- LIVE QUOTES

- LEARN

- HELP

Nasdaq

Nasdaq Wall Street Journal

Wall Street JournalEN

Vishay Precision Group (VPG) EPS Rebound Tests Bullish Margin Expansion Narrative

Vishay Precision Group (VPG) has just posted its FY 2025 third quarter results with revenue of US$79.7 million and EPS of US$0.59, putting fresh numbers on the table for investors watching its earnings trajectory. The company has seen revenue move from US$75.7 million in Q3 2024 to US$79.7 million in Q3 2025, while EPS has shifted from a loss of US$0.10 per share to EPS of US$0.59 over the same period. This sets up an earnings season where the key question is how durable these margins look from here.

See our full analysis for Vishay Precision Group.With the latest figures in hand, the next step is to see how this earnings profile lines up against the prevailing narratives around Vishay Precision Group and where the numbers start to challenge those stories.

See what the community is saying about Vishay Precision Group

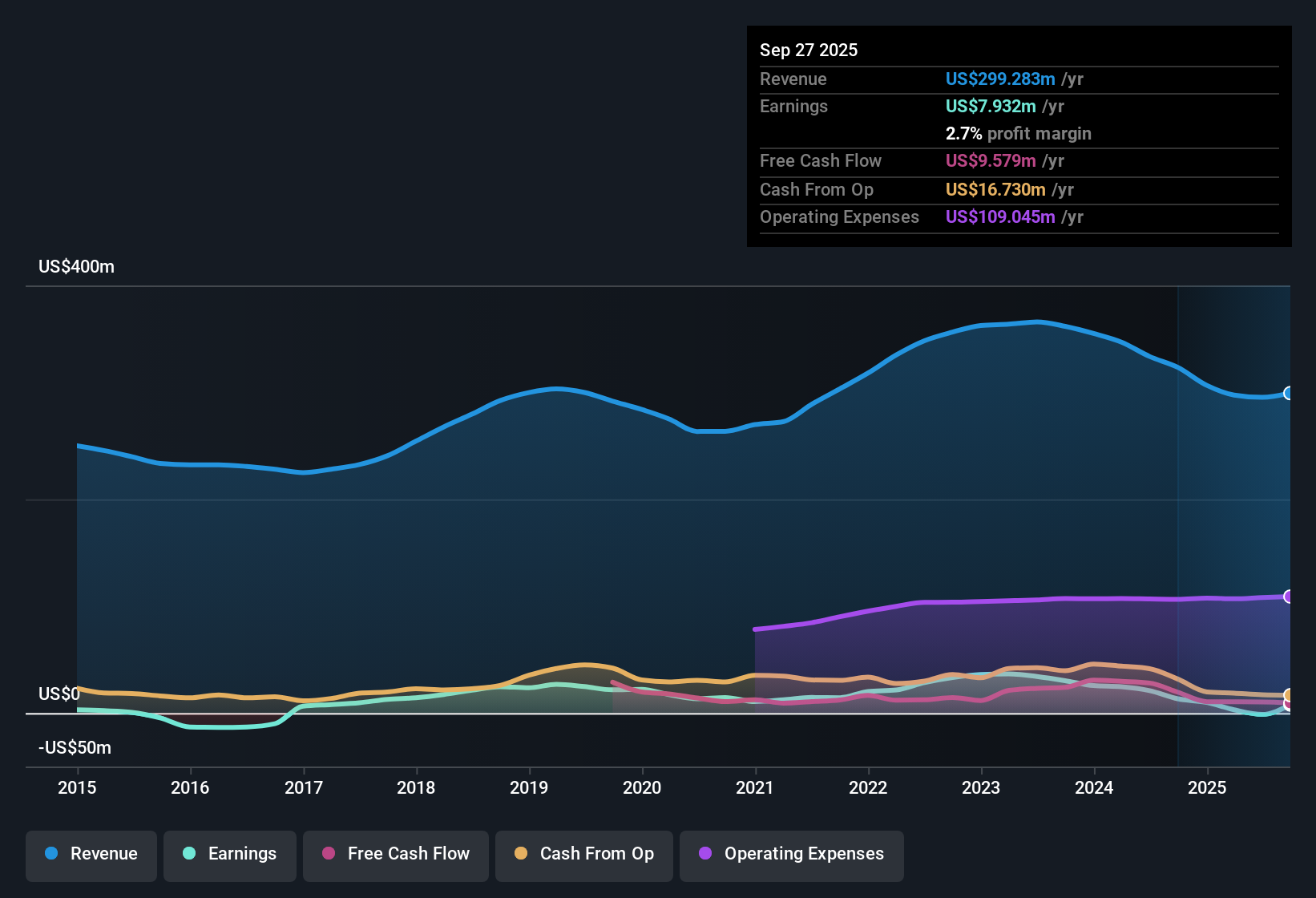

Margins Under Pressure At 2.7% Net

- Over the last 12 months VPG converted US$299.3 million of revenue into US$7.9 million of net income, which works out to a 2.7% net margin compared with 4.2% a year earlier.

- Consensus narrative talks about higher margins helped by automation, robotics and cost savings. However, the current 2.7% margin and a five year earnings decline of about 10.3% a year highlight the gap between that story and the trailing numbers.

- Supporters point to cost programs targeting US$5 million of annualized savings and new orders in areas like humanoid robotics and electrification, which are seen as higher margin niches.

- The trailing margin step down and reliance on a US$4.4 million one off gain make it important to check whether those expected margin gains are already assumed in the current pricing.

EPS Swing And One Off Gain

- Quarterly EPS moved from a loss of US$0.10 in Q3 2024 to US$0.59 in Q3 2025, while the last 12 months include a US$4.4 million non recurring gain that lifts reported earnings quality on paper but is not repeat business.

- For bullish investors who see this EPS swing as a clean turning point, the presence of that one off gain and the five year 10.3% annual earnings decline mean the latest quarter needs to be weighed against a longer stretch of softer profitability.

