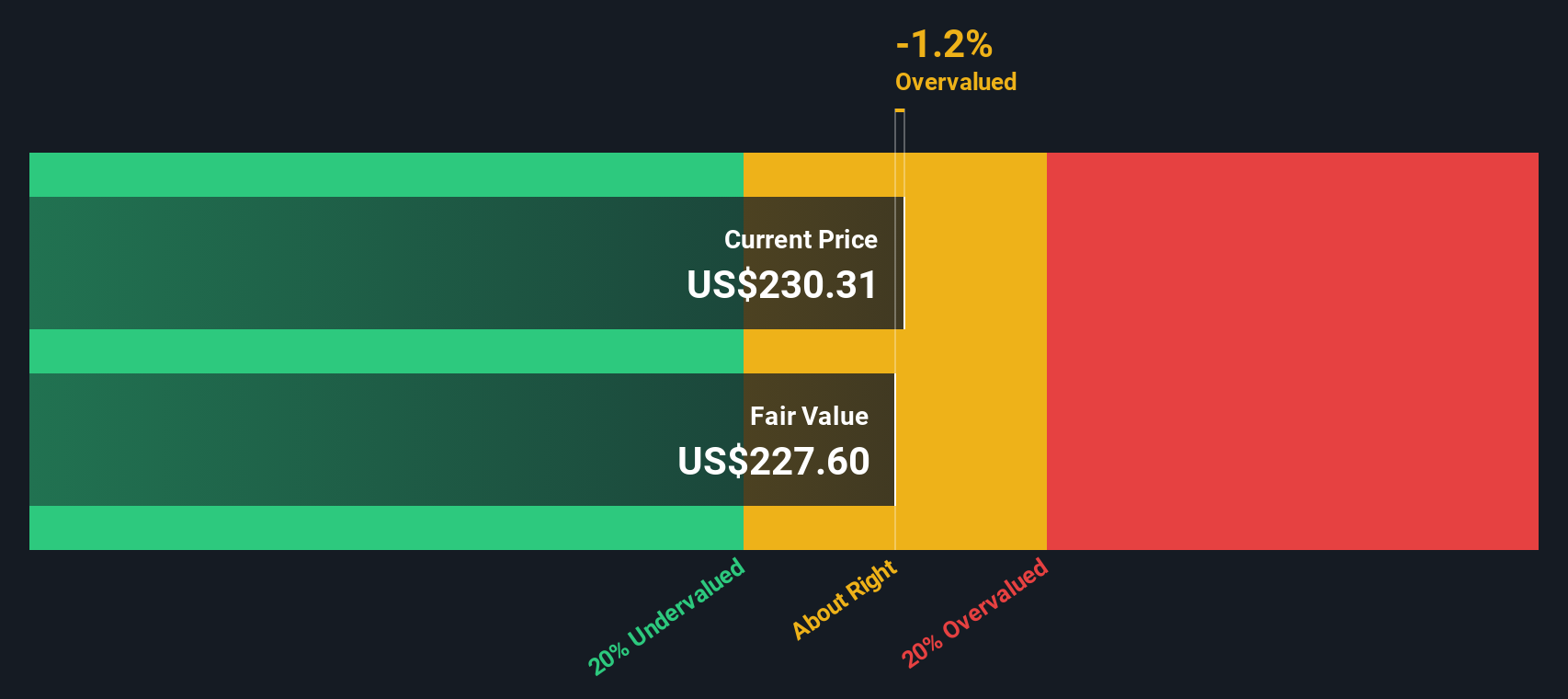

With Argan now trading at $422.50 and sitting at a discount to analyst price targets on some models but a premium to others, the central question is whether there is still a buying opportunity here or if the market is already pricing in future growth.

Preferred P/E of 48.9x: Is it justified?

On simple multiples, Argan is not cheap. The shares trade on a P/E of 48.9x, and our system indicates this is expensive relative to both peers and a modelled fair ratio, even after the recent move in the share price to $422.50.

The P/E ratio compares the current share price to the company’s earnings, so a higher multiple usually means investors are willing to pay more today for each dollar of profit. In project based businesses like construction and power infrastructure, that can reflect expectations for sustained earnings, a strong project pipeline, or perceived quality of those earnings rather than just one strong year.

What stands out here is that Argan’s 48.9x P/E sits above three separate reference points. It is higher than the estimated fair P/E of 35.2x, higher than the US Construction industry average of 39.5x, and above the peer average of 41.3x. That kind of premium suggests the market is placing a rich price on Argan’s current and forecast earnings and could move closer to the lower fair ratio level if sentiment or forecasts change.

Explore the SWS fair ratio for Argan

Result: Price-to-Earnings of 48.9x (OVERVALUED)

However, there are clear risks, including Argan trading below the US$361 analyst price target and reliance on a project-driven revenue base that can be lumpy.

Find out about the key risks to this Argan narrative.

Another angle from our DCF model

While the P/E points to an expensive stock, our DCF model presents an even tougher picture. On that framework, Argan at $422.50 is trading well above an estimated future cash flow value of $184.79. This highlights valuation risk if sentiment cools or growth assumptions soften.

Look into how the SWS DCF model arrives at its fair value.

Simply Wall St performs a discounted cash flow (DCF) on every stock in the world every day (check out Argan for example). We show the entire calculation in full. You can track the result in your watchlist or portfolio and be alerted when this changes, or use our stock screener to discover 51 high quality undervalued stocks. If you save a screener we even alert you when new companies match - so you never miss a potential opportunity.

Build Your Own Argan Narrative

If you see the numbers differently or want to stress test your own assumptions, you can build a custom Argan story in just a few minutes, starting with Do it your way.

A great starting point for your Argan research is our analysis highlighting 2 key rewards and 2 important warning signs that could impact your investment decision.

Looking for more investment ideas?

If Argan has sharpened your focus, do not stop here. The next strong idea on your list could come from a broader search across quality stocks.

- Spot potential bargains early by scanning our 51 high quality undervalued stocks, which pairs solid fundamentals with prices that may not fully reflect their strengths.

- Prioritise resilience with the 85 resilient stocks with low risk scores, built to highlight companies that our system flags with lower overall risk scores.

- Hunt for future leaders before the crowd catches on by checking the screener containing 24 high quality undiscovered gems, packed with lesser known names that already show strong fundamentals.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

Have feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team@simplywallst.com