- LIVE QUOTES

- LEARN

- HELP

Nasdaq

Nasdaq Wall Street Journal

Wall Street JournalEN

Assessing Woodward (WWD) Valuation After Strong Quarter And Higher 2026 Guidance

Why Woodward’s latest quarter is drawing fresh attention

Woodward (WWD) just posted a quarter that topped expectations, raised its 2026 sales and earnings guidance, and lifted its dividend. This gives investors a fresh, fundamentals based catalyst to reassess the stock.

See our latest analysis for Woodward.

The stronger earnings, higher 2026 guidance, dividend increase, and ongoing buybacks sit alongside a sharp acceleration in the share price. The 90 day share price return is 45.93% and the 1 year total shareholder return is 104.44%, suggesting momentum has been building over both shorter and longer horizons.

If Woodward’s move has you looking for other ways to play the build out of critical systems, it could be worth checking out 24 power grid technology and infrastructure stocks as a next research stop.

With the shares up strongly and trading only about 6% below the average analyst price target, the key question now is whether Woodward is still offering value or if the market is already factoring in much of the future growth.

Most Popular Narrative: 4.9% Undervalued

Woodward’s most followed narrative pegs fair value at $413, slightly above the last close of $392.78, and builds that view from detailed long range earnings and margin assumptions.

The analyst fair value estimate for Woodward has shifted from $317.13 to $413.00. Analysts point to a higher assumed future P/E multiple and supportive recent research updates from firms raising their price targets as key drivers behind the change.

Curious what is sitting behind that higher fair value mark. The narrative leans heavily on sustained revenue growth, a stronger profit margin profile, and a richer future earnings multiple. Investors may want to see how those pieces fit together.

Result: Fair Value of $413 (UNDERVALUED)

Have a read of the narrative in full and understand what's behind the forecasts.

However, there is still meaningful execution and capital allocation risk if heavy investment, acquisitions, or end market volatility fail to translate into the earnings path that analysts are modeling.

Find out about the key risks to this Woodward narrative.

Another view on valuation

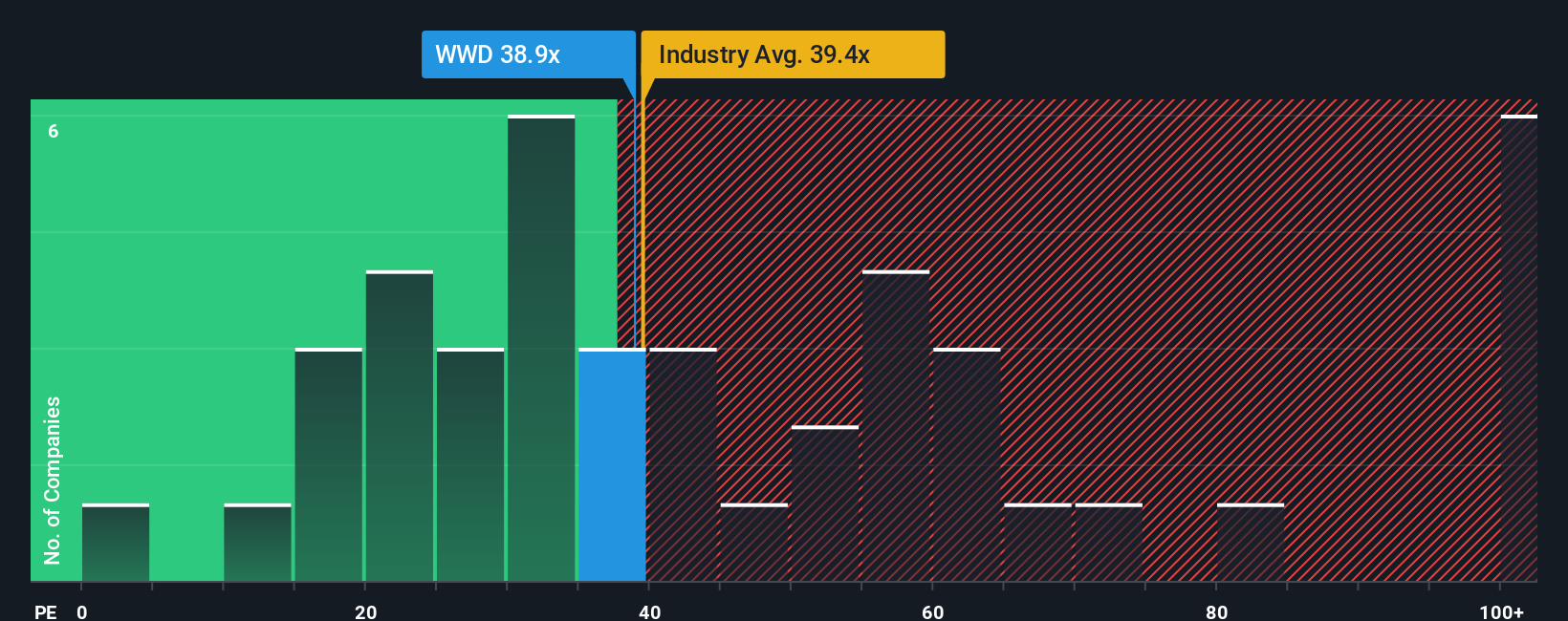

The narrative pegs Woodward at 4.9% undervalued, but the P/E data tell a different story. At 47.9x earnings, the shares sit above both the estimated fair ratio of 31x and the US Aerospace & Defense average of 41.3x. This points to meaningful valuation risk if expectations cool even slightly.

See what the numbers say about this price — find out in our valuation breakdown.

Build Your Own Woodward Narrative

If parts of this story do not quite line up with your own view and you prefer to test the inputs yourself, you can spin up a custom Woodward thesis in just a few minutes and see how your assumptions compare to the crowd, then Do it your way.

A good starting point is our analysis highlighting 2 key rewards investors are optimistic about regarding Woodward.

Looking for more investment ideas?

If Woodward has sharpened your focus, do not stop here. Broaden your watchlist now so you are not scrambling when the next opportunity appears.

- Target value by scanning our list of 52 high quality undervalued stocks that combine quality fundamentals with prices that may warrant a closer look.

- Prioritize resilience by checking a solid balance sheet and fundamentals stocks screener (45 results) that could handle tougher conditions without you constantly worrying about financial strain.

- Get ahead of the crowd by reviewing a screener containing 24 high quality undiscovered gems before they land on everyone else’s radar.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

Have feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team@simplywallst.com