- Bulls highlight growing interest in humanoid robotics, where VPG has about US$3.6 million of projects so far, and rising sensor bookings that could help EPS if they translate into steady production volumes.

- At the same time, softness in areas like Weighing Solutions and Measurement Systems and booking delays in defense and space programs show that not all segments are moving in the same direction yet.

Rich P/E Versus DCF Fair Value

- At a share price of US$46.43, VPG trades on a trailing P/E of 77.7x, compared with a peer average of 61.6x and US Electronic industry average of 26.9x, while the supplied DCF fair value is US$34.87 and the single analyst price target in the data is US$48.00.

- Bears point out that this premium multiple sits on top of a 2.7% net margin, a five year earnings decline and that US$4.4 million one off gain, so the current valuation already assumes improvement that is not yet visible in the trailing figures.

- Cautious investors also flag that earnings over the past five years have moved lower on average even as the multiple has remained high versus peers and the DCF fair value.

- Supporters of the bearish view therefore focus on whether future margin expansion and growth can justify paying more than both the DCF fair value and the analyst target embedded in the data.

Next Steps

To see how these results tie into long-term growth, risks, and valuation, check out the full range of community narratives for Vishay Precision Group on Simply Wall St. Add the company to your watchlist or portfolio so you'll be alerted when the story evolves.

See the numbers in a different light, then turn that view into your own narrative in just a few minutes and let your thesis stand out. Do it your way

A great starting point for your Vishay Precision Group research is our analysis highlighting 3 important warning signs that could impact your investment decision.

See What Else Is Out There

Vishay Precision Group combines a 2.7% net margin, a five year 10.3% annual earnings decline and a rich 77.7x P/E, all resting on a US$4.4 million one off gain.

If that mix of thin margins and a premium valuation feels uncomfortable, compare it with our 52 high quality undervalued stocks to see which companies offer steadier earnings at prices that look more grounded in their recent results.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

Have feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team@simplywallst.com